{kind=link}

Think a bad accident can’t wipe out your savings?

Many people assume their car or home insurance will cover everything.

Umbrella insurance is extra liability protection that kicks in when those policies hit their limits, often starting at $1,000,000 for as little as $150 to $300 a year.

This post explains what umbrella policies cover, common exclusions, how they work with your auto and home insurance, and what to buy based on your risk.

Core Explanation of Umbrella Insurance Fundamentals

Here’s umbrella insurance in one sentence: it’s extra liability coverage that kicks in when a claim blows past your home, auto, or renters policy limits. Picture this. Your auto insurance covers up to $300,000 for injuries you cause in a crash. A serious wreck leads to $1,200,000 in medical bills and legal costs. Your auto policy pays its $300,000 cap, then your umbrella steps in and covers the remaining $900,000, assuming your umbrella limit is high enough. This layer sits “above” what you already have, catching expenses that would otherwise wipe out your savings, retirement accounts, or future paychecks.

How it actually works: umbrella insurance waits on the sidelines until your base liability policy maxes out, then it covers the next chunk. Let’s say you’ve got $300,000 of homeowners liability and a guest gets badly hurt on your property, leading to an $800,000 settlement. Your homeowners policy handles the first $300,000. Your umbrella takes care of the remaining $500,000 if you’ve bought enough coverage. Without that umbrella, you’re personally on the hook for $500,000. That could mean losing home equity, draining college funds, or dealing with garnished wages.

Excess liability just means coverage that goes beyond your base policy caps. Your home and auto policies already include liability protection, but those limits usually stop somewhere between $100,000 and $500,000 depending on what you purchased. Umbrella insurance adds another million or more on top, so your total protection can reach several million if something catastrophic happens.

- Pushes total liability limits way beyond standard home and auto policy caps.

- Handles certain personal liability claims (think defamation or privacy invasion) that your base policies might exclude or barely touch.

- Shields personal assets and future earnings from getting seized to pay a judgment.

- Covers legal defense costs for covered claims, which can pile up fast even before trial.

Key Coverage Basics of Umbrella Insurance

Umbrella insurance typically covers bodily injury to others, property damage to others, and personal liability situations that exceed your underlying limits. It also picks up legal fees and court costs, which can easily hit tens of thousands even if you win. Say you accidentally injure a pedestrian while driving and medical bills, lost wages, and pain and suffering push the claim past your auto liability cap. The umbrella covers the excess. Same story if a guest slips on your icy driveway, suffers a brain injury, and sues you for $2,000,000.

Real situations where this matters: landlord liability if you rent out a place and a tenant gets hurt due to negligence, personal injury claims like libel or slander (for instance, if you’re sued for defamatory comments made online or at a community meeting), and incidents involving boats, RVs, or vacation properties. The policy generally covers legal defense from the moment a covered lawsuit gets filed, so you won’t be paying an attorney out of pocket while fighting the case.

- Bodily injury to others: medical expenses, lost income, pain and suffering, rehab costs.

- Property damage to others: repairs or replacement of vehicles, buildings, fences, belongings you accidentally damage.

- Personal and advertising injury: libel, slander, wrongful eviction, invasion of privacy, similar personal liability claims.

- Landlord liability: injuries or damages at rental properties you own, depending on policy terms.

- Legal defense costs: attorney fees, court costs, expert witnesses, settlement negotiations for covered claims.

- Worldwide coverage: many policies extend liability protection to incidents outside the U.S., with some limitations.

Common Limitations of Basic Umbrella Insurance

Umbrella policies protect you from lawsuits brought by other people, so they generally don’t cover your own injuries, your own property damage, or liabilities from running a business. Exclusions exist because insurers want to separate personal liability from commercial risk and intentional harm from accidents. The specific exclusion list varies by carrier and policy, so read the declarations page and policy language before buying.

Most policies exclude certain high risk or specialized exposures that need separate coverage. If you run a business, provide professional services, or engage in high risk hobbies like flying planes, those activities typically fall outside a personal umbrella and require their own liability policies.

- Your own injuries or property damage: umbrella insurance pays claims brought against you, not your own medical bills or car repairs.

- Business and professional activities: if you run a company, practice medicine or law, or provide consulting, you need commercial general liability or professional liability coverage instead.

- Intentional or criminal acts: lawsuits from assault, fraud, or other deliberate harmful conduct are excluded.

- Contractual liability: obligations you take on by signing a contract (like agreeing to indemnify a venue where you’re hosting an event) may not be covered unless the policy includes specific language.

- Self insured retention on drop down claims: if the umbrella covers a claim type not covered by your underlying policy (certain defamation claims, for example), you might owe a small deductible, often $250 to $500, before the umbrella pays.

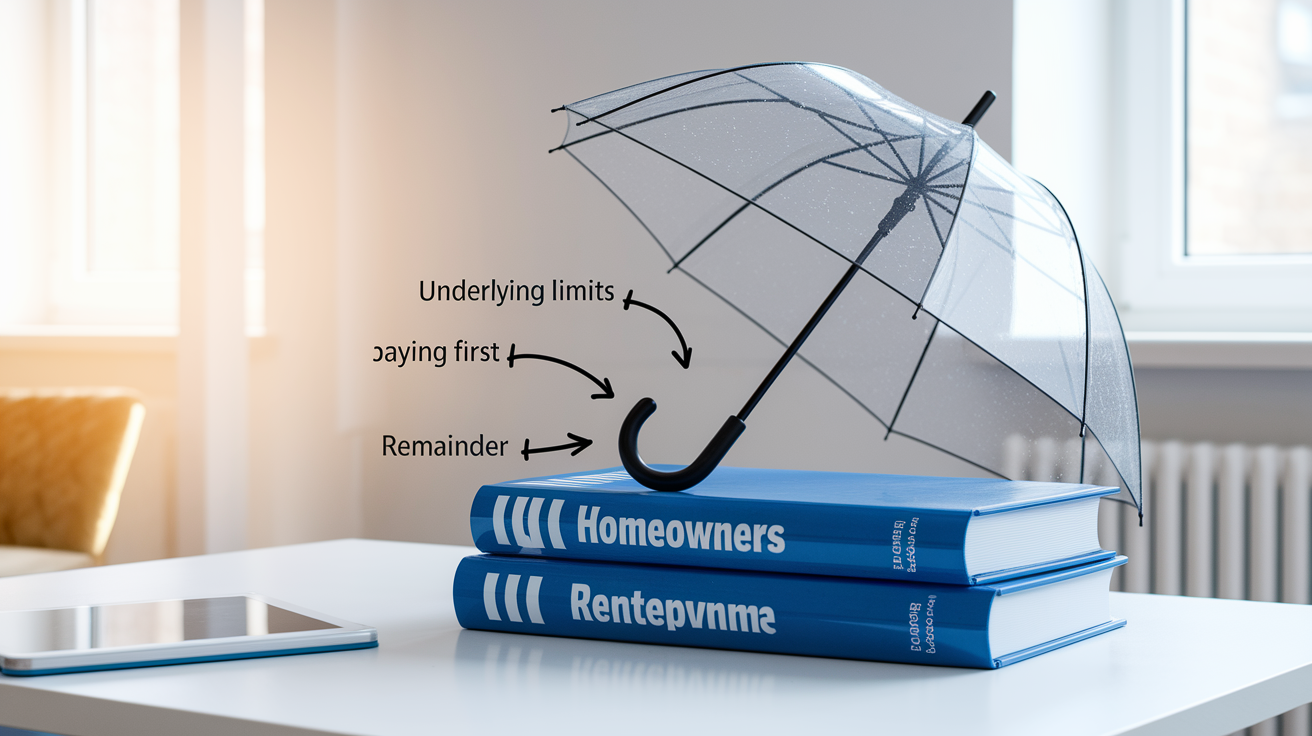

How Umbrella Insurance Works With Auto and Home Policies

Umbrella insurance doesn’t replace your existing auto, homeowners, or renters insurance. It requires you to keep minimum liability limits on those base policies before the umbrella activates. For instance, an insurer might require at least $250,000 per person and $500,000 per accident in auto bodily injury liability, plus at least $300,000 in homeowners liability, before they’ll sell you a $1,000,000 umbrella. These underlying limits ensure your primary policies handle smaller claims, so the umbrella only responds to the most serious stuff.

When a covered claim happens, the underlying policy pays first up to its full limit. Once that’s exhausted, the umbrella kicks in up to the umbrella limit you bought. If a claim falls in a coverage gap (your base policy excludes it but your umbrella covers it), some umbrella policies will “drop down” and pay directly after you satisfy a small self insured retention. This feature isn’t universal, so confirm with your agent whether your policy includes drop down coverage for personal injury claims like defamation.

If you own multiple vehicles, multiple properties, or rent out a home, your insurer may require higher underlying limits or endorsements on your base policies. Say you own a rental property. The insurer may ask you to add a landlord liability endorsement to your homeowners policy and bump that policy’s liability limit to $500,000 before issuing the umbrella. These requirements protect both you and the insurance company by making sure serious exposures are backed by adequate primary coverage.

| Primary Policy Type | Typical Required Limit | How Umbrella Applies |

|---|---|---|

| Auto Insurance | $250,000 per person / $500,000 per accident (or $300,000+ combined single limit) | Auto policy pays up to its limit; umbrella pays the remainder of the claim. |

| Homeowners Insurance | $300,000 to $500,000 liability coverage | Homeowners policy pays first; umbrella covers excess liability and some additional personal injury claims. |

| Renters Insurance | $100,000 to $300,000 liability coverage | Renters policy pays its limit; umbrella picks up the remaining covered liability, if applicable. |

Coverage Amounts and Typical Policy Limits

Many personal umbrella policies start at $1,000,000, which is often the minimum insurers will sell. That first million typically runs between $150 and $300 per year for a household with average risk factors, making it one of the most affordable ways to add serious liability protection. If you own significant assets, have multiple drivers in your household, or face higher liability exposures, consider $2,000,000 or more.

Higher limits come in increments, and each additional million usually costs less than the first. Jumping from $1,000,000 to $2,000,000 might add only $50 to $100 per year. Reaching $5,000,000 could cost $300 to $500 annually depending on your risk profile. Some carriers offer policies up to $10,000,000 for individuals with very high net worth, complex asset structures, or elevated public exposure.

- $1,000,000 (1 million): Most common starting point, suitable for homeowners and families with moderate assets and standard liability risks.

- $2,000,000 (2 million): Common choice for households with significant home equity, retirement savings, or one or more teenage drivers.

- $5,000,000 (5 million): Often selected by higher net worth individuals, landlords with multiple properties, or people in public facing roles.

- $10,000,000 (10 million): Available through select carriers for ultra high net worth households or those with complex liability exposures; may require underwriting review.

Real World Scenarios Where Umbrella Insurance Helps

Umbrella insurance becomes valuable when standard policy limits can’t cover the full cost of a serious accident or lawsuit. These situations aren’t rare edge cases. They happen every day across the country, and the financial fallout can be brutal without adequate coverage. A severe car accident with multiple injured passengers, a dog bite that requires reconstructive surgery, or a guest who suffers a life changing injury at your home can all lead to claims in the hundreds of thousands or millions.

Legal defense alone can cost $50,000 to $150,000 or more, even if you ultimately win or settle early. Umbrella insurance pays those defense costs in addition to any settlement or judgment, which means your policy limit stays mostly intact to cover the actual damages. This dual benefit (defense costs plus liability coverage) makes umbrella insurance especially powerful in high stakes lawsuits.

Another area where umbrella coverage proves useful is defamation or personal injury claims. If you’re accused of libel, slander, wrongful eviction, or invasion of privacy, your homeowners or renters policy may provide little or no coverage, but your umbrella often will. In those cases, the umbrella may drop down and cover the claim after you pay a small self insured retention, protecting you from paying tens of thousands in legal fees and potential damages out of your own savings.

| Scenario | Typical Liability Risk | Umbrella Benefit |

|---|---|---|

| Severe At Fault Auto Accident | Medical bills, lost wages, pain and suffering for multiple injured parties can exceed $500,000. | Covers the amount above your auto liability limit, protecting your savings and home equity. |

| Dog Bite Lawsuit | Reconstructive surgery, therapy, and legal costs can reach $100,000 to $300,000 or more. | Picks up costs beyond your homeowners liability limit; may also cover defense fees. |

| Guest Injury at Your Home | Pool accidents, trampoline injuries, or slip and fall incidents can result in six figure claims. | Extends coverage after homeowners policy limit is exhausted, including legal defense. |

| Defamation or Slander Claim | Libel lawsuits, online defamation, or wrongful eviction claims can involve substantial legal fees. | May drop down to cover the claim if your base policy excludes it, after a small retention. |

| Rental Property Liability | Tenant injuries due to negligence (faulty stairs, broken railings) can lead to large settlements. | Provides additional liability protection for landlords, subject to policy terms and underlying coverage requirements. |

Who Benefits Most From an Umbrella Policy

Homeowners with significant equity, families with teenage drivers, and landlords who rent out residential property are among the groups who get the most value from umbrella insurance. If a lawsuit judgment exceeds your primary insurance limits, creditors can go after your bank accounts, investment portfolios, and even future earnings through wage garnishment. Umbrella coverage shields those assets by providing an extra layer that kicks in when your base policies max out.

People who own pools, trampolines, boats, or dogs also face higher liability exposure. A single incident (a child drowning in an unsecured pool or a dog biting a neighbor) can result in a multi million dollar lawsuit. Even if you take every reasonable precaution, accidents happen. Juries often award large sums to injured parties. Umbrella insurance ensures you’re not personally on the hook for those awards.

- Homeowners with substantial home equity or savings: If your net worth exceeds $100,000, a lawsuit could threaten your financial security.

- Parents of teenage drivers: Teen drivers have higher accident rates. At fault crashes involving young drivers can result in catastrophic injuries and outsized verdicts.

- Landlords and owners of rental properties: Tenant injuries, wrongful eviction claims, and property related accidents increase liability risk.

- Owners of recreational vehicles, boats, or ATVs: These activities carry additional accident risk that may exceed standard auto or homeowners liability limits.

- Individuals with high future earning potential: Even if your current assets are modest, a judgment can attach to your future income for years.

- Public facing professionals or volunteers: If you serve on a nonprofit board, coach youth sports, or hold a visible community role, you may face personal liability or defamation claims.

Cost Basics and Affordability of Umbrella Insurance

A $1,000,000 personal umbrella policy typically costs between $150 and $300 per year for a household with average risk factors. That makes it one of the most affordable ways to add substantial liability protection. Each additional million dollars of coverage usually costs $50 to $150 more per year, so a $2,000,000 policy might run $200 to $400 annually. A $5,000,000 policy could cost $400 to $600 depending on your insurer and risk profile. These are rough estimates. Actual premiums vary by state, carrier, and individual underwriting factors.

Several factors influence your umbrella insurance premium. Insurers look at the number of vehicles you own, the number of licensed drivers in your household, your driving record, any prior liability claims, the number of properties you own, and whether you have high risk features like a pool, trampoline, or certain dog breeds. Your location matters too. States with higher jury verdicts and more litigious legal climates tend to have higher umbrella premiums. If you’ve had at fault accidents, speeding tickets, or liability claims in the past three to five years, expect to pay more.

- Number of vehicles and drivers: More cars and more drivers mean higher accident exposure, which raises the premium.

- Driving record and claims history: At fault accidents, DUIs, or recent liability claims can increase your cost or make coverage harder to obtain.

- Property exposures: Owning rental properties, having a swimming pool, trampoline, or certain dog breeds all increase risk and premium.

- Geographic location: States with higher litigation rates, larger jury awards, or more severe weather risks may see higher umbrella insurance costs.

Choosing the Right Umbrella Insurance Limit

Choosing the right umbrella limit starts with adding up your current assets and estimating your future earning potential. Include your home equity, retirement accounts, savings, investment accounts, and college funds. Then think about how many years of income you could lose if a judgment allowed creditors to garnish your wages. Say you’ve got $500,000 in net assets and expect to earn another $1,000,000 over the next decade. You’re looking at $1,500,000 of potential exposure that a serious lawsuit could reach.

Next, evaluate your personal liability exposures. Do you have teenage drivers? Own rental properties, a pool, a boat, or a trampoline? Frequently host gatherings at your home? Have a dog, especially a breed that insurers consider higher risk? Each of these bumps up the chance of a large liability claim. If you check multiple boxes, you may want to start with $2,000,000 or more in umbrella coverage rather than the minimum $1,000,000.

Finally, remember that umbrella insurance is relatively cheap for the protection it provides, so rounding up to the next coverage tier is often smart. If your asset analysis suggests you need $1,200,000 in coverage, buying a $2,000,000 policy for an extra $50 to $100 per year gives you a meaningful cushion. Review your coverage every few years or whenever your assets, income, or exposures change (after buying a home, having a child, acquiring rental property, or reaching a new career milestone).

- Tally your current assets and future earnings: Add home equity, savings, investments, and estimated lifetime income to understand your total exposure.

- Map your liability exposures: Count the number of drivers, vehicles, properties, pools, trampolines, boats, and other risk factors in your household.

- Start at $1,000,000 and scale up based on risk: If your assets and exposures are modest, $1,000,000 may be enough. If you have significant wealth or multiple high risk factors, consider $2,000,000 to $5,000,000 or more.

Final Words

You now know what an umbrella policy does: it sits on top of your home, auto, renters (or boat) liability and steps in when those limits run out. It boosts liability limits, helps cover legal fees, and can catch claims standard policies don’t cover.

We covered common exclusions, typical limits ($1M and up), real-life scenarios, who benefits, and how to choose a limit.

With basic umbrella insurance explained, you can see it’s an affordable, simple way to protect your assets. Worth checking at renewal or after any life change.

FAQ

Q: How much should a $1,000,000 umbrella policy cost?

A: A $1,000,000 umbrella policy typically costs about $150–$300 per year, depending on vehicles, drivers, properties, claims history, and location, so shop around for quotes.

Q: What is umbrella insurance for dummies?

A: Umbrella insurance, in simple terms, is extra liability coverage that kicks in after your auto or home limits are exhausted; it protects your savings and future earnings from large lawsuits.

Q: What are the downsides of umbrella insurance?

A: The downsides of umbrella insurance include exclusions, required higher underlying limits, and extra costs like a self-insured retention for certain claims. It also won’t cover intentional acts or most business liabilities.

Q: What does Dave Ramsey say about umbrella insurance?

A: Dave Ramsey says umbrella insurance is a smart, low-cost way to protect your assets and future earnings; he often recommends starting at $1 million if you have assets to protect.