{kind=link}

What if the government let you save for medical bills tax-free, and cut your tax bill at the same time?

That’s basically what a Health Savings Account does when paired with a high-deductible health plan.

Contribute pre-tax money, let it grow tax-free, and take it out tax-free for qualified medical costs.

Leftover funds roll over year to year, the account moves with you if you change jobs, and many HSAs let you invest the balance.

This post explains the tax advantages, who qualifies, and how to use an HSA so you can decide if it’s right for you.

Core Mechanics of How a Health Savings Account Functions

A health savings account pairs with a high-deductible health plan and gives you a place to stash money for medical bills with some serious tax perks. You don’t pay tax on what goes in, your balance grows without getting taxed, and when you pull money out for qualified medical costs, that’s tax-free too. It’s a triple win.

Here’s how it actually works. Money flows into the HSA from your paycheck before taxes get taken out, or your employer might chip in as part of your benefits package. You can also add money yourself after the fact. Once it’s in there, the cash either sits earning a bit of interest or you can invest it if your HSA provider lets you. Got a medical bill? Doctor visit, prescriptions, dental work, whatever. Pay it straight from the HSA with a debit card, check, or online transfer. As long as the expense is on the IRS’s qualified list, the money comes out clean. No taxes.

And here’s the part people love: leftover money doesn’t disappear at year-end. It rolls over. No “use it or lose it” deadline hanging over your head. The account follows you even if you switch jobs or change health plans, as long as you stay enrolled in an HSA-eligible high-deductible plan to keep contributing.

Step by step, using an HSA looks like this:

- Make sure you’re enrolled in an HSA-eligible high-deductible health plan.

- Open an HSA through a bank or your employer’s provider.

- Put money in, up to the annual IRS limit. Payroll deduction or direct deposit both work.

- Use the funds when medical expenses pop up, or just let the balance sit and grow.

- Keep every receipt. If the IRS ever asks, you’ll need proof that what you spent was actually qualified.

- Unused money rolls over automatically. Keep contributing each year as long as you’re still eligible.

Eligibility Rules That Determine Whether You Can Use an HSA

You can’t just open an HSA because you feel like it. The IRS has a checklist, and you’ve got to tick every box during the months you want to contribute.

First up, you need to be covered by a high-deductible health plan that hits the IRS definition. For 2024, that meant your plan’s deductible had to be at least $1,600 for individual coverage or $3,200 for family. The out-of-pocket max couldn’t go over $8,050 individual or $16,100 family. In 2025, those numbers bumped up to $1,650 individual / $3,300 family for the deductible and $8,300 individual / $16,600 family for the out-of-pocket cap. If your plan doesn’t clear those hurdles, it’s not HSA-compatible.

Second, you can’t have other health coverage that disqualifies you. That includes being on Medicare or having a general-purpose flexible spending account that covers medical expenses before you hit your deductible. You also can’t be claimed as a dependent on someone else’s return. Limited-purpose FSAs for dental and vision only? Those are fine. Disability insurance, long-term care, stand-alone dental or vision plans? All allowed.

Once you enroll in Medicare, you’re done contributing. You can still spend what’s already in the HSA, but no new money can go in, even if you’re still working. If any of these apply, you’re blocked from putting money into an HSA during that time:

- You’re enrolled in Medicare.

- Someone else claims you as a dependent.

- You have non-HDHP coverage that isn’t an allowed exception, like a general-purpose FSA or a low-deductible plan.

- Your HDHP doesn’t meet the IRS minimums or it exceeds the out-of-pocket max.

- Your spouse’s non-HDHP plan covers you before the deductible kicks in.

Contribution Limits and How HSA Contributions Work

The IRS caps how much you can deposit into an HSA each year. These limits apply to everything that goes in: your money, your employer’s contributions, anyone else’s. It all counts toward the same ceiling. For 2024, the limit was $4,150 for individuals with self-only coverage and $8,300 for family plans. In 2025, those went up to $4,300 for self-only and $8,550 for family. If you’re 55 or older, you can throw in an extra $1,000 catch-up contribution.

| Year | Individual Limit | Family Limit | Catch-Up Amount (Age 55+) |

|---|---|---|---|

| 2024 | $4,150 | $8,300 | +$1,000 |

| 2025 | $4,300 | $8,550 | +$1,000 |

Contributions happen a few ways. Most common is payroll deduction if your employer offers HSA benefits. That money gets pulled before federal income tax, and usually state and FICA taxes too. Immediate tax break. If your employer doesn’t do payroll contributions, or you want to add more yourself, you can make direct deposits to your HSA provider. Those deposits use after-tax money, but you claim the deduction when you file, so the tax benefit ends up the same.

Employers can also put money into your HSA. Some match what you contribute up to a dollar amount, others drop in a flat sum at the start of the year. All of it counts toward your annual limit. If you become HSA-eligible partway through the year, your limit usually gets prorated by how many months you were eligible. There’s a “last-month rule” that can let you contribute the full year’s amount if you’re eligible on December 1 and stay that way for the next 12 months, but check IRS guidelines or talk to a tax advisor if you’re in that situation.

You’ve got until the tax filing deadline to make HSA contributions for a given tax year. Usually that’s April 15 of the following year. So you can contribute to your 2024 HSA up until around April 15, 2025, and still claim the deduction on your 2024 return.

Understanding HSA Withdrawals and Qualified Medical Use

Pull money from your HSA for qualified medical expenses and you pay zero tax on the withdrawal. The IRS publishes a long list in Publication 502. It covers most routine and necessary healthcare: doctor visits, hospital stays, surgeries, prescriptions, lab tests, x-rays, mental health counseling, physical therapy, dental care, vision exams, glasses, contacts, hearing aids, certain over-the-counter meds, and menstrual products. You can also use HSA funds for long-term care services, COBRA premiums, health insurance premiums while you’re on unemployment, and Medicare premiums once you’re enrolled (though you can’t contribute anymore after Medicare starts).

Most HSA providers give you a debit card that works anywhere accepting payment for medical services. You can also pay out of pocket and reimburse yourself later by moving money from your HSA to your checking account. The catch is you need documentation. Keep receipts showing the date, provider, service or product, and amount paid. If the IRS ever audits your HSA withdrawals, those receipts prove the expenses were qualified. You can reimburse yourself years later for old medical expenses as long as the expense happened after you opened the HSA and you saved the receipt. This delayed-reimbursement thing is one way to let your HSA balance grow invested while covering your immediate medical costs with cash.

Typical qualified expenses you can pay with HSA funds:

- Doctor visits and specialist consultations

- Prescription drugs and insulin

- Dental cleanings, fillings, crowns, braces, dentures

- Vision exams, prescription glasses, contacts, corrective eye surgery like LASIK

- Mental health and psychiatric care

- Ambulance and emergency room services

- Medical equipment: crutches, bandages, blood pressure monitors, diabetic supplies

Non-Qualified Expenses, Penalties, and Age-Based Rules in HSAs

Withdraw HSA money for something that’s not a qualified medical expense and the tax treatment flips. Before age 65, a non-qualified withdrawal gets added to your taxable income for the year, plus you pay a 20% penalty on the amount you took out. So if you pull $1,000 to pay for a vacation, you owe income tax on that $1,000 at your regular rate plus an extra $200 penalty. Steep cost for treating your HSA like a regular savings account.

At 65, the 20% penalty goes away. You can withdraw HSA money for any reason without penalty, but you still owe ordinary income tax on non-medical withdrawals. This makes the HSA work kind of like a traditional IRA after 65. You get taxed on the way out if you don’t use the money for healthcare. But if you do use it for qualified medical expenses at any age, the withdrawal is completely tax-free. Most people treat the HSA as a medical fund first and a backup retirement account second, since the tax-free treatment for healthcare beats the taxable treatment for other spending. Common non-qualified expenses include cosmetic procedures that aren’t medically necessary, gym memberships, most health insurance premiums (except COBRA, unemployment coverage, long-term care, and Medicare), and funeral or burial costs.

How HSA Investments Work and When You Can Invest Your Balance

A lot of HSA providers let you invest part of your balance once you hit a minimum cash threshold. That’s usually somewhere between $500 and $2,000, depending on the provider. The idea is to keep enough cash around to pay near-term medical bills while investing the rest for long-term growth. Because HSA investment earnings grow tax-free and can be withdrawn tax-free for qualified expenses, the account works like a Roth IRA for healthcare. You never pay tax on the gains as long as you use the money for eligible costs.

Investment options vary. Most providers offer a menu of mutual funds, index funds, or ETFs that you pick and manage yourself. Some have target-date funds or model portfolios if you’d rather go hands-off. A few HSA providers partner with brokerage firms and offer a self-directed investment account, where you can buy individual stocks or a wider range of funds. Watch the fees. Some HSAs charge monthly maintenance fees, per-trade transaction fees, or higher fund expense ratios. Low-cost index funds are popular because they keep fees down and capture broad market growth over time.

If you don’t need your HSA money right away, investing the balance is one of the smartest ways to build a tax-advantaged medical fund for later. Even small amounts compound over decades. Invest $4,150 at an average annual return of 6% and it grows to roughly $13,300 in 20 years, all without paying taxes on the gains if you use it for healthcare. Common investment types in HSAs:

- Mutual funds, actively managed or index-tracking

- ETFs with low expense ratios

- Target-date funds that automatically adjust as you age

- Money market funds for conservative, low-risk growth

HSA Portability, Rollovers, Transfers, and Account Ownership

One of the best things about an HSA is that you own it. It’s not tied to your employer the way a 401(k) or health FSA often is. Change jobs, retire, leave the workforce for any reason? The HSA stays with you and all the funds remain available. No vesting schedule. Employer contributions become yours immediately once they’re deposited. The account never expires, and there’s no “use it or lose it” deadline at year-end. Funds roll over indefinitely, so you can build a huge balance over many years.

If you switch HSA providers, maybe your new employer uses a different bank or you find a better investment platform, you can move your balance without triggering taxes or penalties. The safest way is a trustee-to-trustee transfer, where your old HSA provider sends the money directly to your new provider. You can also do a rollover, where the old provider sends you a check and you deposit it into the new HSA within 60 days, but you’re only allowed one rollover per 12-month period. Trustee-to-trustee transfers have no limit and dodge the risk of missing the 60-day window, so they’re usually the better move.

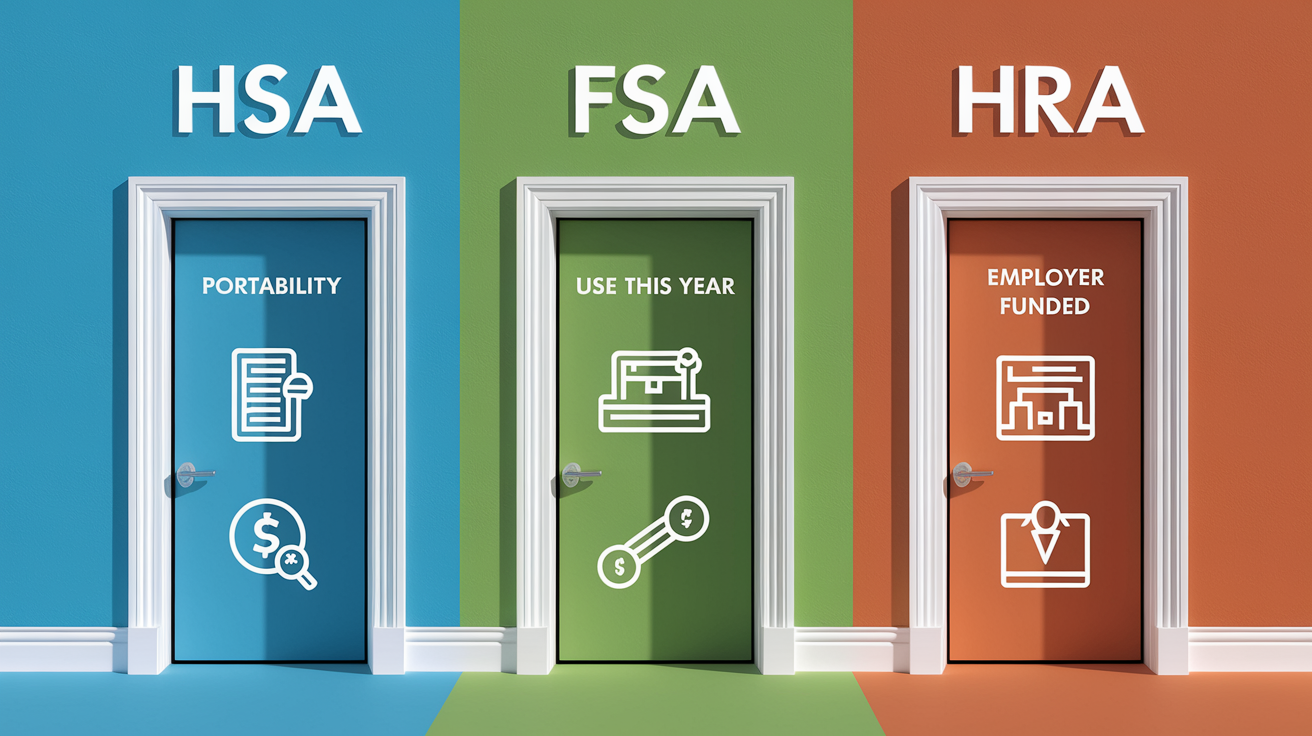

Comparing HSAs to FSAs and HRAs for Better Health Coverage Choices

Health savings accounts, flexible spending accounts, and health reimbursement arrangements all help pay for medical expenses with some kind of tax advantage, but the rules and flexibility are pretty different.

Key Differences Between HSAs and FSAs

An FSA is an employer-sponsored benefit that lets you set aside pre-tax money for medical expenses, but it’s got more restrictions. Most FSAs operate on a “use it or lose it” basis. Any money you don’t spend by the end of the plan year, or a short grace period or carryover amount if your employer allows it, gets forfeited. FSAs aren’t portable. Leave your job and you lose access to any remaining balance. You also can’t invest FSA funds. The contribution limit for a health FSA in 2024 was $3,200, lower than HSA limits, and you don’t need a high-deductible health plan to participate. But if you’re enrolled in a general-purpose health FSA, you can’t contribute to an HSA at the same time. Limited-purpose FSAs that cover only dental and vision are allowed alongside an HSA.

How HSAs Compare to HRAs

An HRA is funded entirely by your employer. You can’t put in your own money, and the employer sets all the rules: what’s covered, how much is available, and whether unused funds roll over or expire at year-end. Some HRAs are portable if you leave the company, but many aren’t. HRAs don’t require a high-deductible health plan, and there’s no investment option because the employer controls the account. The upside is that HRAs don’t count against your personal contribution limits. It’s employer money. The downside is you’ve got no control over funding or terms.

Choosing the Right Account for Your Health Plan

If you’re enrolled in a high-deductible health plan and want full control, portability, and the ability to invest for long-term growth, an HSA is usually the strongest pick. If your employer offers an FSA and you’re not HSA-eligible, or you expect to spend all the money within the year, the FSA’s pre-tax contributions are still valuable, but you lose the rollover and investment benefits. If your employer funds an HRA, you can use those dollars first and supplement with an HSA if you’re eligible.

| Account Type | Portability | Rollover | Investment Options | Who Owns Funds |

|---|---|---|---|---|

| HSA | Yes, stays with you | Yes, indefinitely | Yes, if provider offers | Employee |

| FSA | No, tied to employer | Limited or none | No | Employer |

| HRA | Depends on employer rules | Depends on employer rules | No | Employer |

Tax Reporting, Required Forms, and Recordkeeping for HSA Users

Every year, you’ll report your HSA activity to the IRS. If you get employer contributions, they show up on your W-2 in Box 12 with code W. That amount is just informational. It’s not included in your taxable wages. You’ll file IRS Form 8889 along with your Form 1040 to report your total contributions, any employer contributions, the amount you withdrew, and the amount you’re claiming as a deduction.

Your HSA provider sends you two forms. Form 1099-SA reports all the distributions you made during the year. Form 5498-SA reports the total contributions made to your HSA, including yours, your employer’s, and any third-party contributions. You use these forms to fill out Form 8889. The IRS matches the information, so accurate recordkeeping matters.

You’re responsible for keeping receipts and documentation for every withdrawal. The IRS doesn’t require you to submit receipts with your tax return, but they can ask for them during an audit. Store copies, digital or paper, of every medical bill, explanation of benefits, prescription receipt, and payment confirmation for at least three years. Some tax professionals say keep them for up to seven years or indefinitely if you plan to reimburse yourself later. If you’re reimbursing yourself years after an expense, the receipt proves the expense was qualified and happened after you opened the HSA. Key IRS forms you’ll work with for HSA reporting:

- Form 8889: Required annual filing to report contributions, distributions, and calculate your deduction.

- Form 1099-SA: Sent by your HSA provider to report the total amount distributed from your HSA.

- Form 5498-SA: Sent by your HSA provider to report the total contributions made during the tax year.

- W-2 Box 12 Code W: Shows employer HSA contributions, informational only, not taxable income.

Strategies to Maximize the Tax Benefits and Long-Term Value of an HSA

The simplest way to squeeze more value from an HSA is to contribute the max each year if you can swing it. Every dollar you put in reduces your taxable income, or it’s already pre-tax if done through payroll, and the savings stack up over time. If your employer offers any matching contributions, prioritize hitting that match. It’s free money and goes straight into your account.

If you don’t need your HSA funds right now, pay your medical bills out of pocket and leave the HSA balance invested. Save those receipts, and you can reimburse yourself years later, tax-free, while the account grows in the meantime. This “delayed reimbursement” move turns the HSA into a long-term investment vehicle. Contribute $4,150 and invest it at an average 6% annual return? The balance grows to roughly $13,300 in 20 years without any additional contributions. Use it for qualified medical expenses and that entire $13,300 comes out tax-free.

Once you hit 55, make sure to add the catch-up contribution every year. It’s an extra $1,000 you can stash away. After you turn 65, you can withdraw HSA money for any reason without the 20% penalty, though you’ll still owe income tax on non-medical withdrawals. This makes the HSA work like a backup retirement account. A lot of people use HSA funds to pay Medicare premiums, supplemental insurance, and long-term care expenses in retirement. Six practical tips to max out your HSA:

- Contribute early in the year so the money has more time to grow if invested.

- Capture any employer match first before contributing elsewhere.

- Invest any balance you won’t need in the next year or two. Choose low-cost index funds to keep fees down.

- Keep detailed records and receipts for every expense. Consider saving them digitally for easy long-term access.

- Skip withdrawing for non-qualified expenses before age 65. The penalty and taxes make it expensive.

- Use the HSA as part of your retirement plan, especially for healthcare costs in retirement, since medical expenses often spike with age.

How to Open and Manage an HSA Effectively

Opening an HSA is pretty straightforward once you confirm you’re enrolled in an HSA-eligible high-deductible health plan. Many employers offer an HSA as part of their benefits package and will set up an account for you automatically when you elect HDHP coverage. If your employer doesn’t offer an HSA, or you’d rather use a different provider with better fees or investment options, you can open one yourself at a bank, credit union, or specialized HSA provider.

To apply, you’ll need a photo ID, your Social Security number, and proof that you’re enrolled in an HSA-compatible HDHP. Often a copy of your insurance card or plan details works. Most applications happen online and take less than ten minutes. Once the account is open, you can fund it by linking your checking account for direct deposits or setting up payroll deductions through your employer if they support it. Many providers offer a debit card you can use to pay medical bills directly, and most have mobile apps that let you check your balance, view transactions, upload receipts, and manage investments from your phone.

Comparing HSA Providers: What to Look For

Not all HSA providers offer the same features or charge the same fees. Before you open an account, compare providers on these points:

- Monthly maintenance fees: Some charge $2 to $5 per month unless you keep a minimum balance. Others have no monthly fees at all.

- Investment options and minimums: Check what funds are available, what the minimum balance is before you can invest, and whether there are transaction fees for trades.

- Customer support and tools: Look for providers with easy-to-use mobile apps, clear online account access, receipt-upload features, and responsive customer service.

- Debit card and payment flexibility: Make sure the provider issues an HSA debit card and allows check-writing or online bill pay for medical expenses.

- Fee transparency: Review the full fee schedule for account transfers, paper statements, overdrafts, and fund expense ratios to dodge surprise costs.

Final Words

You can now see the flow: enroll in an HSA-eligible HDHP, open the account, fund it (you, your employer, or someone else), use it for qualified medical costs, keep receipts, and let unused funds roll over and grow.

If you still wonder how does health savings account work, remember HSAs offer tax benefits at contribution, growth, and qualified withdrawal. Use them for everyday care or let them build for the future — they’re flexible and quietly powerful for long-term health costs.

FAQ

Q: How much money should I put in my HSA per paycheck?

A: You should divide your target annual HSA contribution by your pay periods and contribute that amount per paycheck; prioritize covering expected medical costs and any employer match, then add more to build a long-term balance.

Q: What is the downside of having an HSA?

A: The downside of having an HSA is needing an HSA‑eligible high‑deductible plan, facing income tax plus a 20% penalty for nonqualified withdrawals before 65, plus possible fees and extra recordkeeping for receipts.

Q: Does HSA cover tretinoin?

A: HSA covers tretinoin when it’s a prescription for a qualified medical condition; if you use it only for cosmetic purposes it’s typically nonqualified. Keep the prescription and receipt for substantiation.

Q: How does an HSA work for dummies?

A: An HSA works by pairing an HSA‑eligible high‑deductible plan with a tax‑advantaged account: you contribute pre‑tax, funds grow tax‑free, withdraw tax‑free for qualified medical costs, and unused money rolls over and stays yours.