{kind=link}

Think disability insurance is only for older people? Think again.

A 25-year-old worker faces about a one-in-four chance of a disability before retirement, and without coverage a few months away from work can wipe out your savings.

This post breaks down what entry-level disability insurance actually pays, the difference between short- and long-term plans, employer group versus individual options, and the key terms to watch so you can pick sensible, affordable protection early.

Clear Breakdown of What Entry-Level Disability Insurance Covers

Disability insurance replaces part of your income when illness or injury stops you from working. For people just starting their careers, this keeps the bills paid when the paycheck disappears. Most policies replace around 50% to 60% of what you earned before getting sick or hurt. Insurers won’t cover 100%. That percentage might feel low, but it’s usually enough to handle rent, groceries, car payments, and student loans when your income suddenly cuts off.

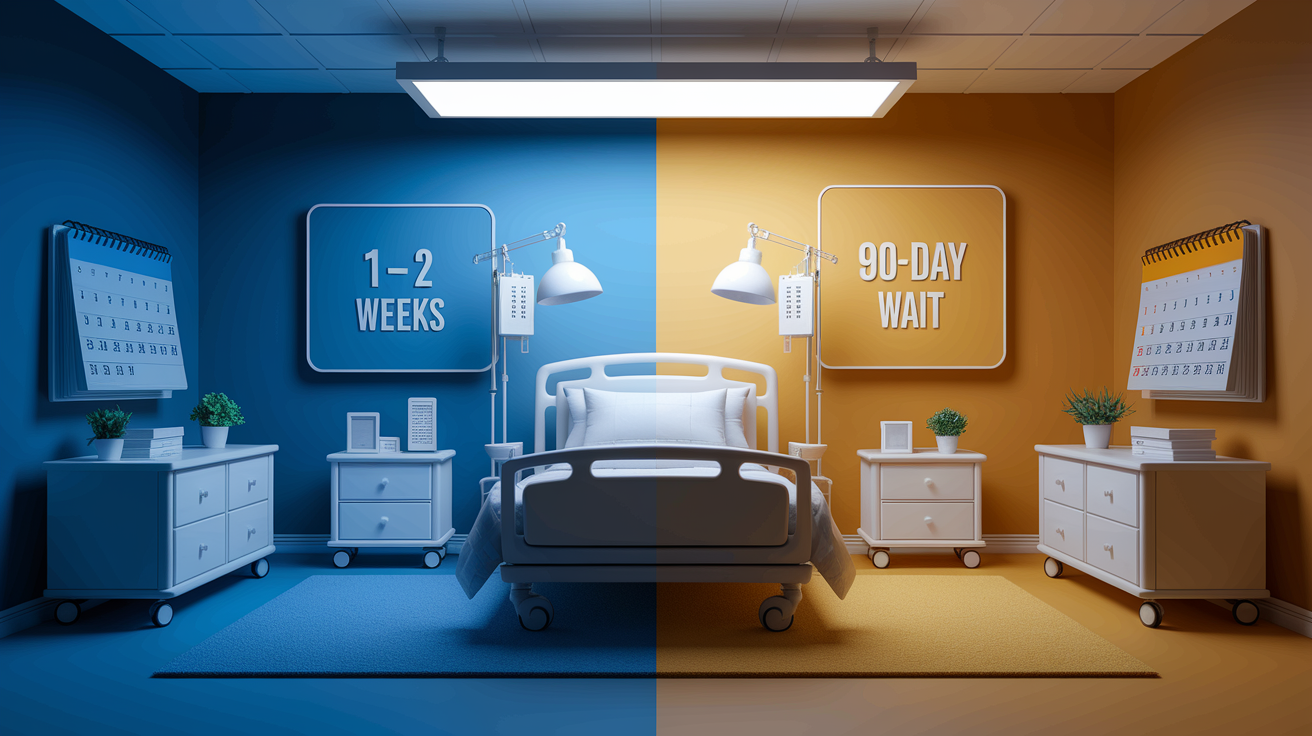

The two main types run on different timelines. Short-term disability insurance usually starts paying within one to two weeks after you can’t work anymore and keeps going for three to six months. Long-term disability insurance typically makes you wait 90 days before benefits kick in, then can last for several years or until you hit retirement age, like 65. Think of the waiting period like a deductible. You’ve got to be disabled that long before the insurer starts sending checks.

Early in your career, protecting your income matters way more than most people think. A 25-year-old worker has about a one in four chance of getting disabled before age 67. That’s eight times more likely than dying during those same years. Locking in coverage early means lower premiums and protection during the decades when you’re building savings, paying off debt, and funding retirement accounts.

Here’s what disability insurance actually does:

- Replaces lost income when you can’t earn your regular paycheck

- Covers essential bills like housing, utilities, and loan payments

- Protects long-term earning potential by preventing gaps that mess up retirement savings

- Bridges waiting periods for other programs like Social Security Disability

- Prevents financial instability that forces you to drain emergency funds or rack up debt

Short-Term vs Long-Term Entry-Level Disability Insurance Basics

Short-term disability insurance handles temporary problems. Surgery recovery, childbirth, a broken bone that needs a few months to heal. STDI sends you weekly or biweekly payments while you’re out of work. Benefits usually start within one to two weeks of your last workday and keep going for several weeks up to six months. The short benefit window keeps premiums lower per dollar of coverage, but claims happen often. Minor injuries and planned medical events trigger STDI all the time.

Long-term disability insurance protects against events that keep you out of work for months or years. Cancer treatment, severe injuries, major mental health conditions, degenerative diseases. These often need lengthy recovery or result in permanent impairment. LTDI policies usually make you wait 90 days before benefits start. Once they’re active, payments can last for a set number of years (two, five, or ten are common) or continue until you reach a certain retirement age, like 65 or 67. The longer the potential benefit period, the higher the premium.

| Type | Start Time | Typical Duration | Common Uses |

|---|---|---|---|

| Short-Term (STDI) | 1–2 weeks after disability begins | 3–6 months | Surgery recovery, childbirth, short-term injuries, minor illnesses |

| Long-Term (LTDI) | After 90-day elimination period (can vary) | Several years to age 65/67 | Cancer, severe injuries, heart attack recovery, mental health conditions, chronic diseases |

Entry-Level Worker Coverage Essentials and Why Early Protection Matters

Most disability policies replace 50% to 60% of your pre-disability income. Insurers cap the replacement ratio so people don’t earn more while disabled than they did working. For entry-level salaries, that percentage usually translates to enough for rent, food, and loan payments. Not discretionary spending. If you earned $40,000 a year before disability, expect a benefit of roughly $20,000 to $24,000 per year. Some employer group plans impose even stricter caps, limiting total monthly benefits no matter what your salary was.

Premiums are lower when you’re younger and healthier. A 25-year-old in good health pays way less than a 45-year-old with the same coverage amount and occupation. Buying early also locks in your insurability. If you develop a chronic condition or have a serious medical event later, individual policies might become unaffordable or completely unavailable. Emergency funds can substitute for short-term disability sometimes, but almost no early-career workers have the savings to replace months or years of lost income if a long-term disability hits.

Here’s why getting disability insurance early makes sense:

- Lower cost: Premiums go up with age and health changes.

- Stronger insurability: Locking in coverage before medical issues show up keeps the option open.

- Income protection during critical years: Your 20s and 30s are when you build the foundation for long-term financial stability.

- Portability: Individual policies stay with you no matter where you work, protecting you through job changes.

Group vs Individual Entry-Level Disability Insurance Options

Employer-sponsored group disability insurance is the easiest starting point. Lots of companies offer short-term and long-term disability as part of their benefits package, often with no medical exam if you enroll as a new hire. Premiums usually come out of your paycheck, and the employer might cover part or all of the cost. The catch: group policies often end when you leave the company, benefits might be capped at a flat dollar amount or percentage well below your full salary, and the definition of disability can get more restrictive over time (shifting from “own occupation” early in the claim to “any occupation” after a set period, like two years).

Individual disability insurance policies require medical underwriting. Application, health questionnaire, sometimes a physical exam or medical records review. The insurer checks your occupation, income, and health history before issuing coverage. Individual policies cost more than group plans but offer stronger protection. The contract is portable (it stays with you if you change jobs), disability definitions tend to be more favorable (especially “own occupation” language), and you can add riders like cost-of-living adjustments (COLA) or guaranteed insurability options that let you increase coverage later without a new exam.

Early-career workers often do best by combining both types. Enroll in your employer’s group plan to get immediate, low-cost baseline coverage, then add an individual policy that gives you portability, higher benefit limits, and stronger contract language. As your income grows, the individual policy can be increased (if you included a guaranteed insurability rider) without requiring proof of good health. That layered approach balances affordability, immediate protection, and long-term flexibility.

Key Disability Insurance Terms Explained Simply for Beginners

Own vs Any Occupation Definitions

“Own occupation” means the insurer pays benefits if you can’t perform the main duties of your specific job, even if you could work in a different role. A surgeon who injures both hands and can’t operate anymore might still collect full benefits under a true own-occupation policy, even if that surgeon earns income teaching or consulting. “Any occupation” requires that you be unable to perform any job you’re reasonably qualified for by education, training, or experience. Much harder standard to meet. Policies sold as “own occupation” often include fine print that shifts to “any occupation” after a set period, usually two years.

Elimination vs Waiting Periods

The elimination period is the number of days you’ve got to be disabled before benefits begin. It works like a deductible measured in time instead of dollars. The most common elimination period for individual long-term disability policies is 90 days. Shorter elimination periods (30 or 60 days) cost a lot more. Longer periods (180 days or one year) offer only modest premium savings. The waiting period is sometimes used interchangeably with elimination period, but in practice both terms mean the same thing: the gap between when you become disabled and when the insurer starts paying.

Benefit Period Basics

The benefit period defines how long the insurer will pay monthly benefits once they start. Common benefit periods include two years, five years, ten years, to age 65, or to age 67. The average disability claim lasts about five years, which means a two-year benefit period covers many claims but leaves you exposed if the disability continues. “To age 65” or “to age 67” gives you the strongest protection for severe, long-lasting conditions. If cost is a problem, a five-year benefit period provides real protection for most claims and costs way less than lifetime coverage.

Residual and Partial Disability

Residual disability coverage pays a proportional benefit if you return to work but earn less than you did before the disability. If your income drops by 40% because you can only work part-time or in a lower-paying role, the policy pays 40% of your full benefit. Most policies require at least a 20% loss of income to trigger residual benefits. Total disability is often defined as a 75% to 80% loss of income, depending on the carrier. Residual riders are really valuable because many claims go from total to partial disability over time. Recovery is often gradual, and this rider supports you during that transition.

Popular Riders (COLA, GI, Catastrophic)

A cost-of-living adjustment (COLA) rider increases your benefit amount while you’re on claim, usually starting at the end of the first year and annually after that. The increase is typically tied to the Consumer Price Index (CPI) with a cap, like 3% or 6% per year, and can be simple or compound. Guaranteed insurability (GI) riders let you buy more coverage on certain anniversaries without a medical exam, requiring only proof of higher income. Catastrophic illness riders pay an extra monthly benefit if you suffer a severe impairment, like needing help with two of six activities of daily living or significant cognitive decline. Stacking a catastrophic rider with your base benefit can bring total replacement closer to 100% of your pre-disability income.

Cost Drivers and Sample Pricing Insights for Entry-Level Disability Insurance

Premiums vary a lot based on age, health, occupation, and the strength of the policy contract. Younger applicants in low-risk occupations (office work, technology, finance) pay the least. Adding features like own-occupation definitions, non-cancellable rate guarantees, COLA riders, and guaranteed insurability options bumps up the monthly cost. Occupation class is one of the biggest premium drivers. Manual laborers and people in high-risk jobs pay way more than desk workers, and some jobs (offshore drilling was one example) might be uninsurable under standard policies.

Short-term disability insurance tends to cost more per dollar of benefit because short-term claims are common. Long-term disability premiums are higher in absolute terms but spread that cost over the potential for years of benefits. Non-cancellable policies, where the insurer can’t raise your rates, cost more upfront but give you rate stability for decades. Guaranteed renewable policies let the insurer increase premiums for entire classes of policyholders, which can lead to surprise rate hikes later in life.

Here are five practical ways to cut costs for entry-level workers:

- Choose a longer elimination period (90 or 180 days instead of 30) to reduce premiums, then rely on an emergency fund or employer short-term disability to cover the gap.

- Select a shorter benefit period (five years instead of to age 65) if premium affordability is critical. Coverage for the average claim length is better than no coverage at all.

- Drop or defer riders like COLA or catastrophic illness until income increases, then add them later if the policy includes guaranteed insurability.

- Avoid graded premium policies that start cheap but increase annually. They often cost more over the life of the contract and increase the risk you’ll drop coverage when rates climb.

- Combine employer group coverage with a small individual policy to balance immediate affordability and long-term portability.

How Entry-Level Workers Obtain Disability Insurance

Start by checking what your employer offers. Lots of companies provide group short-term and long-term disability insurance with guaranteed-issue enrollment during your first 30 days of employment. Guaranteed-issue means no medical exam or health questionnaire. Everyone who enrolls during the window gets approved. If your employer pays the premium and doesn’t include it as taxable income on your W-2, any benefits you receive will be taxable. If you pay the premium yourself or the employer includes the premium as imputed income, benefits are generally tax-free.

If employer coverage is limited or doesn’t exist, individual policies fill the gap. These require underwriting. Expect to complete a detailed application covering your occupation, income, health history, hobbies, and sometimes family medical history. Depending on the benefit amount and your health profile, the insurer might request medical records, order a phone interview with a nurse, or require a physical exam (blood work, urine sample, height/weight check). Guaranteed insurability riders are especially valuable for early-career workers. They lock in the ability to increase coverage at future anniversaries without repeating the underwriting process, even if your health gets worse.

Follow these four steps to get covered:

- Review your employer’s plan during open enrollment or within 30 days of hire to capture any guaranteed-issue windows.

- Compare supplemental options from individual carriers, focusing on own-occupation definitions, benefit periods, and riders that fit your budget.

- Apply for individual coverage while you’re healthy. Medical underwriting is easier and premiums are lower when you have no pre-existing conditions.

- Use online calculators to figure out how much monthly benefit you need based on fixed expenses (rent, loans, utilities) and the length of time your emergency fund could cover a gap.

Real Entry-Level Disability Scenarios and How Claims Work

Filing a claim starts with notifying your insurer as soon as you believe you meet the policy’s definition of disability. You’ll complete claim forms and provide medical documentation from your treating physician that describes your diagnosis, treatment plan, functional limitations, and expected recovery timeline. The insurer compares that documentation to the disability definition in your policy. If the claim gets approved, benefits usually start after you satisfy the elimination period. Commonly 90 days for long-term policies, shorter for short-term coverage.

Certain conditions qualify as presumptive disabilities and trigger automatic payouts without waiting periods or strict proof of inability to work. Common examples include loss of sight in both eyes, loss of hearing in both ears, loss of speech, loss of both hands or both feet, or loss of one hand and one foot. Some policies also include specific cancers or total paralysis in their presumptive disability language. These provisions recognize that certain injuries or illnesses are just inherently disabling and get rid of the burden of proving you can’t perform job duties.

Here are three real examples of how claims play out:

-

Short-term recovery from surgery: A 27-year-old administrative assistant undergoes knee surgery and can’t return to work for six weeks. Her employer’s short-term disability policy has a one-week waiting period, then pays 60% of her salary for up to 12 weeks. She receives benefits for five weeks (six weeks minus the one-week wait), covering most of her mortgage and utilities while she recovers at home.

-

Childbirth complication: A 29-year-old accountant experiences complications during childbirth and can’t work for three months. Her individual short-term disability policy has a two-week elimination period and pays benefits for up to six months. She receives roughly 10 weeks of benefits (12 weeks total disability minus the two-week wait), replacing about 50% of her income during that period.

-

Long-term cancer treatment: A 32-year-old software engineer gets diagnosed with cancer and undergoes surgery, chemotherapy, and radiation over 18 months. His employer’s long-term disability plan has a 90-day elimination period and pays 60% of his salary to age 65 as long as he remains unable to perform his job duties. After satisfying the 90-day wait, he receives monthly benefits for the rest of his treatment and recovery. More than a year in total. This lets him focus on his health without losing his home or defaulting on student loans.

Choosing the Right Entry-Level Disability Insurance Policy: Checklist

Not all disability policies are built the same. Definitions, exclusions, renewability guarantees, and rider options vary a lot among carriers and even among different products from the same insurer. Reading the policy contract before you buy, or at minimum asking pointed questions, prevents surprises when you need to file a claim. Policies marketed as comprehensive sometimes include restrictive language buried in the fine print, like mental health limitations (benefits capped at 24 months), substance abuse exclusions, or gradual shifts from own-occupation to any-occupation definitions.

Use this checklist when comparing policies or talking with an agent:

- What is the exact definition of disability? Confirm whether the policy uses own-occupation, any-occupation, or a hybrid that changes over time.

- How long is the elimination period? Know how many days you’ve got to be disabled before benefits start.

- What is the benefit period? Verify how long benefits continue. Two years, five years, to age 65, or longer.

- Is the policy non-cancellable or guaranteed renewable? Non-cancellable locks your rate. Guaranteed renewable allows rate increases.

- What riders are included or available? Look for COLA, residual disability, guaranteed insurability, and catastrophic illness options.

- Are there exclusions or limitations? Ask specifically about mental health caps, pre-existing condition clauses, and high-risk activity exclusions.

- How is “income” defined for benefit calculation? Some policies exclude bonuses, commissions, or irregular income when calculating your benefit amount.

- Can I increase coverage later without a medical exam? Confirm whether guaranteed insurability or automatic increase riders are available and how they work.

Final Words

You now know the basics: what entry-level disability insurance covers, the short-term vs long-term rules, and why early-career protection matters.

We also covered group versus individual options, key terms to watch, cost drivers, how to buy, and real claim examples. Use the checklist to compare offers and spot common gaps.

If you want a next step, compare your employer plan to an individual quote. This is entry level disability insurance explained in plain steps. You’re in a strong position to protect your income.

FAQ

Q: How much SSDI will I get if I make $60,000 a year?

A: The SSDI you’ll get if you make $60,000 a year depends on your average indexed monthly earnings, work history, and bend points—typical benefits range about $1,200–$2,500 monthly; use the SSA calculator for an exact estimate.

Q: Does osteoporosis qualify for disability? Does Parkinson’s qualify for long-term disability? Does ALS qualify for social security disability?

A: Osteoporosis qualifies only if fractures or severe limits prevent you from working; Parkinson’s can qualify when symptoms stop you from doing your job; ALS typically meets Social Security listings and often gets faster approval with strong medical records.