{kind=link}

Think a budget planner is just a rigid list that kills spontaneity?

Actually, the right template or tool does the opposite: it shows where money arrives, where it leaks, and gives you small, practical levers to fix it.

This article walks you through simple budget planner components you can use right away—how to collect real numbers, turn yearly bills into monthly slices, and pick a method that fits your life.

You’ll see concrete examples, common traps, and templates (spreadsheets, printable, and apps) so you can stop guessing and start steering your money.

Core Components of an Effective Budget Planner and How to Use One Immediately

A budget planner organizes your income, expenses, and savings in one place so you can actually see where money shows up, where it disappears, and what’s left over. Could be a spreadsheet. Could be a printable PDF. Could be an online quiz that spits out a template. They all do the same thing: turn invisible money movement into something concrete you can work with.

The format matters less than what you put into it. Your planner is only useful if you feed it real numbers, so grab three months of bank statements, bills, utility invoices, and receipts before you start. Looking back through past transactions catches recurring subscriptions you forgot about, seasonal spikes, and one-off costs that memory alone won’t capture. Not sure about an amount? Overestimate. Better to budget cautiously than get blindsided mid-month.

Most planners break down into sections for income, fixed expenses, variable expenses, and savings or debt payments. Fixed costs stay the same each month: rent, insurance premiums, loan repayments, childcare contracts, gym memberships. Variable costs bounce around: electricity, water, groceries, fuel, shopping, dining out, travel, entertainment. Savings and debt categories show what you’re setting aside or paying down. By separating needs, wants, and obligations into different buckets, you can see whether you’re living within your means or quietly drifting into the red.

Here’s how to start using a budget planner right now:

-

Collect your statements. Download or print three months of bank transactions, credit card bills, utility invoices, and cash receipts.

-

List all income sources. Enter monthly take-home pay (after tax, National Insurance, student loan deductions), benefits, freelance income, rental income, anything regular hitting your account.

-

Categorize every expense. Assign each transaction to a category: housing, transport, food, insurance, subscriptions, entertainment, clothing, healthcare. Most planners include nearly 100 pre-built categories so you’re not lumping dissimilar costs together.

-

Assign monthly amounts. Enter fixed costs as they appear on bills. For variable costs, calculate the average across your three-month sample. For annual or irregular expenses (car insurance, holidays, Christmas), divide the yearly total by twelve to create a monthly equivalent.

-

Compare total expenses to total income. Subtract all outgoings from all income. Positive number means surplus. Negative means overspend.

-

Adjust allocations until the plan balances. If you’re overspending, identify categories to trim or switch. If you’ve got surplus, decide how much goes to savings, debt repayment, or future one-off costs.

A completed budget planner reveals spending leaks you never noticed. The £2.50 coffee habit costing over £600 a year. The unused subscriptions draining £15 monthly. The impulse online orders inflating your “miscellaneous” line. By showing the full picture in one view, the planner turns vague financial anxiety into a concrete list of priorities you can actually act on.

Advanced Budget Setup: Converting Irregular Costs, Auditing Spending Habits, and Setting Category Caps

Once you’ve built a basic budget, the next step is converting irregular and seasonal costs into predictable monthly entries so your planner reflects reality across the full year. One-offs don’t fit neatly into a “monthly” mindset. Holidays, Christmas gifts, car servicing, annual insurance renewals, back-to-school costs. They still drain your account when they land. The fix: estimate the annual total, divide by twelve, enter that amount as a monthly line item. £2,000 budgeted for car costs becomes £166.66 per month (most people round to £167 to keep the math clean). An £800 Christmas fund converts to £67 monthly. By spreading these costs month-by-month, your planner shows the true monthly commitment, not just the bills that happen to land this month.

An in-depth spending audit sharpens accuracy further. Pull twelve months of transaction history if you’ve got it, then look for seasonal patterns. Heating bills spike in winter, travel costs rise in summer, grocery spending jumps around holidays. Identify triggers that push you over budget: stress purchases, payday splurges, social pressure to match friends’ spending. Mark categories where you consistently underestimate, then raise those monthly caps to reflect habit rather than wishful thinking. The goal isn’t shame. It’s honesty. A budget pretending you spend £200 on groceries when you routinely spend £300 will fail every month, whereas a budget that accepts £300 and finds savings elsewhere can actually work.

Advanced budgeting elements that prevent ongoing overages:

- Category caps, maximum monthly spend per bucket, flagged when exceeded.

- Rolling categories, unspent grocery budget this month carries forward to next month.

- Seasonal adjustments, higher heating cap in winter, higher travel cap in summer.

- Monthly equivalents for annual costs, convert every yearly expense to its per-month share.

- Habit triggers, track what event or emotion precedes overspending in each category.

- Sub-categories, split broad buckets (e.g., “Food” into groceries, dining out, takeaways) to catch hidden leaks.

- Threshold alerts, notification when a category hits 75% of its cap mid-month.

- Reconciliation schedule, diary reminder to review actuals vs plan every month-end.

Realistic caps, informed by real transaction history, prevent the cycle where you set an aspirational budget, blow past it by day ten, then abandon the whole system in frustration. When caps reflect genuine spending patterns (not fantasy versions of yourself), you can make small, sustainable cuts rather than swinging between denial and despair. A budget that survives contact with your actual life is infinitely more valuable than a perfect spreadsheet you ignore after week one.

Budget Planner Methods: Zero-Based, 50/30/20, Envelope System, and Cash-Flow Tracking

Different budgeting methods suit different incomes, personalities, and financial goals. Many free budget planners are designed around a specific framework or let you choose one that fits.

Zero-Based Budgeting

Zero-based budgeting assigns every single pound of income a specific job before the month begins, so income minus all allocations equals zero. Every pound goes somewhere: rent, groceries, savings, debt repayment, entertainment, or a named sinking fund. The method forces intentional decision-making because there’s no “leftover” money sitting unassigned in your account. Works well for people who want maximum control, earn predictable income, and prefer active involvement in their finances. The downside is the administrative load. Every transaction needs a category, every category needs a limit. Miss a receipt or forget a subscription, and the whole plan wobbles.

50/30/20 Framework

The 50/30/20 rule splits after-tax income into three broad allocations: 50% for needs (housing, utilities, insurance, minimum debt payments, transport), 30% for wants (dining out, hobbies, subscriptions, holidays), and 20% for savings and extra debt repayment. Many free online budget planners automatically compare your entries to this breakdown and highlight where you’re over or under. The framework is forgiving and easy to explain, making it ideal for beginners or households that don’t want granular tracking. The trade-off is less precision. Lumping all “wants” together hides whether you overspend on clothes versus entertainment. For example, if you enter £1,200 monthly income, the 50/30/20 target is £600 needs, £360 wants, £240 savings. If your needs total £750, the planner flags the imbalance immediately.

Envelope System

The envelope system divides your budget into separate “envelopes” or pots, each holding money for a single category. Once an envelope is empty, spending in that category stops until next month. Physical envelopes use real cash. Digital versions use app-based “pots” offered by banks like Chase, Monzo, and Starling. You fund each pot via standing order on payday (£67 to the Christmas pot, £167 to the car pot, £300 to groceries) so your main account balance shows only genuinely available spending money. The method prevents accidental overspend because the structure is physical (or visually separated), not just a number in a spreadsheet you can ignore.

Cash-Flow Forecasting

Cash-flow forecasting projects income and expenses month-by-month across several months or a full year, showing when surpluses and shortfalls will occur. Especially useful for freelancers, seasonal workers, or anyone with irregular income. You enter expected income by month, then map fixed and variable costs to the same timeline. The forecast highlights months where income dips below expenses, giving you time to build a buffer or adjust spending before the gap hits. Unlike static monthly budgets, cash-flow planning treats your finances as a rolling film, not a single snapshot.

The best method depends on your income stability and control preference. Zero-based suits steady earners who want granular oversight. 50/30/20 suits beginners who need simplicity. Envelopes suit impulsive spenders who need physical boundaries. Cash-flow forecasting suits anyone facing income variability.

| Method | Best For | Key Advantage |

|---|---|---|

| Zero-Based | Steady income, high control preference | Every pound has a named purpose |

| 50/30/20 | Beginners, low administrative tolerance | Simple three-bucket framework |

| Envelope System | Impulsive spenders, tactile learners | Physical or visual spending limits |

| Cash-Flow Forecasting | Irregular income, seasonal work | Anticipates future shortfalls |

Using a Budget Planner to Build Short-Term and Mid-Term Savings Systems

A budget planner transforms vague savings intentions into funded, predictable systems by treating future expenses as current monthly obligations. Sinking funds are dedicated savings pots for known upcoming costs: Christmas gifts, summer holidays, car repairs, annual insurance premiums, back-to-school uniforms, wedding costs. Instead of scrambling when the bill arrives or reaching for a credit card, you’ve already set aside the money in small, manageable monthly chunks. The planner calculates the monthly amount by dividing the target total by the number of months until you need it, then you fund that category automatically each payday. If you need £800 for Christmas in twelve months, the planner shows £67 per month. If your car insurance renewal is £600 in six months, you allocate £100 monthly starting now.

An emergency fund sits alongside sinking funds but serves a different purpose: it covers true unpredictables like job loss, boiler breakdown, urgent medical costs, or sudden home repairs. Most guidance suggests three to six months of essential expenses as a target, though even £500 or £1,000 provides meaningful protection against small crises. The budget planner helps by showing your actual monthly needs total (rent, utilities, minimum food, transport, insurance), then multiplying that figure by three or six to set your emergency-fund goal. Once you know the target, you can assign a monthly contribution (£50, £100, £200) that appears as a line item in your budget just like any other expense.

Common sinking-fund categories that appear in well-structured budget planners:

- Christmas and holiday gift funds

- Annual or biannual insurance premiums (car, home, pet, life)

- Car maintenance, MOT, and repair reserves

- Holiday or travel savings

- Home maintenance and appliance replacement (boiler, fridge, washing machine)

Automation makes these systems sustainable. Many banking apps let you schedule standing orders that move money into labeled pots or separate savings accounts two days after payday, before you see the balance and mentally spend it. Round-up features (offered by apps like Chase, which rounds purchases to the nearest pound and saves the difference at rates like 5% AER on the rounded amount, or Monzo) automate micro-contributions without requiring active decisions. The more the system runs itself, the less willpower you need to maintain it.

Budget planners stabilize near-future financial needs by converting lumpy, irregular expenses into smooth monthly flows. Instead of January feeling catastrophic because Christmas, car insurance, and council tax all land at once, the planner spreads that pain across the year. Your main account balance becomes a truer picture of genuinely disposable income. Large purchases stop derailing your entire month because the money was already waiting in the right pot.

Debt-Repayment Planning Inside Your Budget Planner

A budget planner provides the structure debt repayment needs: a clear view of how much you owe, what you can afford to pay, and which debts to tackle first. Start by listing every non-mortgage debt (credit cards, personal loans, store cards, overdrafts, car finance, payday loans) along with the balance, interest rate, and minimum monthly payment. If your total non-mortgage debt exceeds 50% of your after-tax annual salary, you likely face a serious problem that needs immediate attention, not just incremental adjustments. For example, if you earn £24,000 after tax and owe £13,000 on credit cards and loans, the ratio signals a debt load that can spiral into missed payments, default charges, and long-term financial harm.

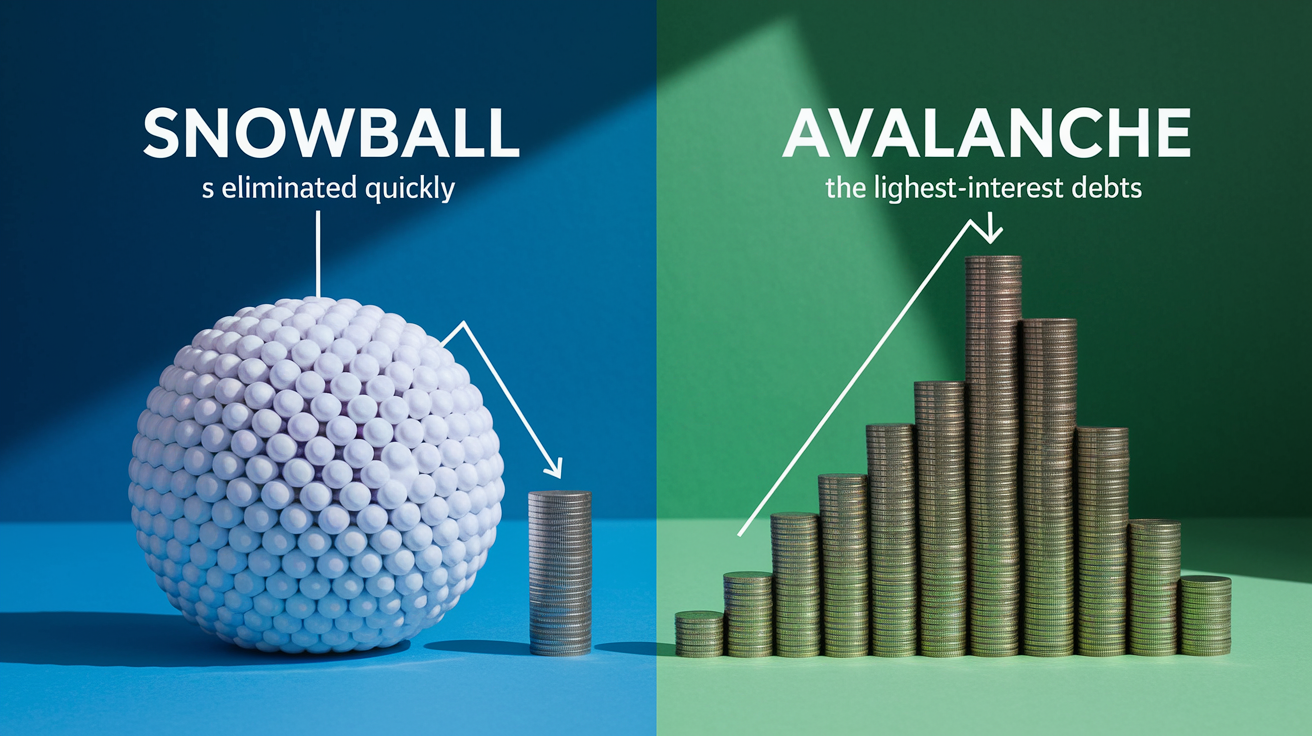

The planner shows where money is available for extra repayments by subtracting all essential expenses and minimum debt payments from income. Any surplus can be directed toward debt elimination using one of two priority frameworks. The snowball method targets the smallest balance first, regardless of interest rate, to generate quick wins and psychological momentum. You make minimum payments on all debts except the smallest, throw every spare pound at that one, then roll the freed-up payment into the next-smallest debt once the first is cleared. The avalanche method targets the highest interest rate first to minimize total interest paid over time. You make minimums on everything except the highest-rate debt, attack that aggressively, then move to the next-highest rate. Snowball prioritizes motivation and visible progress. Avalanche prioritizes mathematical efficiency and cost savings.

A small comparison of the two approaches:

- Speed to first payoff: Snowball wins, smallest balance clears fastest.

- Motivation and behavior change: Snowball wins, early wins build confidence.

- Total interest savings: Avalanche wins, high-rate debt costs the most.

- Required discipline: Avalanche demands more patience, snowball offers frequent reinforcement.

Before painful spending cuts, try “pain-free” savings. Switching credit cards to 0% balance-transfer offers. Negotiating lower interest rates with current lenders. Consolidating multiple debts into a single lower-rate loan. Cutting subscriptions. Switching broadband or mobile contracts. Challenging council tax bands. Shopping at cheaper supermarkets. These moves reduce outgoings without lifestyle sacrifice, freeing cash for debt repayment. Re-run your budget after implementing pain-free changes to see the new surplus, then decide how much of it goes to extra debt payments versus building a small emergency buffer.

Warning signs that debt is becoming unmanageable include rising minimum payments month-on-month, using credit to pay for essentials like groceries or bills, borrowing from one card to pay another, missing payment deadlines, or feeling constant anxiety about money. If you recognize these patterns, contact a free, non-profit debt advice agency (Citizens Advice, StepChange, or National Debtline) before the situation worsens. A budget planner helps you arrive at that conversation with accurate data: what you earn, what you owe, what you spend, and what’s realistically available for repayment.

Digital vs Printable Budget Planners: Choosing the Format That Fits Your Lifestyle

The choice between digital and printable budget planners comes down to how you think, where you work, and what kind of interaction keeps you engaged.

| Format | Key Benefits |

|---|---|

| Printable PDF worksheets | Tactile, visual, no screen time, easy to pin on fridge or filing system |

| Excel or Google Sheets | Automatic calculations, customizable formulas, version control, sharable across household |

| Budgeting apps (Monzo, Starling, Chase) | Bank-feed integration, real-time balance updates, automatic categorization, mobile notifications |

| Standalone budgeting software | Advanced features like goal tracking, net-worth dashboards, investment links, multi-year forecasting |

Digital planners that integrate with your bank account can pull transactions automatically, categorize spending based on merchant names, and update your budget in real time without manual data entry. You open the app, see today’s balance, check which category is overspent, and adjust on the spot. Dashboards visualize spending trends with charts and color-coded alerts, making it easier to spot patterns. Grocery spending spiking every weekend. Subscriptions you forgot existed. Impulse purchases clustering around stressful weeks. Some apps let you photograph receipts, attach them to transactions, and search your spending history by keyword, date, or category.

Physical planners (printed spreadsheets, budget binders, or downloadable PDF worksheets) suit people who think better with pen and paper, want to disconnect from screens, or find the act of writing numbers reinforces awareness. Filling out a printed budget at the kitchen table, calculator in hand, can feel more intentional than tapping through an app. The planner becomes a physical artifact you review weekly, not a background process you ignore. For households budgeting together, a shared printable worksheet on the fridge provides a constant visual reminder that both partners see daily.

When selecting a budgeting app, look for these five features:

- Bank-feed integration, automatic import of transactions without CSV uploads or manual typing

- Customizable categories, ability to rename, add, split, or merge spending buckets to match your life

- Real-time alerts and notifications, warnings when a category nears its cap or a bill is due

- Savings-pot or envelope functionality, virtual spaces to separate money by purpose within one account

- Export and reporting tools, downloadable summaries for tax, mortgage applications, or long-term review

The best format is the one you’ll actually use month after month. If the friction of opening a spreadsheet means you skip updates, switch to an app. If app notifications stress you out and you prefer weekly sit-down reviews, print a template. The mechanics of the planner matter far less than consistent engagement with the data it contains.

Monthly Review Routine: Using Your Budget Planner to Adjust, Reconcile, and Stay on Track

A budget planner isn’t a set-it-and-forget-it document. It’s a living tool that only works if you reconcile it against reality every month. Reconciliation means comparing what you planned to spend with what you actually spent, identifying variances, understanding why they happened, and adjusting future months to reflect new information. Set a recurring calendar reminder (last day of the month, first weekend, payday) and treat the review as a non-negotiable appointment with your finances.

Start by pulling the month’s actual transactions from your bank, credit card, and cash spending. Match each transaction to a budget category, flagging anything that doesn’t fit or surprises you. Check whether you stayed within each category cap. If groceries were budgeted at £300 but you spent £340, note it and ask why. Did prices rise? Did you host guests? Did you waste food? Or was £300 never realistic? If the overspend was one-time (birthday cake, dinner party), leave the budget as-is. If it’s a pattern, raise the grocery cap and find savings elsewhere. Update any recurring costs that changed (new mobile contract, gym membership increase, subscription cancellation) so next month’s plan reflects current reality.

Review progress toward savings goals and debt-repayment targets. Did you fund your sinking funds as planned? Did you make extra payments on high-interest debt? If not, identify what blocked it. Unexpected expense? Income shortfall? Discretionary overspend in another category? Decide whether to adjust next month’s allocations or tighten spending to stay on track. Check your emergency fund balance and net worth (assets minus liabilities) if you track it, noting whether the trend is upward, flat, or downward over the past three or six months.

Monthly reconciliation checklist:

- Download and categorize all transactions from the past month.

- Compare actual spending to budgeted amounts in every category.

- Identify and investigate variances over 10% or £20, whichever is larger.

- Update recurring bills, subscriptions, and fixed costs that changed.

- Confirm all sinking-fund and savings-goal contributions were made.

- Adjust next month’s budget caps based on realistic patterns, not wishful thinking.

This routine turns the budget from a static wish list into a feedback loop. Each month’s actuals teach you something about your habits, your income stability, your true costs, and your priorities, and you fold that learning into the next iteration. Over time, your budget becomes more accurate, more sustainable, and more aligned with the life you actually live.

Planning for Major Life Events With Your Budget Planner

Major life events require long-term financial planning that a monthly budget alone can’t handle. Weddings. Home renovations. College or university funds. New-baby costs. Extended travel. Elder care. A budget planner supports these goals by creating dedicated sinking funds with multi-month or multi-year timelines, so you accumulate the money gradually rather than borrowing or raiding emergency savings when the event arrives.

The planning process starts with a realistic cost estimate. Research typical costs for the event, add a 10 to 20% buffer for surprises, then divide the total by the number of months until you need it. That monthly figure becomes a line item in your budget, funded automatically just like rent or insurance. A wedding budgeted at £12,000 in two years requires £500 per month. A home extension estimated at £30,000 in three years needs roughly £833 per month. If the monthly amount feels impossible, you have three choices: extend the timeline, reduce the scope, or find additional income.

| Event | Typical Timeline | How to Budget Monthly |

|---|---|---|

| Wedding | 12 to 24 months | Total cost ÷ months = monthly sinking-fund contribution |

| Home renovation | 24 to 36 months | Total estimate + 15% buffer ÷ months until start |

| University fund (child age 10) | 8 years (96 months) | Estimated fees + maintenance ÷ 96 months, adjusted annually |

| Extended travel (sabbatical year) | 18 to 36 months prep | Lost income + travel costs ÷ months of saving beforehand |

| New-baby costs (first year) | 9 months pregnancy + 3-month buffer | Cot, pram, clothes, childcare deposits ÷ 12 months |

Long-range sinking funds prevent the debt accumulation that derails financial stability. When you fund a wedding over two years instead of putting it on credit cards, you avoid thousands in interest charges and start married life without a debt hangover. When you save for home repairs in advance, a broken boiler or leaking roof becomes an inconvenience, not a crisis that forces you into high-interest loans. The budget planner makes these large, distant goals tangible by breaking them into small, manageable monthly actions that fit within your current income.

Aligning major-event planning with your broader financial picture ensures you don’t sacrifice retirement contributions, emergency-fund growth, or debt repayment to fund a single goal. The planner shows the trade-offs: if you allocate £500 monthly to a wedding fund, that’s £500 not available for other priorities. Adjust category caps, delay discretionary spending, or find additional income to keep all goals moving forward without abandoning long-term security for short-term celebration.

Long-Term Financial Planning Through Your Budget Planner

A budget planner bridges the gap between day-to-day cash flow and decade-long financial goals by tracking not just this month’s bills but next decade’s retirement income, investment contributions, and net-worth trajectory. Long-term planning inside a budget starts with defining your target retirement age and estimating annual expenses in retirement, then working backward to calculate how much you need to save monthly to reach that goal. Pension contribution calculators and retirement forecasting tools provide rough targets, but your budget planner is where you make those targets real by allocating actual pounds from actual income.

If your employer offers a pension scheme with matching contributions, the budget planner should reflect your payroll deduction (if you enter net pay) or show the contribution as a separate expense line (if you enter gross pay and manually list deductions). Workplace pensions often deduct before tax, reducing your taxable income and lowering what you pay in income tax and National Insurance. Personal pensions or SIPPs (Self-Invested Personal Pensions) funded via direct debit appear as monthly expenses in your budget, competing for space with rent, groceries, and debt repayment. The planner forces the question: can you afford to increase pension contributions this year, or does clearing high-interest debt take priority?

Investment contributions (ISAs, general investment accounts, or regular savings into index funds) appear in the budget as monthly outflows just like any other financial goal. A stocks-and-shares ISA contribution of £200 per month totals £2,400 annually, well within the current £20,000 annual ISA allowance, and builds a tax-free pot for medium and long-term growth. The budget shows whether that £200 is genuinely available after essentials, debt payments, and emergency-fund contributions, or whether you’re funding investments by underfunding more urgent priorities. Some planners include net-worth tracking, where you log asset values (pension balance, ISA value, property equity, cash savings) and liabilities (mortgage, loans, credit cards) monthly or quarterly, so you can see whether your financial position is improving over time even if monthly cash flow feels tight.

Financial independence and FIRE (Financial Independence, Retire Early) planning layers onto traditional budgeting by calculating your “FI number,” the invested sum that generates enough passive income to cover annual expenses indefinitely, typically 25 times annual spending using the 4% withdrawal rule. If your budget shows £30,000 annual expenses, your FI number is roughly £750,000. The planner helps you track progress by showing monthly investment contributions, portfolio growth, and the gap between current net worth and the target. Adjust spending downward or income upward, and the timeline to FI shortens. Lifestyle inflation or debt accumulation pushes it further out.

Annual review tasks for long-term planning:

- Recalculate retirement-income needs based on current lifestyle and expected changes (downsizing, travel, healthcare).

- Increase pension or investment contributions in line with salary rises or windfalls.

- Rebalance portfolio allocations if they’ve drifted from target risk levels.

- Update FI number if annual expenses changed materially (mortgage paid off, children left home, new recurring costs).

Long-term financial planning through your budget planner ensures today’s spending decisions align with tomorrow’s freedom. The planner shows the trade-off in real terms: spending an extra £100 monthly on takeaways versus investing that £100 at 7% annual growth compounds to over £50,000 in twenty years. The choice is yours, but the planner makes the choice visible.

Budget Planner Troubleshooting and Common Mistakes to Avoid

Even well-intentioned budget planners fail when common mistakes go uncorrected. Recognizing these pitfalls early and adjusting the system prevents the frustration that leads people to abandon budgeting altogether.

Underestimating one-off and irregular costs is the most frequent error. A budget that only accounts for monthly bills looks balanced until Christmas, car insurance, birthday gifts, and holiday costs all land in the same quarter and blow the plan apart. The fix is simple but requires discipline: identify every annual, biannual, or seasonal expense, convert it to a monthly equivalent, and enter it as a recurring line item. If you skip this step, your budget will fail every few months, and you’ll conclude budgeting “doesn’t work” when the real problem is incomplete inputs.

Ignoring forgotten subscriptions and auto-renewals drains hundreds of pounds annually without conscious spending decisions. Streaming services, magazine subscriptions, app memberships, cloud storage, domain renewals, software licenses, gym contracts you stopped using. All quietly renew until you audit transaction history and cancel what no longer serves you. A monthly reconciliation process catches these leaks, but only if you actually review every transaction rather than scanning totals.

Common budgeting mistakes and how to fix each:

- Setting caps based on wishful thinking, not transaction history. Fix: Use actual past spending to set realistic starting caps, then reduce them gradually.

- Budgeting to highest monthly income when income varies. Fix: Budget to your lowest expected monthly income, treat extra income as bonus for savings or one-time goals.

- Lumping dissimilar costs into vague “miscellaneous” categories. Fix: Split broad categories into specific buckets (groceries vs dining out vs takeaways).

- Forgetting to update the budget when life changes. Fix: Review and adjust caps after any major event (move, job change, new baby, car purchase).

- Treating the budget as punishment rather than a decision-making tool. Fix: Frame caps as permission to spend up to that amount guilt-free, not as deprivation.

- Failing to negotiate recurring bills. Fix: Contact providers annually to request retention discounts, price-match competitors, or switch to cheaper alternatives.

- Not separating credit card spending from credit card debt repayment. Fix: Enter purchases under spending categories, only log the interest and fees under “debt costs.”

If your income is irregular (freelance, commission-based, seasonal, zero-hours contracts), budget to the lowest monthly income you’ve earned in the past year, not an optimistic average. In higher-income months, the surplus goes to sinking funds, emergency savings, or debt repayment rather than lifestyle inflation. This approach prevents the cycle where flush months fund overspending that crashes when lean months arrive. Some planners support multiple income scenarios or rolling three-month averages, which smooth volatility without pretending it doesn’t exist.

Subscription management deserves its own monthly audit. Create a master list of every recurring charge (name, cost, renewal date, cancellation method) and review it quarterly. Cancel anything unused, downgrade over-spec services, and consolidate where possible (family plans, bundled services). Typical households carry £10 to £30 in forgotten or underused subscriptions. Over a year, that’s £120 to £360 reclaimed without sacrificing anything meaningful.

The goal of troubleshooting isn’t perfection. It’s continuous improvement. Every month you reconcile actuals against the plan, you learn something. Every mistake you catch and correct makes next month’s budget more accurate. Over time, the planner becomes a true reflection of your financial life, and the decisions it informs become clearer, faster, and more confident.

Final Words

You built a working budget planner: gathered statements, categorized income and expenses, chose a method (zero-based, 50/30/20, or envelope), and set monthly amounts.

We covered converting irregular costs, setting realistic category caps, sinking funds, debt-repayment tactics, and picking digital or printable formats.

Start with a template, run monthly reviews, and adjust as life changes. Your budget planner will reveal spending leaks and keep priorities clear. You’re set to make steady, manageable progress.

FAQ

Q: What is the 50 30 30 budget rule?

A: The 50/30/30 budget rule is not a common standard and is likely a misremembering; the typical rule is 50/30/20: 50% needs, 30% wants, 20% savings or debt repayment.

Q: What is the 50 30 20 rule of money?

A: The 50/30/20 rule of money divides after-tax income into 50% essentials (rent, bills), 30% wants (dining, entertainment), and 20% savings or debt repayment, a simple starting framework.

Q: What is the best free budget planner?

A: The best free budget planner depends on your needs: use Google Sheets or Excel templates for control, Mint for bank feeds and automatic categorisation, or Goodbudget for envelope-style tracking.

Q: What is the 50 40 10 budget rule?

A: The 50/40/10 budget rule allocates 50% to needs, 40% to wants, and 10% to savings; it suits people who prioritise current spending or have short-term savings goals.