{kind=link}

Which matters more: paying less each month or being able to see any doctor you want?

At a glance, an HMO keeps your premiums and copays lower by requiring a primary care doctor who coordinates care and gives referrals for specialists, while a PPO lets you see any provider, including out‑of‑network doctors, but usually costs more.

This post breaks down the real differences, shows the money trade-offs, and helps you pick the plan that fits your health needs and budget.

Core Breakdown of HMO vs PPO Differences

An HMO (Health Maintenance Organization) locks you into a specific network of doctors and hospitals. You’ll pick a primary care physician who becomes your gatekeeper for everything. Need to see a specialist? Your PCP has to refer you first. Go out of network for anything that’s not an emergency, and you’re paying the whole bill yourself. The entire setup is built to keep care coordinated and costs down by controlling how you access services.

A PPO (Preferred Provider Organization) doesn’t box you in like that. You can see any provider you want, in or out of network, without getting permission first. Go straight to a specialist if you need one. See an out of network doctor if that’s who you trust. You’ll pay more for out of network care, but the plan won’t stop you. PPOs don’t make you choose a primary care physician either. You manage your own care and decide where to go.

Here’s the basic trade: HMOs cost less each month and when you use them, but you give up choice and deal with referrals. PPOs cost more upfront and at every visit, but you get freedom to see whoever you want without jumping through hoops.

| Feature | HMO | PPO |

|---|---|---|

| Primary care physician required | Yes | No |

| Referral needed for specialists | Yes | No |

| Out-of-network coverage | Emergency only | Covered, higher cost |

| Typical monthly premium | Lower | Higher |

| Typical copays and deductibles | Lower or none | Higher |

| Provider choice | In-network only | In- or out-of-network |

Operational Mechanics of HMO Plans Beyond the Basics

HMOs handle most of the paperwork for you. When you visit an in network doctor, they bill the HMO directly. You pay your copay at the visit and you’re done. No filing claims, no waiting for reimbursement. Your PCP coordinates everything, which means the plan knows what services you’ve had and can avoid ordering the same test twice or prescribing treatments that conflict. That coordination keeps costs low, but it also means you’ll need prior authorization for bigger services like imaging, surgery, or certain medications.

Prior authorization is just the plan checking that a service is medically necessary before it happens. Your PCP or specialist sends a request to the HMO, they review it, and if it’s approved, you’re covered as usual. If it’s denied, you can appeal or pay yourself. Most routine care doesn’t involve this step, but anything expensive or specialized probably will. Expect a short wait while the authorization goes through.

Out of network care isn’t really an option unless it’s an emergency. If you go to an out of network provider for routine stuff, you’re paying the full bill. The plan’s online directory tells you which doctors you can see. If a provider isn’t listed there, don’t expect coverage.

Your PCP isn’t just a doctor you see once a year. They’re your main contact for all health questions, they manage referrals, and they track your care history so nothing falls through the cracks. In network providers submit claims directly to the HMO, so you rarely see the billing process at all.

Operational Mechanics of PPO Plans Beyond the Basics

PPOs let you see anyone, but if you go out of network, you’re doing more of the work yourself. Out of network doctors might ask you to pay upfront, then you submit a claim to the PPO for partial reimbursement. The plan pays based on what they consider an “allowed charge,” and if the doctor’s bill is higher than that, you’re covering the difference. That’s called balance billing, and it can turn a $200 visit into a $400 one fast.

Even in network, some PPO services need prior authorization for expensive treatments, surgeries, or imaging. And your out of pocket costs are structured differently depending on whether you stay in network or not. You might have one deductible for in network care and a separate, higher one for out of network. Once you hit the deductible, you’ll pay coinsurance (usually a percentage of the bill) until you reach the annual out of pocket maximum.

Travel doesn’t really change how a PPO works. The network is usually big enough that you can find in network providers in most cities. But if you need a specific doctor who isn’t in the network, the out of network rules apply no matter where you are.

For out of network care, you often pay upfront and submit receipts to get reimbursed later. Out of network providers can charge more than the plan’s allowed amount, and you’re stuck with the difference. Many PPOs split deductibles between in network and out of network, with the out of network one being significantly higher.

Cost Differences Between HMO and PPO Health Plans

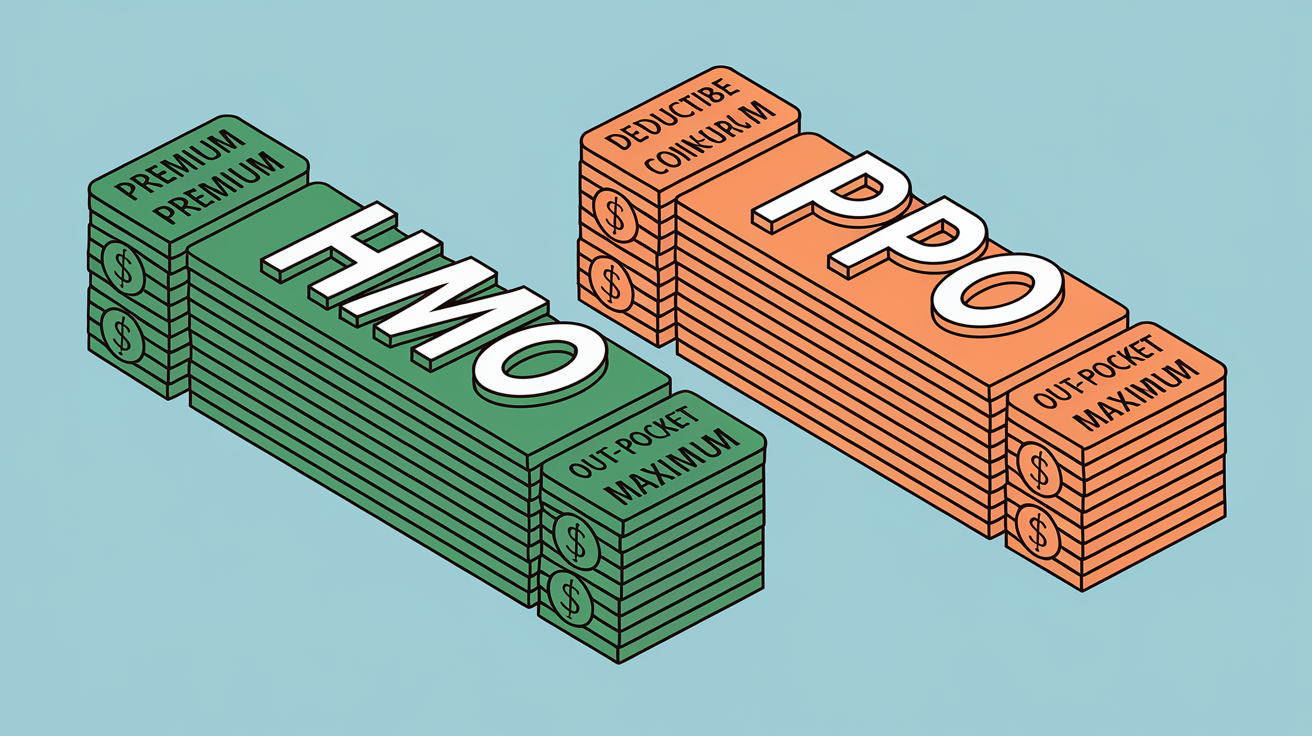

HMO plans cost less month to month and when you actually use care. Premiums are lower. Many HMOs charge a flat copay for doctor visits, often somewhere between $10 and $30, and you don’t have to meet a deductible before coverage kicks in. Prescription copays are lower too. Because the plan coordinates everything, you’re not getting duplicate tests or unnecessary referrals that jack up your spending. Stay in network and surprise bills are rare.

PPO plans cost more across the board. Higher premiums. Most PPOs make you meet an annual deductible before the plan starts sharing costs. After that, you’re paying coinsurance (commonly 20% of each bill) until you hit the plan’s out of pocket maximum. Use an out of network provider and the deductible is higher, the coinsurance is higher, and you’re exposed to balance billing if the doctor charges more than the plan allows.

Both plans cap your annual spending with an out of pocket maximum, but how you get there is completely different. In an HMO, costs are predictable and low as long as you follow the rules. In a PPO, costs swing wildly based on which providers you choose and whether you’ve met your deductible yet.

HMO monthly premiums are lower. PPO premiums are higher. HMOs often have low or no deductible. PPOs usually require a deductible, and it’s higher if you go out of network. HMO copays are low and fixed. PPO copays are higher or replaced by coinsurance. HMOs rarely use coinsurance. PPOs use it after the deductible is met, often 20% of the bill. HMOs don’t allow balance billing in network. PPOs allow it for out of network providers.

Pros and Cons of HMO vs PPO Plans

What works with HMOs:

You’re paying less each month. Copays for doctor visits and prescriptions stay low. Little or no deductible to worry about. Your care is coordinated, so you’re not getting duplicate tests or conflicting treatments. Costs are predictable if you stay in network.

What doesn’t work with HMOs:

You’re stuck in network for all routine care. Referrals are required to see specialists. Provider choice is limited. Out of network care isn’t covered except in emergencies. Prior authorization is required for many services.

What works with PPOs:

You can see any provider without referrals. Out of network care is covered, just at a higher cost. Broader provider network helps when you’re traveling. Easier access to specialists and second opinions.

What doesn’t work with PPOs:

Monthly premiums are higher. Deductibles and coinsurance are higher. Out of network visits often mean filing your own claims. Balance billing is a real risk when you use out of network providers. Less care coordination, which can lead to duplicate services or more administrative hassle.

How to Choose Between an HMO and PPO Plan

Start by figuring out whether saving money each month matters more than having unlimited provider choice. If your health is stable, you see the same primary care doctor regularly, and you’re fine with getting referrals for specialists, an HMO keeps your premiums and copays low. If you’ve got a specialist you need to keep seeing, you travel a lot for work, or you want to skip the referral step and go straight to a specialist, a PPO gives you that flexibility. But you’re paying more for it.

Don’t just compare premiums. Look at the deductible, the copays for the services you actually use, and the out of pocket maximum. If you’ve got a chronic condition that needs multiple specialist visits, a PPO’s higher premium might actually cost less overall than paying for out of network care under an HMO. If you rarely see doctors and want low monthly costs, the HMO is safer.

How often do you see doctors or specialists each year? Do you have a specialist or doctor you want to keep who may be out of network? Are you comfortable coordinating your care through a primary care physician? Do you travel often and need access to providers in multiple cities?

What are the exact deductible amounts for in network and out of network care in each plan? What are the copays for office visits, urgent care, and prescriptions? What’s the annual out of pocket maximum for each plan, and how quickly would you hit it based on your typical health needs?

Real Life Scenarios Comparing HMO and PPO Outcomes

Budget focused family:

A family with two young children needs regular checkups, occasional urgent care visits, and prescriptions for asthma. They go with an HMO. $50 monthly premium, $20 copays for pediatrician visits, no deductible. The PCP coordinates all care, and referrals to specialists are rare. Total annual cost for premiums and copays is around $900. Predictable expenses, no surprise bills.

Frequent traveler with existing specialists:

A consultant travels weekly for work and already sees a cardiologist and physical therapist who aren’t in most HMO networks. They pick a PPO. $180 monthly premium, $1,500 in network deductible. The flexibility to see out of network providers while traveling and keep their existing specialists is worth the higher cost. Annual cost for premiums, deductibles, and coinsurance is around $3,200, but the plan covers care in every city they visit.

Chronic condition requiring multiple specialists:

Someone managing diabetes sees an endocrinologist, podiatrist, and dietitian quarterly. Under an HMO, each specialist visit requires a PCP referral, but copays are only $25 per visit and prescriptions cost $10 per fill. Under a PPO, no referrals are needed, but the deductible is $2,000 and coinsurance is 20% after that. The HMO saves this person about $1,800 annually because coordinated care keeps costs low and the referral process is simple for routine specialist visits.

Final Words

We compared how HMOs keep care in-network through a primary care physician and referrals, while PPOs give direct specialist access and out-of-network options without referrals. The piece defined each plan and showed the core trade-off.

We walked through how each plan works day-to-day, the cost differences, and the pros and cons. The how-to-choose checklist and scenarios helped match plans to real needs.

If you’re deciding, weigh cost versus flexibility. Understanding the difference between hmo and ppo makes the choice clearer. You’re on the right track.

FAQ

Q: Which is better, a PPO or HMO plan?

A: The better plan between a PPO and HMO depends on whether you want lower monthly and out-of-pocket costs with tighter network rules (HMO) or more provider choice and out-of-network access (PPO).

Q: What are three disadvantages of HMO?

A: Three disadvantages of an HMO are limited provider choice, needing a primary care physician and referrals for specialists, and little to no out-of-network coverage except in emergencies.

Q: What is the downside to a PPO plan? Why do doctors prefer PPO over HMO?

A: The downside to a PPO plan is higher premiums, larger deductibles, and balance-billing risk; doctors often prefer PPOs because they allow easier specialist access and more flexible payment arrangements.