{kind=link}

Think your mortgage or your home’s market value tells you how much insurance you need?

Choosing limits that are too low can leave you paying tens of thousands after a fire, storm, or lawsuit.

This post shows new homeowners exactly how much coverage to set for dwelling (rebuild cost), personal property, liability, additional living expenses, and deductibles, using simple rules of thumb and clear examples so you’re not underinsured on day one.

Determining the Right Coverage Amounts for a New Homeowner

Homeowners insurance protects you against financial loss from fire, theft, liability lawsuits, and dozens of other covered perils. But only if your policy limits match your actual risk. The coverage amounts you choose determine how much the insurer will pay after a covered loss, so picking the right limits from day one prevents painful out-of-pocket shortfalls when you file a claim.

Industry benchmarks and lender requirements provide a starting point. Dwelling coverage should equal your home’s full replacement (rebuild) cost, not its market value. Personal property limits are usually 50–70% of your dwelling coverage. Liability coverage starts at $100,000, but financial experts often recommend $300,000–$500,000 to protect your savings and future earnings. Additional Living Expenses (sometimes called Loss of Use) are typically set at 10–20% of dwelling coverage or 12–24 months of temporary housing costs. Most mortgage lenders require coverage that meets or exceeds the replacement cost of the home and at least 80% of that rebuild value to satisfy the coinsurance rule.

Use these numerical rules to set your initial policy limits:

Dwelling (Coverage A) = square footage × local rebuild cost per sq ft + 10–25% for permits, code upgrades, and debris removal

Personal Property (Coverage C) = 50–70% of dwelling coverage, adjusted higher if you own expensive furniture, electronics, or collections

Other Structures (Coverage B) = 10% of dwelling coverage (raise it if you have a large detached garage, workshop, or barn)

Liability (Coverage E) = at least $300,000; consider $500,000 if you have significant assets, a pool, or host frequent gatherings

Medical Payments (Coverage F) = $1,000–$5,000 (pays minor injury claims for guests regardless of fault)

Additional Living Expenses (Coverage D) = 10–20% of dwelling coverage or local monthly rent × 12–24 months

Calculating Home Rebuild Costs and Setting Dwelling Coverage

Dwelling coverage (also called Coverage A) pays to repair or rebuild your home after a covered loss. This limit should reflect how much it’ll cost to rebuild your house from the ground up today, which is almost always different from your home’s market value or your mortgage balance. A home in a desirable neighborhood might sell for $500,000 but only cost $350,000 to rebuild, while a modest older home in a high construction market could cost more to rebuild than you paid for it.

To calculate your replacement cost estimate, multiply your home’s heated living area (in square feet) by the current local rebuild cost per square foot, then add 10–25% to cover building code upgrades, contractor overhead, permit fees, and debris removal. Extended replacement cost endorsements add a percentage cushion (often 25%) above your dwelling limit, so if building costs spike unexpectedly you’re still covered. Guaranteed replacement cost endorsements go even further and promise to pay the full rebuild cost no matter what it takes, though these policies are becoming rare and cost significantly more.

Follow these steps to set your dwelling limit:

-

Get a local rebuild cost estimate. Use your insurer’s dwelling coverage calculator, request a quote from a local contractor, or search regional cost per square foot data (often $100–$300/sq ft depending on finishes and location).

-

Multiply square footage by cost per sq ft. Example: 2,000 sq ft × $150/sq ft = $300,000.

-

Add a buffer for code upgrades and debris removal (10–25%). Example: $300,000 + 20% = $360,000.

-

Adjust after major renovations or every few years. Replacement costs rose 5.2% from April 2024 to April 2025 nationally, so even small annual jumps compound quickly.

Setting the Right Personal Property Coverage Limits

Personal property coverage (Coverage C) pays to replace or repair your belongings after theft, fire, or other covered perils. Insurers automatically set this limit at 50–70% of your dwelling coverage, but that default may not fit your situation. A couple who recently graduated and rents furniture might need only 40%, while a family with high end appliances, musical instruments, and a full home office should choose 70% or create a separate inventory to confirm the total value.

Replacement cost coverage pays to buy new items at today’s prices, while actual cash value (ACV) subtracts depreciation and leaves you with a fraction of what you originally paid. ACV for a five year old laptop might be $200 even though a new equivalent model costs $900. Always choose replacement cost coverage for personal property. The premium difference is modest and depreciation reductions can be devastating after a major loss. Keep a detailed digital inventory with photos, receipts, descriptions, and estimated replacement costs stored in the cloud so you have proof if you ever need to file a claim.

Follow these inventory best practices to confirm your personal property limit is adequate:

Photograph or video every room, open closets and drawers, and zoom in on serial numbers and brand labels

Save receipts and appraisals for expensive items (furniture, electronics, jewelry, art, collectibles)

Use a spreadsheet or home inventory app to list each item, purchase date, original cost, and current replacement cost

Store a copy off site (cloud storage, email to yourself, or with a trusted family member)

Update your inventory after major purchases, inheritances, or gifts

Choosing Liability Coverage and Deciding Whether to Add an Umbrella Policy

Liability coverage (Coverage E) protects you if someone is injured on your property or if you accidentally damage someone else’s property and they sue you. It pays legal defense costs, settlements, and court judgments up to your policy limit. Standard policies often start at $100,000, but that amount evaporates quickly in a serious lawsuit. Medical bills, lost wages, and pain and suffering awards routinely exceed six figures.

Financial advisors commonly recommend carrying liability coverage equal to your net worth or at least $300,000–$500,000. If you have a swimming pool, trampoline, certain dog breeds, or you host large gatherings, your risk of a liability claim increases. If your assets, savings, or expected future earnings exceed $500,000, add a personal umbrella policy that starts where your homeowners liability stops. Umbrella policies typically begin at $1,000,000 in coverage and cost roughly $150–$300 per year for that first million.

Medical payments to others (Coverage F) is a small companion coverage, usually $1,000–$5,000, that pays minor injury expenses for guests regardless of who was at fault. It’s designed to avoid lawsuits over twisted ankles or minor cuts by reimbursing medical bills quickly and without admitting liability. Most homeowners leave this at the insurer’s default $5,000 because the premium impact is negligible and goodwill with an injured visitor can prevent a larger claim later.

Additional Living Expenses Coverage and Temporary Housing Needs

Additional Living Expenses (ALE), also called Loss of Use or Coverage D, reimburses you for hotel bills, rental housing, restaurant meals, storage fees, and extra commuting costs while your home is uninhabitable after a covered loss. Policies commonly set this limit at 10–20% of your dwelling coverage or define a time window such as 12–24 months of actual incurred costs, whichever comes first.

To check whether your ALE limit is realistic, estimate what it would cost to rent a comparable home or stay in extended stay lodging in your area for six to twelve months. Add daily meal costs (if you normally cook at home, eating out every day gets expensive quickly) and any extra transportation if the temporary housing is farther from work or school. A $360,000 dwelling with a 20% ALE limit provides $72,000, which might cover six months in a moderate cost area or only three months in a high rent city. Run the numbers against your local costs to be sure.

Common expenses covered under ALE include:

Hotel or short term rental housing at a comparable standard to your home

Increased meal costs (restaurant and takeout expenses above your normal grocery spending)

Storage unit rental for furniture and belongings while repairs are underway

Understanding Deductibles and How They Affect Premiums

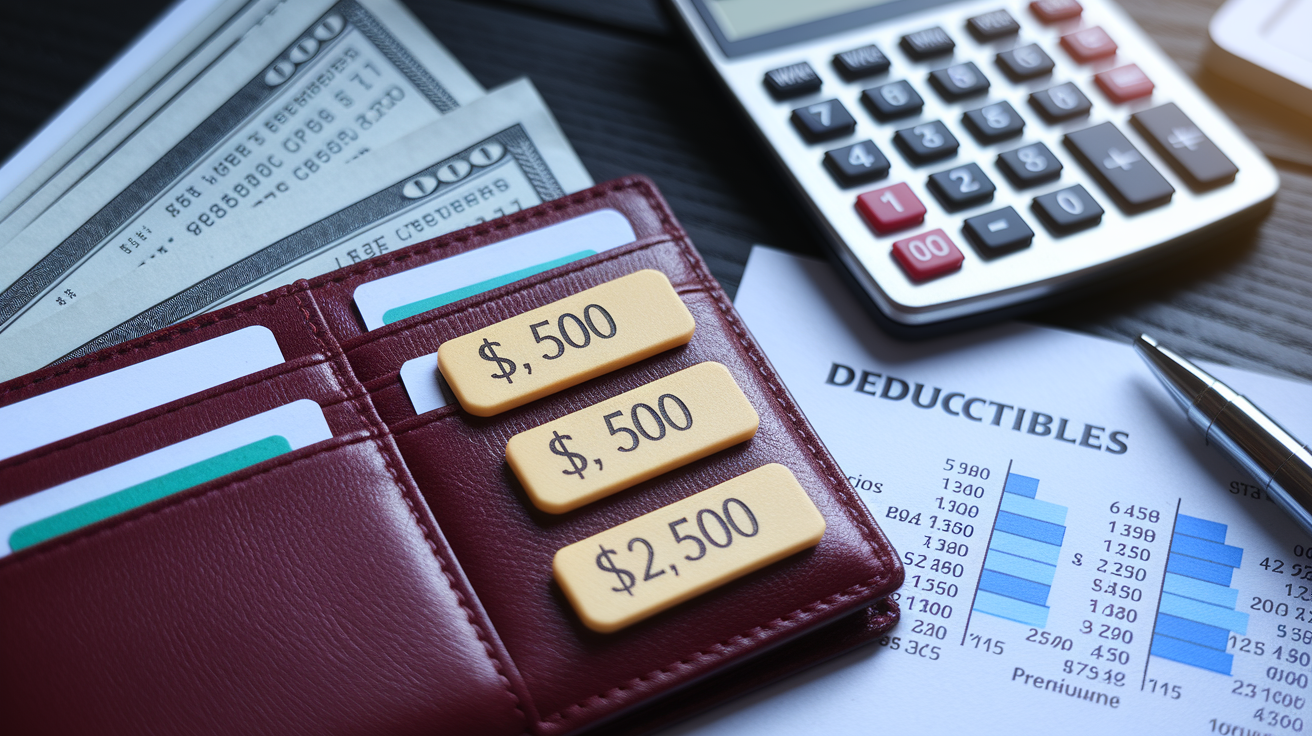

Your deductible is the amount you pay out of pocket before the insurance company starts paying on a covered claim. Common homeowners deductibles are $500, $1,000, and $2,500. Choosing a higher deductible lowers your annual premium because you’re agreeing to cover more of the loss yourself. The trade off is straightforward: a lower deductible gives you more immediate claim help but costs more every year, while a higher deductible saves premium dollars but requires a bigger emergency fund.

Hurricane, windstorm, hail, and earthquake deductibles are often expressed as a percentage of your dwelling coverage rather than a flat dollar amount. A 2% hurricane deductible on a $400,000 dwelling means you pay the first $8,000 of wind damage out of pocket, and a 5% earthquake deductible on a $300,000 home means a $15,000 deductible before coverage kicks in. Percentage deductibles can create sticker shock, so confirm what your policy uses and whether you have the savings to cover that amount after a disaster.

Consider these three trade off tips when setting your deductible:

-

Raise your deductible to $1,000 or $2,500 if you have at least six months of living expenses in savings. The annual premium savings often pay back the higher deductible within a few claim free years.

-

Keep a lower $500 deductible if cash flow is tight or you live in a high risk area where small claims are common (hail, windstorms, frequent severe weather).

-

Confirm separate percentage deductibles for wind, hurricane, or earthquake and set aside a dedicated fund equal to that percentage of your dwelling coverage so you’re not caught short.

Evaluating Special Endorsements and Filling Common Coverage Gaps

Standard homeowners policies exclude flood, earthquake, and several other perils, so you’ll need separate coverage or endorsements to close those gaps. Flood insurance is available through the National Flood Insurance Program (NFIP) with limits up to $250,000 for the building and $100,000 for contents, or through private insurers who sometimes offer higher limits and additional features. Even homes outside high risk flood zones can flood, and mortgage lenders in Special Flood Hazard Areas require flood coverage.

Earthquake coverage is sold as a separate policy or endorsement and typically comes with high percentage based deductibles, often 2–20% of your dwelling coverage. Sewer and water backup endorsements add $1,000–$25,000 of coverage for damage caused by drains, sewers, or sump pump failures. This is not the same as flood coverage and addresses a common exclusion. Scheduled personal property (also called a valuable items endorsement) overcomes the standard sublimits on jewelry, watches, art, collectibles, and musical instruments. For example, if your policy caps jewelry theft at $1,500 but you own a $5,000 engagement ring, scheduling the ring individually raises the limit to its appraised value.

Five key endorsements and typical coverage amounts to consider:

Flood insurance (NFIP or private): $250,000 building / $100,000 contents (NFIP maximums); private policies can go higher

Earthquake endorsement: varies by location; deductibles commonly 10–20% of dwelling coverage in high seismic zones

Sewer and water backup: $5,000–$25,000 per occurrence

Scheduled personal property (jewelry, fine art, cameras, instruments): actual appraised value per item, with no deductible on scheduled items

Service line coverage: $5,000–$10,000 for underground utility line repair (water, electric, sewer, data) on your property

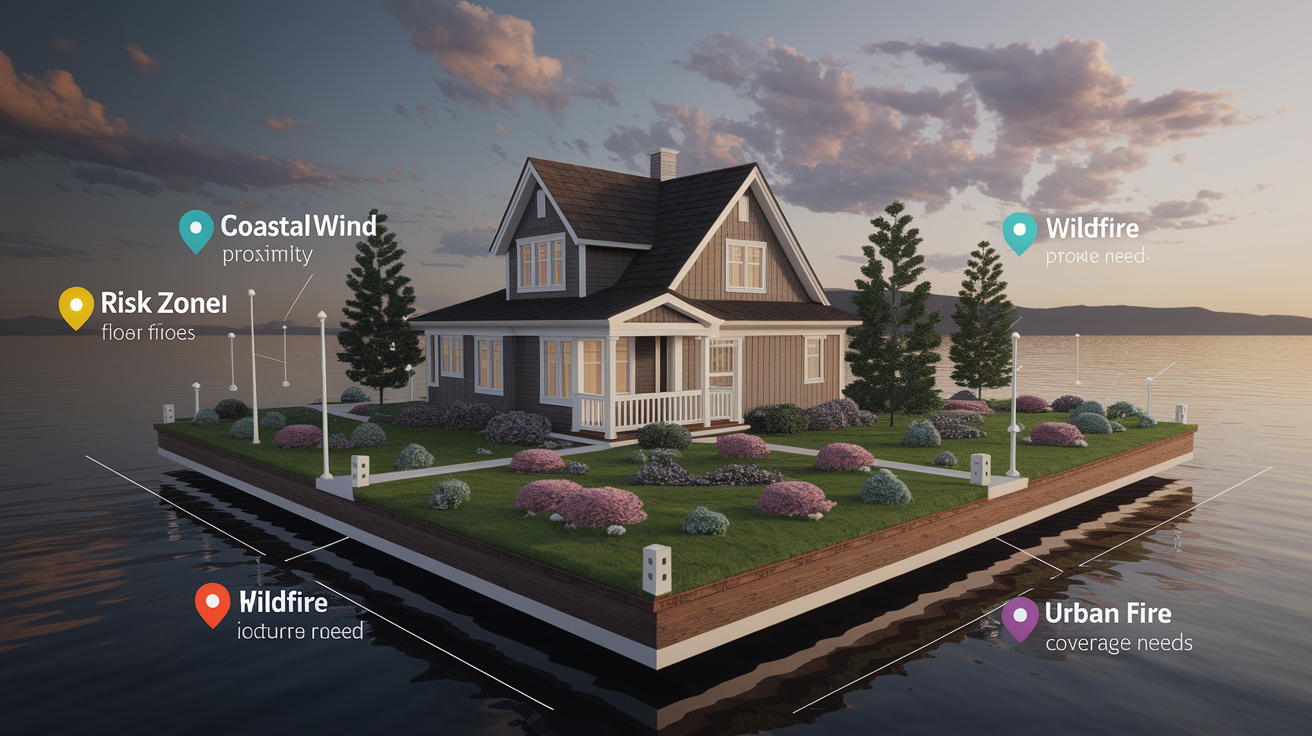

Coverage Considerations for Location, Home Features and Risk Factors

Where you live and the characteristics of your home directly change both the price of your policy and the amount of coverage you need. Homes in coastal wind zones, wildfire prone areas, or flood plains face higher premiums, mandatory percentage deductibles, and stricter insurer underwriting. Proximity to a fire station and nearby hydrants lowers your premium because the fire department can respond faster and limit damage, while a rural home miles from the nearest hydrant may cost significantly more to insure.

Roof age and condition are among the most scrutinized factors during underwriting. A roof older than 15–20 years may trigger an inspection requirement, a depreciation schedule that reduces claim payouts, or outright policy non renewal until you replace it. Wind and hail damage to old roofs is often paid on an actual cash value basis even when the rest of your dwelling coverage is replacement cost, leaving you responsible for a large share of the repair bill.

| Factor | Effect on Coverage Needs |

|---|---|

| Coastal or high wind zone | Requires hurricane/windstorm deductible (1–5% of dwelling); may need separate wind policy |

| Flood zone (FEMA A or V) | Lender mandates separate flood insurance; recommend $250,000 building coverage minimum |

| Wildfire prone area | Higher rebuild cost inflation; insurer may require brush clearance or decline coverage |

| Older roof (15+ years) | Roof damage may pay ACV instead of replacement cost; consider roof endorsement or replacement |

How Renovations, Upgrades, and Detached Structures Influence Coverage

Detached structures (sheds, detached garages, fences, gazebos) are automatically covered under Coverage B, usually at 10% of your dwelling limit. A home with $300,000 dwelling coverage receives $30,000 for other structures by default. If you have a large workshop, barn, or a finished guest house, that 10% may not be enough, and you should increase the limit or purchase a separate structure endorsement to match the actual rebuild cost.

Every time you finish a renovation (adding a bedroom, remodeling a kitchen, installing a new roof) you increase the cost to rebuild your home, so you must update your Coverage A dwelling limit to reflect the new value. Failing to increase coverage after a $50,000 kitchen remodel can leave you underinsured by exactly that amount if a fire destroys the house. Call your insurer immediately after completing any major project, provide receipts and contractor invoices, and request a coverage adjustment. Roof age and material also affect premiums. Upgrading from asphalt shingles to metal or tile often qualifies for a discount because these materials resist wind and fire better, but the insurer needs to know about the change to apply the credit.

Checklist for New Homeowners to Determine Ideal Coverage Levels

Setting your initial homeowners insurance limits requires gathering information about your home, your belongings, and your financial situation, then translating those details into policy limits and endorsements.

Follow these steps before you buy your first policy:

-

Calculate replacement cost for your dwelling. Multiply square footage by local rebuild cost per sq ft, then add 10–25% for permits, code upgrades, and debris removal.

-

Inventory your personal property. Photograph every room, list high value items with receipts, and estimate total replacement cost to confirm the default 50–70% coverage is adequate.

-

Verify lender insurance requirements. Confirm minimum dwelling coverage (often 100% of replacement cost or loan balance), flood zone status, and any required endorsements.

-

Compare quotes on coverage types, not just price. Check whether policies offer replacement cost or ACV for contents and roof, confirm deductible types (flat or percentage), and verify included endorsements.

-

Evaluate liability and umbrella needs. Set liability at $300,000–$500,000 minimum, and add a $1,000,000 umbrella if your net worth or future earnings justify it.

-

Add essential endorsements. Purchase flood or earthquake coverage if your location requires it, add sewer backup and scheduled item endorsements, and confirm ordinance and law coverage for code upgrade costs.

-

Choose an appropriate deductible. Balance premium savings against your emergency fund. Select $1,000–$2,500 if you can cover that amount comfortably, and confirm any separate percentage deductibles for wind or earthquake.

Final Words

in the action: we walked through measuring rebuild cost, setting dwelling limits, estimating personal property, choosing liability and umbrella amounts, planning additional living expenses, picking deductibles, and checking endorsements.

Use square footage × local rebuild cost, add 10–25% for code and debris. Personal property is usually 50–70% of dwelling; consider $300k–$500k liability and ALE that matches local living costs.

If you still ask how much coverage do I need as a new homeowner, follow these rules of thumb and review annually — you’ll be in good shape.

FAQ

Q: How much homeowners coverage should you have?

A: The amount of homeowners coverage you should have equals your home’s rebuild cost (sq ft × local rebuild cost), plus 10–25% for code upgrades. Aim personal property 50–70% of dwelling; liability $300k–$500k recommended.

Q: Is osteoporosis covered by insurance?

A: Osteoporosis is covered by health insurance, not homeowners policies. Medical tests, prescriptions, and treatments are handled by health plans or Medicare; disability or long-term-care policies may help with related daily-care costs.

Q: What is the 80% rule for homeowners insurance?

A: The 80% rule means you must insure at least 80% of your home’s replacement cost to avoid coinsurance penalties. For a $400,000 rebuild estimate, carry at least $320,000 in dwelling coverage.

Q: Does homeowners insurance cover termites?

A: Homeowners insurance typically does not cover termite damage because it’s treated as preventable maintenance. Pest-control warranties, home warranties, or specific endorsements may cover termites; check your policy and schedule regular inspections.