{kind=link}

Think all Medigap plans give the same protection?

They have standardized benefits by letter, but what you pay and what you might still owe can differ a lot—sometimes hundreds of dollars a year.

This guide compares popular options like Plan G and Plan N, explains the most important coverage differences, and shows how pricing methods and enrollment timing affect your cost.

Read on to learn the simple checks that save money and help you avoid surprise medical bills.

Understanding the Purpose and Structure of Medigap Coverage

Medigap, officially called Medicare Supplement Insurance, is private health insurance you buy to cover costs that Original Medicare (Part A and Part B) doesn’t pay. You’re buying it from a private company, not the government. It works alongside Medicare to fill in the gaps—things like deductibles, coinsurance, and copays that can pile up fast when you need care.

Here’s what matters most about Medigap: benefits are standardized by the federal government in most states. Every insurance company selling Medigap Plan G has to offer identical benefits under that letter. What changes? The monthly premium. This makes shopping easier because you’re comparing price for the same coverage, not trying to decode different benefit packages.

Medigap only works if you’re enrolled in Original Medicare Part A and Part B. You can’t use it with a Medicare Advantage plan (Part C), and you can’t have both at the same time. You’ll pay a separate monthly premium for Medigap on top of your Part B premium.

Medigap is designed to cover these gaps in Original Medicare:

- Part A hospital coinsurance for extended stays (days 61 to 90 and lifetime reserve days)

- Part B coinsurance or copayment (usually 20% of the Medicare approved amount)

- Medicare Part A deductible for hospital inpatient stays

- Skilled nursing facility care coinsurance

- First three pints of blood each year

Standardized Medigap Plan Options and What Each Letter Covers

Most states offer ten standardized Medigap plan letters: A, B, C, D, F, G, K, L, M, and N. Each letter represents a defined set of benefits. Every insurance company has to offer the same benefits for a given plan letter. What changes from company to company? The monthly premium and customer service. The coverage itself is identical.

Not all plans are available to everyone. Plans C and F aren’t sold anymore to people who became eligible for Medicare on or after January 1, 2020. This came from a 2015 federal law that stopped new Medigap policies from covering the Medicare Part B deductible. If you were eligible before that date, you can still buy or keep Plan C or F.

| Plan Letter | Covers Part A Deductible? | Covers Part B Excess Charges? | Skilled Nursing Coverage? | Foreign Travel Emergency? |

|---|---|---|---|---|

| A | No | No | No | No |

| B | Yes | No | No | No |

| C | Yes | No | Yes | Yes (80% after $250 deductible) |

| D | Yes | No | Yes | Yes (80% after $250 deductible) |

| F | Yes | Yes | Yes | Yes (80% after $250 deductible) |

| G | Yes | Yes | Yes | Yes (80% after $250 deductible) |

| K | 50% coverage | No | 50% coverage | No |

| L | 75% coverage | No | 75% coverage | No |

| M | 50% coverage | No | Yes | Yes (80% after $250 deductible) |

| N | Yes | No | Yes | Yes (80% after $250 deductible) |

Key Coverage Details and 2025 Medigap Benefit Amounts

All Medigap plans cover the 20% Part B coinsurance for most physician visits and outpatient services. They also cover Part A hospital coinsurance for days 61 through 90 of an inpatient stay, which costs $419 per day in 2025. If you use your lifetime reserve days (an extra 60 days available after day 90 of a single benefit period), the coinsurance jumps to $838 per day in 2025. Medigap plans with hospital coinsurance coverage pay these amounts in full.

The Medicare Part A deductible is $1,676 per benefit period in 2025. Many Medigap plans cover this, though some (like Plan A and the cost sharing Plans K and L) don’t pay the full amount or skip it entirely. The Medicare Part B deductible is $257 in 2025. Because of the 2015 law change, no Medigap plan sold to someone first eligible for Medicare after January 1, 2020, can cover it.

Medigap plans also cover the first three pints of blood you might need each year. Some plans add coverage for skilled nursing facility coinsurance, hospice coinsurance, Part B excess charges (when a doctor bills up to 15% above the Medicare approved amount), and foreign travel emergency care. Coverage for these depends on which plan letter you choose.

When you’re comparing Medigap plans, focus on these six coverage areas:

- Part A hospital deductible and coinsurance

- Part B coinsurance and copayments

- Part B excess charges (matters if you see doctors who don’t accept Medicare assignment)

- Skilled nursing facility coinsurance

- Foreign travel emergency coverage (if you travel outside the U.S.)

- Annual out of pocket limits (only available on Plans K and L)

Enrollment Windows, Open Enrollment Rules, and Guaranteed Issue Protections

The best time to buy a Medigap policy is during your six month Medigap Open Enrollment Period. This window starts on the first day of the month you turn 65 and are enrolled in Medicare Part B. During this period, insurance companies have to sell you any Medigap policy they offer, no matter your health. They have to charge you their best available rate for your age. They can’t use medical underwriting to deny you or jack up your price.

Outside this six month window, most insurance companies in most states can ask about your health history, decline your application, or charge higher premiums based on your medical conditions. Some states don’t allow this, but in most places you lose the guaranteed protections once your initial enrollment period ends.

You can also gain guaranteed issue rights in specific situations. When you have guaranteed issue rights, you can buy certain Medigap plans without medical underwriting, even outside your initial enrollment period. These rights usually last for 63 days after the event that triggers them. You’ve got to act quickly.

Here are six common situations that may give you guaranteed issue rights:

- You’re leaving a Medicare Advantage plan because the plan is leaving Medicare or you moved out of the plan’s service area.

- Your employer group health coverage (or a union or COBRA plan) is ending.

- You lose coverage through no fault of your own (for example, an insurer goes bankrupt).

- You tried a Medicare Advantage plan for the first time when you became eligible for Medicare, and you’re canceling it within the first year.

- You joined a Medicare Advantage plan when you first enrolled in Medicare Part B, and within one year the plan violated its contract or misled you.

- Your Medigap insurance company goes out of business or stops offering your plan in your area.

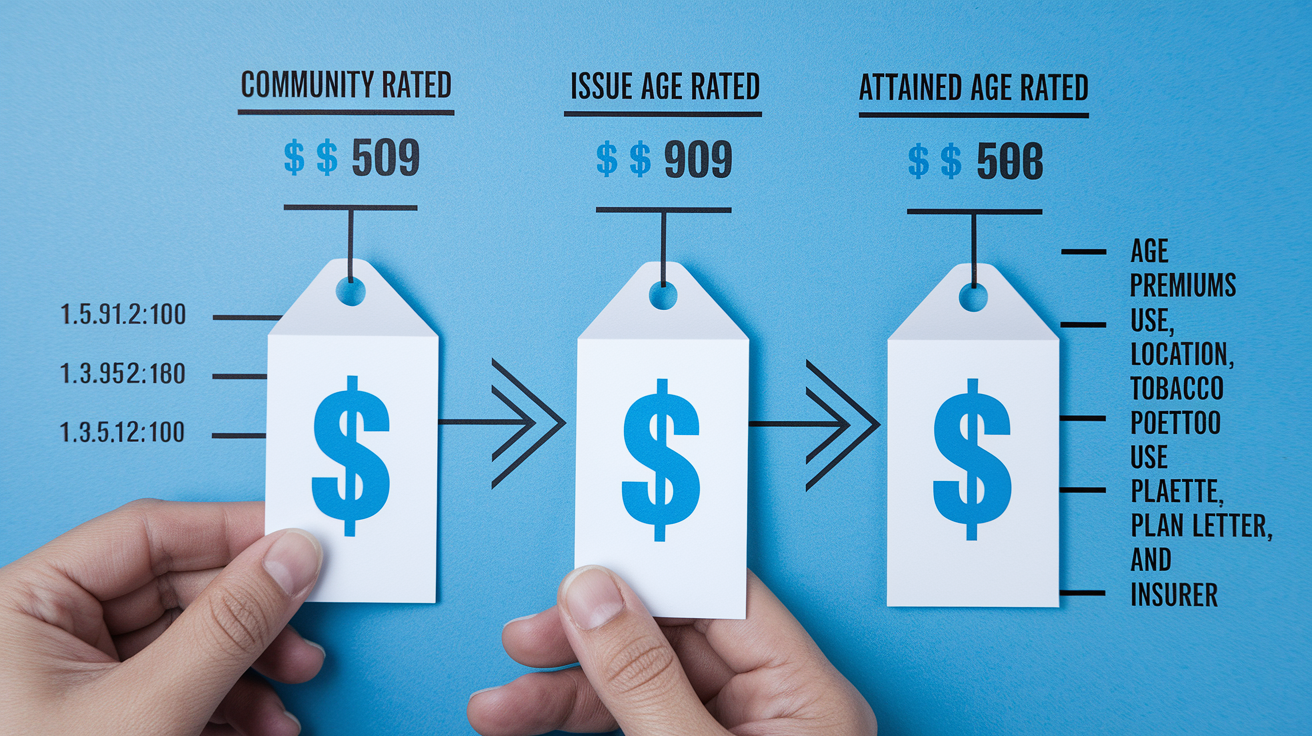

Pricing Structure and How Medigap Premiums Are Calculated

Medigap premiums vary a lot even for identical coverage. Two companies selling Plan G in the same ZIP code can charge very different monthly amounts because insurers set their own rates. Pricing differences can reach hundreds of dollars per year, so comparing quotes from multiple companies is one of the smartest things you can do.

Insurance companies use three main pricing methods. Community rated (also called no age rated) premiums are the same for everyone enrolled in the plan, no matter your age. Issue age rated premiums are based on your age when you first buy the policy and don’t increase as you get older, though they can still rise because of inflation or other factors. Attained age rated premiums start lower but increase as you age, in addition to any inflation adjustments. The pricing method a company uses has a long term effect on what you’ll pay, so ask before you buy.

These are the five main factors that influence your Medigap premium:

- Your age (and the pricing method the insurer uses)

- Where you live (premiums vary by ZIP code and state)

- Whether you use tobacco

- Which plan letter you choose (Plan G typically costs more than Plan N)

- The insurance company you select

Plan G, Plan N, and Alternatives to Plan F for New Enrollees

Plan F used to be the most comprehensive Medigap option, covering every allowable gap in Medicare including the Part B deductible. That plan is closed now to anyone who became eligible for Medicare on or after January 1, 2020. For people shopping today, Plan G offers nearly the same coverage as Plan F, with one difference: Plan G doesn’t cover the $257 Part B deductible in 2025. You pay that amount once per year out of pocket, then Plan G covers the rest.

Plan N is a popular lower premium alternative. It covers the Part A deductible and most other major gaps, but it requires you to pay up to $20 for some doctor visits and up to $50 for emergency room visits (the ER copay is waived if you’re admitted to the hospital). Plan N might also leave you responsible for Part B excess charges, which can cost up to 15% more than the Medicare approved amount if your doctor doesn’t accept assignment. Most doctors do accept assignment. Several states (including Connecticut, Massachusetts, Minnesota, New York, Ohio, Pennsylvania, Rhode Island, and Vermont) don’t allow excess charges at all.

Choosing between Plan G and Plan N comes down to how much you value predictability. Plan G offers simpler, more comprehensive protection with fewer surprise costs. Plan N trades small copays and the risk of excess charges for a lower monthly premium.

These are the main differences to weigh:

- Plan G covers Part B excess charges. Plan N typically doesn’t.

- Plan N requires copays for doctor visits and ER visits. Plan G doesn’t.

- Plan G premiums are usually higher than Plan N.

- Both plans cover the Part A deductible, skilled nursing coinsurance, and foreign travel emergency care.

High Deductible Medigap Options and Cost Saving Models

Some insurers offer high deductible versions of Plan G (and Plan F, if you were eligible for Medicare before January 1, 2020). These plans charge much lower monthly premiums but require you to pay a higher deductible before coverage begins. In 2025, the high deductible amount is $2,870. You pay all Medicare covered costs out of pocket until you reach that annual threshold, then the plan covers the same benefits as the standard version of the plan letter.

High deductible Medigap works well if you expect low or predictable medical expenses and want to lower your monthly insurance costs. The premium savings can be substantial, sometimes several hundred dollars per year compared to a standard plan. If you rarely visit the doctor or need tests, you might come out ahead even after paying the deductible.

Here’s a simple scenario. Imagine you’re paying $200 per month for standard Plan G, or $2,400 per year. A high deductible Plan G might cost $60 per month, or $720 per year. If your out of pocket medical costs stay below $2,870 for the year, you save $1,680 in premiums minus whatever you actually spent. If you hit the $2,870 deductible, your total annual cost (premium plus deductible) is $3,590, compared to $2,400 in premiums alone on the standard plan. So in a high cost year, the standard plan is cheaper. In a low cost year, the high deductible plan wins.

State Specific Medigap Variations and Regulatory Differences

Most states follow the standardized ten plan system, but a few have their own rules. Massachusetts, Minnesota, and Wisconsin use different Medigap structures that don’t align with the national plan letters. If you live in one of those states, you’ll need to review the state specific options to understand what’s available.

Some states offer stronger consumer protections. Connecticut, Massachusetts, and New York require insurers to sell Medigap policies to eligible applicants at any time during the year, regardless of health status or pre existing conditions. Maine allows a one month annual guaranteed issue period for Plan A. Several states have adopted “birthday rules” that let you switch Medigap plans once per year around your birthday without medical underwriting. States with birthday rule protections include California, Idaho, Illinois, Kentucky, Louisiana, Maryland, Nevada, Oklahoma, Oregon, Utah, Virginia, and Wyoming. Indiana’s birthday rule takes effect in 2026, and Minnesota enacted annual guaranteed issue protections that start August 1, 2026.

If you move to a new state, your Medigap policy stays in force, but rules about switching or buying a new policy can change. Some states restrict which plans you can switch to or require underwriting if you want to change carriers after moving in.

Changing, Switching, or Replacing Medigap Plans

You can apply to switch Medigap plans at any time, but unless you live in a state with special protections or you have guaranteed issue rights, the new insurer can require medical underwriting. That means they can ask about your health, review your medical history, and potentially deny your application or charge you more based on your conditions. Some companies might also impose a waiting period of up to six months for coverage of pre existing conditions.

In states with birthday rules or annual switch windows, you can change plans without answering health questions during a specific time each year. These state protections make it easier to move to a lower cost policy or switch carriers if you’re unhappy with service. Medicare Select plans, which require you to use specific network providers for non emergency care, include a 12 month right to switch to a standard Medigap plan if you decide the network limits don’t work for you.

If you’re considering a switch, follow these steps:

- Confirm your new policy is approved and will start before you cancel your current plan.

- Compare the new plan’s benefits and premium to what you have now, including any potential rate increases down the road.

- Ask whether the new insurer will require underwriting or impose a waiting period.

- Review your state’s rules to see if you have guaranteed issue or birthday rule protections.

- Keep your current Medigap plan active until the new coverage officially begins.

How to Evaluate Insurance Companies and Compare Medigap Quotes

(((alt-img10)))

Because Medigap benefits are standardized, the two things that matter most when choosing a policy are price and the company’s reputation. A Plan G from one insurer covers exactly the same services as a Plan G from another, so you want the lowest premium from a financially stable company with good customer service.

Start by getting quotes from at least three to five insurers in your area. Many state insurance departments and the federal Medicare.gov website offer Medigap premium comparison tools that let you search by ZIP code, age, gender, tobacco use, and plan letter. These tools show estimated monthly premiums side by side. Premium differences of $50 or more per month for the same plan are common.

Once you identify the lowest cost options, check the insurer’s financial strength and complaint history. Look for ratings from agencies like A.M. Best or Standard & Poor’s, which evaluate whether a company has the resources to pay future claims. Your state insurance department website often publishes complaint ratios, showing how many complaints an insurer receives relative to its market share. A company with a low premium but a high complaint ratio might not be worth the savings.

Here are four steps for comparing companies and quotes:

- Use an online comparison tool or call your State Health Insurance Assistance Program (SHIP) for help finding quotes in your area.

- Request quotes for the same plan letter from multiple insurers to ensure you’re comparing apples to apples.

- Ask each company which pricing method it uses (community rated, issue age rated, or attained age rated) and how premiums might increase over time.

- Review the insurer’s financial ratings and complaint history before making a final decision.

Final Words

You can see how Medigap fills the cost gaps left by Original Medicare and why the standardized plan letters matter. We covered what each letter generally pays, 2025 cost figures, enrollment timing and protections, pricing methods, and alternatives like Plan G, Plan N, and high‑deductible options.

Next, compare quotes by ZIP code, check your open‑enrollment window, and weigh trade‑offs like premiums versus out‑of‑pocket risk.

With those steps, you’ll be ready to compare medigap plans and choose one that fits your health needs and budget.

FAQ

Q: What is the downside to Medigap plans?

A: The downside to Medigap plans is that they add a separate monthly premium on top of Medicare Part B, can’t be used with Medicare Advantage, and premiums or underwriting can be costly outside open enrollment.

Q: What is the most popular Medigap plan?

A: The most popular Medigap plan is Plan G, because it covers nearly all Original Medicare gaps except the Part B deductible and is widely available after Plan F closed to new enrollees.

Q: What is the average cost of a Medicare Medigap plan?

A: The average cost of a Medicare Medigap plan varies by state, age, and carrier; expect roughly $100–$300 per month, so compare local quotes to find the exact premium for your situation.

Q: What is the difference between Medigap and a Medicare Supplement?

A: The difference between Medigap and a Medicare Supplement is none: Medigap is the common name for Medicare Supplement insurance, which helps pay gaps in Original Medicare coverage.