{kind=link}

Think the cheapest plan is always the best? Think again.

Choosing health coverage means balancing monthly cost, out-of-pocket risk, and which doctors are in-network.

Most people qualify for multiple pathways—employer plans, Marketplace, Medicaid/CHIP, Medicare, COBRA—so the right choice depends on your income, health needs, and timing.

This guide walks you through the main options, core plan types (HMO, PPO, EPO, POS), and the real costs you’ll face, so you can compare plans that fit your life, not just your budget.

Understanding Your Core Health Coverage Choices

When you’re shopping for health insurance, you’re choosing from several major systems. Each one has its own rules, timelines, and eligibility gates. Most people qualify for at least two or three of these pathways, so knowing what’s available and when you can enroll is where you start.

The five largest categories are employer-sponsored group plans (where your job offers coverage and often pays most of the premium), Health Insurance Marketplace plans (also called ACA or “Obamacare” plans, sold individually or to families), Medicaid and the Children’s Health Insurance Program (CHIP, both income-based and run by states), Medicare (primarily for people 65 and older or those with certain disabilities), and COBRA continuation coverage (which lets you keep your old employer plan temporarily after you leave a job). There are also private short-term plans and supplemental policies that fill specific gaps, though those usually don’t replace comprehensive coverage.

Eligibility and enrollment windows vary widely. Medicaid and CHIP accept applications year-round in most states. If your income is at or below 138% of the federal poverty level in an expansion state (roughly $20,120 for one person in 2024), you likely qualify for Medicaid. Marketplace plans have a designated Open Enrollment period each year, typically running from November 1 through mid-January, plus Special Enrollment Periods that open for 60 days after life changes like losing other coverage, getting married, or having a baby. Medicare has a 7-month Initial Enrollment Period surrounding your 65th birthday (three months before, the month of, and three months after) and an Annual Election Period from October 15 to December 7 for switching plans. COBRA gives you 60 days to elect continuation after your employer coverage ends, and you can usually stay on it for 18 months (sometimes up to 36 months in special cases).

Here’s a quick snapshot of the primary coverage categories:

Employer-sponsored plans: group coverage offered through your job. Your employer usually pays a large share of the premium (often 70 to 90% for single coverage), and you pay the rest via payroll deduction.

Marketplace / ACA plans: individual and family plans sold through state or federal exchanges. Income-based premium tax credits and cost-sharing reductions can reduce monthly premiums to $0 for eligible households.

Medicaid and CHIP: state-federal programs offering free or very low-cost coverage to low-income individuals, children, pregnant people, elderly, and disabled. Eligibility rules vary by state, and enrollment is generally year-round.

Medicare: federal health insurance for people 65+ or those with certain disabilities. Includes Part A (hospital), Part B (medical), Part C (Medicare Advantage), and Part D (prescription drugs).

COBRA: temporary continuation of your former employer’s plan after job loss or other qualifying events. You pay the full premium plus up to 2% administration fee, and coverage typically lasts 18 months.

Private and short-term plans: non-group policies that may exclude preexisting conditions and ACA-required benefits. Durations often range from 1 to 12 months depending on state rules. These work for narrow gaps but aren’t comprehensive long-term solutions.

Comparing Health Insurance Plan Structures and Networks

Once you know which coverage category fits your situation, the next decision is which type of plan design works for how you use care. Most plans fall into one of four network structures: HMO, PPO, EPO, or POS. Each one sets different rules about which doctors you can see, whether you need referrals, and what happens if you go out of network.

An HMO (Health Maintenance Organization) usually offers the lowest premiums and deductibles, but it requires you to pick a primary care physician (PCP) and get a referral before seeing a specialist. You’ll pay very little if you stay in network, but out-of-network care is rarely covered except in true emergencies. A PPO (Preferred Provider Organization) gives you the freedom to see any provider without a referral and still get some coverage if you go out of network, though you’ll pay higher cost-sharing for out-of-network visits. And PPO premiums tend to be higher from the start. An EPO (Exclusive Provider Organization) sits in between: you don’t need referrals, but you must stay in network (except emergencies) or you’ll pay the full bill yourself. A POS (Point of Service) plan blends HMO and PPO features. You choose a PCP and need referrals for specialists, but the plan offers limited out-of-network coverage at higher cost.

Here’s a quick summary of each plan structure:

HMO: in-network only, PCP required, referrals for specialists, lowest premiums. Best if you want predictable costs and don’t mind coordination through one doctor.

PPO: broad network access, no referrals, out-of-network coverage available, higher premiums. Best if you want flexibility and are willing to pay more for it.

EPO: in-network only, no referrals, moderate premiums. Good middle ground if you don’t need out-of-network care but want to skip the referral process.

POS: PCP and referrals required, limited out-of-network coverage. Less common. Works if you want some PPO-like flexibility with lower HMO-like premiums.

All of these plan types control costs by building networks of doctors and hospitals who agree to accept negotiated rates. Before you enroll, check the plan’s provider directory online to confirm your current primary care doctor, specialists, and preferred hospital are in network. Networks can be narrow, especially in lower-cost plans, and switching plans mid-year is usually not allowed unless you have a qualifying life event.

Key Differences Between HMO and PPO Plans

The HMO-versus-PPO choice is the most common trade-off you’ll face. HMOs save you money by limiting choice: you stay in network, you coordinate care through one PCP, and the plan pays very little (or nothing) if you wander outside the network. That structure keeps premiums and deductibles low, and copays are often modest. $20 to $40 for a primary care visit is typical. If you’re comfortable with that coordination and your preferred doctors are in the HMO network, the savings can be significant.

PPOs cost more each month, but they let you see specialists without asking permission, and they still cover a portion of out-of-network care (you’ll just pay a higher deductible and coinsurance). If you travel frequently, need out-of-state specialists, or want the certainty that you won’t be locked into a narrow list of providers, the PPO premium is the price of that flexibility. The real-world difference shows up when you need unexpected care: an HMO might require prior authorization and a referral chain even for urgent specialist visits, while a PPO lets you book directly and still get partial reimbursement even if the specialist isn’t contracted.

Understanding Plan Costs and Out-of-Pocket Rules for Health Coverage

Health insurance costs aren’t just the monthly bill. Every plan has multiple cost layers: premium, deductible, copays, coinsurance, and an out-of-pocket maximum. Understanding how they stack up is the only way to predict what you’ll actually pay in a year.

The premium is what you pay every month whether you use care or not. After subsidies, Marketplace premiums can drop to $0 for low-income households. Without subsidies, individual premiums commonly range from $200 to $700+ per month depending on age, location, and plan type. The deductible is the amount you pay out of pocket before the plan starts sharing costs. It can be as low as $0 on some plans or as high as $8,000+ on high-deductible health plans (HDHPs). Once you hit the deductible, most plans use copays (a flat fee per visit, often $10 to $50 for primary care, higher for specialists) or coinsurance (a percentage split, commonly 10% to 50% of the bill, with you paying the smaller share). Your out-of-pocket maximum is the legal cap on what you pay in a year for covered in-network services. After you reach that limit, the plan pays 100%. The Affordable Care Act sets annual limits on out-of-pocket maximums. Check the current year’s numbers, as they adjust annually.

| Cost Component | Typical Range | Notes |

|---|---|---|

| Premium | $0–$700+/month (individual) | Can be $0 after subsidies; employer plans often heavily subsidized by the company. |

| Deductible | $0–$8,000+/year | Amount you pay before plan cost-sharing starts; HDHPs have higher deductibles but may pair with tax-advantaged HSAs. |

| Copay | $10–$50+ per visit | Flat fee per service; specialist copays typically higher than primary care. |

| Coinsurance | 10%–50% | Your share of costs after deductible; 20% coinsurance means you pay 20%, plan pays 80%. |

| Out-of-Pocket Maximum | Varies (ACA sets annual caps) | Once reached, plan pays 100% of covered in-network care for rest of year; caps update annually. |

| Cost-Sharing Reductions / Premium Tax Credits | Income-based | Marketplace subsidies that lower premiums and/or deductibles, copays, and OOP max; eligibility tied to household income as % of federal poverty level. |

To estimate your total annual cost, multiply your monthly premium by 12, then add your expected out-of-pocket spending. If you anticipate regular doctor visits or prescriptions, use the deductible plus estimated copays and coinsurance. If you’re generally healthy and rarely see a doctor, you might only pay the premium and perhaps a few copays. For example, Plan A with a $300/month premium and $1,500 deductible costs $3,600 in premiums plus up to $1,500 in medical costs before coinsurance kicks in. Plan B with a $450/month premium and $0 deductible costs $5,400 in premiums but you start copay-only visits immediately. If you expect less than $1,800 in care, Plan A is cheaper. If you expect frequent visits or a planned surgery, Plan B might save money overall. Always run the math with your own expected use.

ACA Marketplace Health Coverage Options and Plan Tiers

Marketplace plans are organized into metal tiers: Bronze, Silver, Gold, Platinum, and Catastrophic. They represent how much of your total medical costs the plan is designed to cover on average. These tiers don’t measure quality or network size. They measure cost-sharing structure.

A Bronze plan has an actuarial value around 60%, meaning the plan pays roughly 60% of covered costs across all enrollees and you pay the other 40% through deductibles, copays, and coinsurance. Bronze plans have the lowest monthly premiums but the highest out-of-pocket exposure. Deductibles often range from $6,000 to $8,000+. They work well if you’re healthy, rarely visit the doctor, and want catastrophic protection without a high monthly bill. Silver plans sit at roughly 70% actuarial value and are the sweet spot for many people because they unlock cost-sharing reductions if your income qualifies. Those reductions lower your deductible, copays, and out-of-pocket max beyond what the metal tier alone provides. Gold plans cover about 80% of costs with higher premiums and lower deductibles (often $0 to $2,000). They’re a good match if you expect regular care, prescriptions, or a planned procedure. Platinum plans hit roughly 90% coverage with the highest premiums and lowest cost-sharing. Best for people with chronic conditions or high expected use. Catastrophic plans are available only to people under 30 or those with a hardship exemption. They have very low premiums and very high deductibles, covering only three primary care visits and preventive services before the deductible, then everything else after you hit the out-of-pocket max.

Open Enrollment for Marketplace plans typically runs from November 1 through mid-January each year, though exact dates can shift and some states run their own extended timelines. If you miss Open Enrollment, you can still enroll during a Special Enrollment Period if you have a qualifying life event: losing other coverage, getting married, having or adopting a child, or moving to a new coverage area. Special Enrollment Periods usually last 60 days from the date of the event. Premium tax credits and cost-sharing reductions are income-based and calculated as a percentage of the federal poverty level. If your household income falls within the eligible range (historically 100% to 400% of FPL, expanded in recent policy changes), you may qualify for monthly premium credits that are applied directly to your bill.

Here’s a quick summary of the metal tiers:

Bronze: around 60% actuarial value. Lowest premiums, highest deductibles and cost-sharing. Good for low expected care and catastrophic protection.

Silver: around 70% actuarial value. Moderate premiums. Unlocks cost-sharing reductions for eligible incomes. Often the best value for subsidized buyers.

Gold: around 80% actuarial value. Higher premiums, lower deductibles and copays. Ideal for regular doctor visits, ongoing prescriptions, or planned surgeries.

Platinum: around 90% actuarial value. Highest premiums, lowest out-of-pocket costs. Best for chronic conditions or very high expected use.

Catastrophic: available only under age 30 or with hardship exemption. Very low premium, very high deductible, covers three primary visits and preventive care before deductible. Emergency safety net only.

Government Health Coverage Options: Medicare, Medicaid, and CHIP

Medicare is federal health insurance primarily for people age 65 and older, though it also covers younger individuals who’ve received Social Security Disability Insurance (SSDI) for 24 months or have certain conditions like end-stage renal disease or ALS. Medicare is divided into parts: Part A covers inpatient hospital stays and has no premium for most people (if you or your spouse paid Medicare taxes for at least 10 years of work). Part B covers doctor visits, outpatient care, and medical equipment and charges a standard monthly premium (around $174.70 in 2024 for most enrollees, though higher earners pay more). You can also choose Part C, known as Medicare Advantage, which bundles A and B (and often Part D prescription coverage) into one plan sold by private insurers. These plans usually add extra benefits like dental or vision but require you to use a network. Part D is standalone prescription drug coverage. If you don’t enroll when first eligible and lack other creditable coverage, you face a late-enrollment penalty that lasts as long as you have Part D.

Your Initial Enrollment Period for Medicare is a 7-month window: the three months before your 65th birthday, your birthday month, and the three months after. If you’re still working and covered under a large employer plan (20+ employees), you can delay Part B without penalty, but you must enroll within 8 months of leaving that job. The Annual Election Period runs October 15 through December 7 each year, and that’s when you can switch between Original Medicare and Medicare Advantage or change Part D plans.

Medicaid is a joint federal-state program that provides free or very low-cost coverage to low-income individuals and families. Eligibility rules vary by state, but in states that expanded Medicaid under the ACA, you generally qualify if your income is at or below 138% of the federal poverty level. About $20,120 for one person or $41,400 for a family of four in 2024. Children, pregnant people, elderly individuals, and people with disabilities may qualify at higher income levels depending on the state. The Children’s Health Insurance Program (CHIP) covers children in families whose income is too high for Medicaid but too low to afford private coverage. Income limits vary by state. Both Medicaid and CHIP allow year-round enrollment. There’s no waiting for an open enrollment window.

Here’s what each program typically covers:

Medicare Part A: inpatient hospital stays, skilled nursing facility care, hospice, some home health. Usually no premium if work history qualifies.

Medicare Part B: doctor visits, outpatient services, preventive care, durable medical equipment. Requires monthly premium.

Medicare Part D: prescription drug coverage sold by private insurers. Separate premium, formularies vary by plan.

Medicaid/CHIP: comprehensive coverage including doctor visits, hospital care, prescriptions, preventive services, mental health, and often dental and vision for children. Little to no premium or cost-sharing.

How Medicare Advantage Differs From Original Medicare

Medicare Advantage (Part C) is an alternative to Original Medicare (Parts A and B). Private insurers contract with Medicare to deliver all Part A and Part B benefits, and usually Part D drug coverage, under one plan. Most Medicare Advantage plans use HMO or PPO network structures, so you’ll follow the same referral and network rules you would in any HMO or PPO. Many Advantage plans add extra benefits like routine dental, vision, hearing, or gym memberships, and some have $0 premiums (though you still pay the Part B premium to Medicare).

The trade-off is network restrictions and prior authorization requirements that don’t exist in Original Medicare. With Original Medicare, you can see any doctor or hospital that accepts Medicare nationwide, and there are no referrals or network limits. If you want that flexibility and are willing to pay for a Medigap supplemental policy to cover the gaps (Part A and B deductibles, coinsurance, and some copays), Original Medicare might fit better. If you prefer a single plan with predictable copays, bundled drug coverage, and extra perks, and you’re comfortable with a network, Medicare Advantage is often simpler and cheaper month-to-month.

Short-Term, Supplemental, and Specialized Health Coverage Options

Short-term health insurance is exactly what it sounds like: temporary coverage designed to fill a gap between jobs, during a move, or while you wait for other coverage to start. These plans are not ACA-compliant. They can exclude preexisting conditions, cap benefits, and skip certain health benefits like maternity or mental health care. Durations vary by state, ranging from one month up to 12 months per term, and some states ban them entirely. Premiums are usually lower than Marketplace plans, but you’re trading comprehensive protection for temporary emergency coverage. If you have any ongoing health conditions or expect to need real care during the gap, short-term plans often leave you exposed.

Supplemental insurance products fill specific needs rather than replacing comprehensive coverage. Accident insurance pays a lump sum or set benefits if you’re injured. Think broken bones, ER visits, or ambulance rides. Critical illness coverage pays a cash benefit if you’re diagnosed with a serious condition like cancer, heart attack, or stroke. You can use the money however you need (medical bills, mortgage, lost wages). Hospital indemnity plans pay a daily or per-admission benefit when you’re hospitalized, regardless of your other coverage. Long-term care insurance covers custodial care, help with daily activities like bathing, dressing, or eating, when you can no longer live independently, whether at home, in assisted living, or in a nursing facility. These policies are expensive and have strict eligibility rules, so most people buy them in their 50s or early 60s before health issues arise.

Here are the three most common supplemental types:

Accident insurance: pays set benefits for injuries. Useful if you have a high-deductible plan or want extra cash for out-of-pocket costs after an accident.

Critical illness: lump-sum cash benefit for serious diagnoses. Helps cover expenses your health plan doesn’t, like experimental treatments, travel, or income loss.

Hospital indemnity: daily or per-stay cash benefit when you’re admitted to a hospital. Supplements your main plan by offsetting deductibles, copays, or non-medical costs.

Prescription Drug Coverage Within Health Coverage Options

Every health plan includes some level of prescription drug coverage, but what’s covered, how much you pay, and which pharmacies you can use all depend on the plan’s formulary. A formulary is the plan’s official list of covered medications, organized into tiers that determine your cost-sharing. Tier 1 usually includes the cheapest generic drugs with the lowest copay, often $5 to $15. Tier 2 covers preferred brand-name drugs with moderate copays. Tier 3 and 4 tiers include non-preferred brands and specialty drugs, where you might pay 25% to 50% coinsurance instead of a flat copay. Some drugs aren’t on the formulary at all, meaning you pay full price unless you get an exception.

Plans also use tools like prior authorization (the plan must approve the drug before it’s covered), step therapy (you must try a cheaper drug first and fail before the plan covers the more expensive one), and quantity limits (only a certain number of pills per month). Specialty drugs, biologics, infusion therapies, drugs for cancer, MS, HIV, or rare diseases, often sit in the highest tier and require specialty pharmacies. If you take regular medications, check the formulary before you enroll and confirm your drugs are covered, what tier they’re in, and whether any restrictions apply. Medicare Part D plans all have formularies, and switching Part D plans during the Annual Election Period is one way to lower drug costs if your current formulary changes.

Here’s a typical formulary tier breakdown:

Tier 1 (Generic): lowest cost-sharing, often $5 to $15 copay. Preferred first-line drugs.

Tier 2 (Preferred Brand): moderate copay, $30 to $60 typical. Brand-name drugs the plan favors.

Tier 3 (Non-Preferred Brand): higher copay or coinsurance, $75 to $150+. Less favored brands.

Tier 4 (Specialty): coinsurance often 25% to 50%. Expensive or complex drugs, may require specialty pharmacy and prior authorization.

How to Choose the Right Health Coverage Option

Choosing the right health coverage starts with a clear picture of your health needs, your budget, and the providers and prescriptions you depend on. Most people focus only on the monthly premium, but that number alone doesn’t tell you what you’ll pay when you actually use care. The real cost is your annual premium plus your expected out-of-pocket spending. And the only way to estimate that is to think through how often you see the doctor, what medications you take, and whether you have any planned procedures or ongoing conditions.

Start by listing your current doctors, specialists, and preferred hospital, then cross-check them against each plan’s provider directory. If your primary care doctor or a critical specialist isn’t in network, either pick a different plan or be ready to pay out-of-network rates (or switch providers). Next, pull up your prescription list and check each plan’s formulary for coverage, tier placement, and any restrictions like prior authorization. A plan with a $50 lower premium might cost you hundreds more per month in drug costs if your medications sit in a high tier. Then estimate your annual costs: multiply the monthly premium by 12, add the deductible if you expect to meet it, and add estimated copays or coinsurance for your typical visits and prescriptions. Compare that total across three to five plans (bronze, silver, and gold tiers, or HMO versus PPO options) and the lowest total annual cost is usually the best financial fit.

Here are six steps to guide your decision:

-

List your must-haves: current doctors, specialists, hospital, and all prescriptions. Confirm each is available in-network and on the formulary before you narrow your list.

-

Estimate your annual use: count expected doctor visits, specialist appointments, regular prescriptions, and any planned surgeries or treatments.

-

Calculate total annual cost for each plan: (monthly premium × 12) + deductible (if you expect to meet it) + estimated copays and coinsurance. The plan with the lowest total wins on pure cost.

-

Check enrollment deadlines and eligibility: confirm you’re applying during Open Enrollment, a Special Enrollment Period, or year-round Medicaid enrollment, and gather required documents.

-

Review financial assistance: if you’re shopping the Marketplace, run the subsidy calculator to see if premium tax credits or cost-sharing reductions apply. Silver plans unlock the most help.

-

Read the fine print on exclusions and limits: confirm the plan covers the services you need (mental health, maternity, physical therapy) and check for waiting periods, annual or lifetime caps, or exclusions.

One helpful reality check: visit the plan’s website or call member services and ask if your top two or three providers are in network for the exact plan you’re considering. Provider directories online can be outdated, and confirming directly saves surprise bills later.

You can compare localized plan options and networks for individual and family coverage at Individual & Family Health Plans, and use plan comparison tools and provider lookups at UnitedHealthcare to evaluate cost and access side by side.

Balancing Cost and Access

The central trade-off in health insurance is simple: pay more each month for easier access and lower cost-sharing, or pay less each month and accept higher out-of-pocket costs and tighter networks. A low-premium Bronze plan or HMO saves you money upfront but requires you to stay in network, get referrals, and cover a large deductible before the plan starts sharing costs. A high-premium Gold plan or PPO costs more every month but gives you immediate copay-based access to any provider, no referrals, and a lower (or $0) deductible.

If you rarely see the doctor and have no ongoing prescriptions, the Bronze or HMO strategy often wins. You pocket the premium savings and only pay out of pocket in the rare event you need care. If you have regular appointments, take daily medications, or have a chronic condition, the higher premium usually pays for itself through lower deductibles, smaller copays, and predictable costs. The math is straightforward: subtract the annual premium difference between two plans, then compare that to the difference in expected out-of-pocket costs. If Plan A saves you $1,800 in premiums but costs you $2,500 more in deductibles and copays, Plan B is the better deal. The mistake most people make is picking the cheapest premium without checking the formulary, network, or deductible. And then facing a $6,000 surprise the first time they need care.

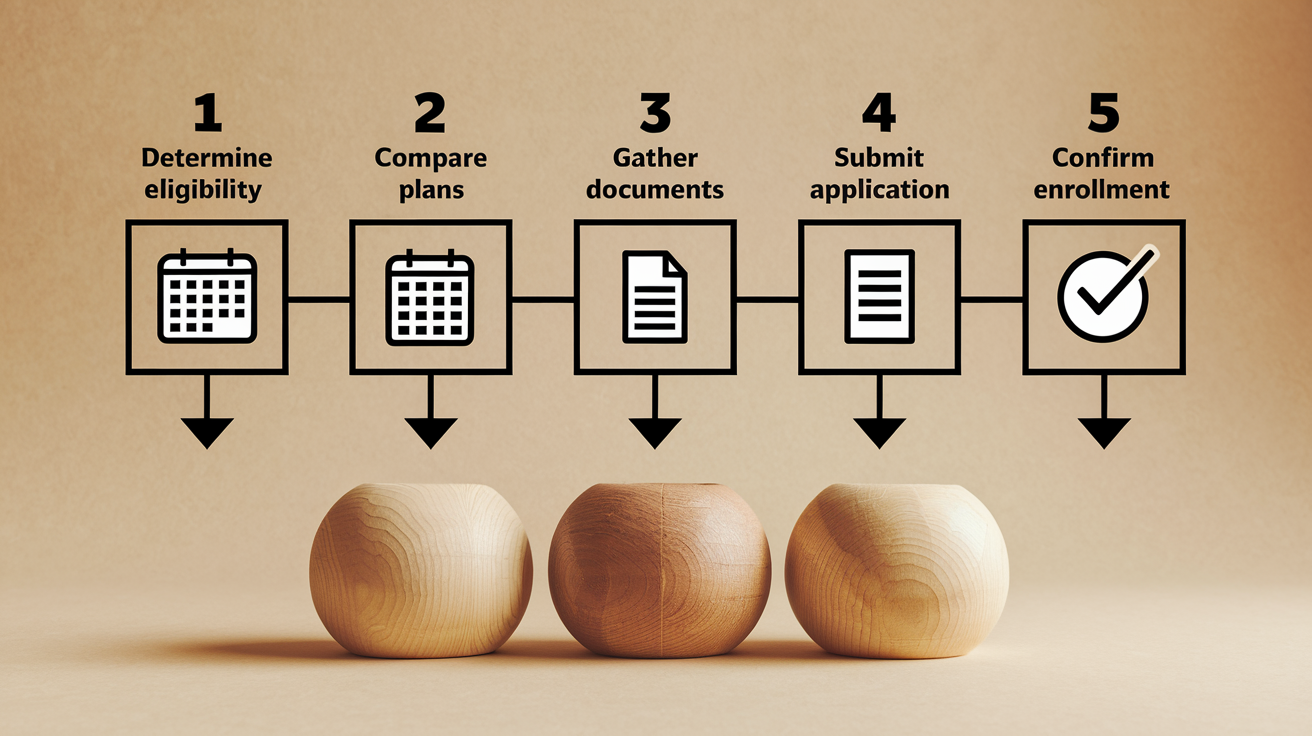

Enrollment Steps and Required Documentation for Health Coverage

Enrolling in health coverage is a multi-step process, and missing a document or deadline can delay your start date or lock you out until the next enrollment window. The exact steps depend on which type of coverage you’re applying for, but the core workflow is similar across Marketplace, Medicaid, Medicare, and employer plans.

First, confirm your eligibility category and the correct enrollment period. If you’re buying a Marketplace plan, check that it’s Open Enrollment (typically November 1 through mid-January) or that you have a qualifying life event that opens a Special Enrollment Period (usually 60 days from the event). For Medicaid or CHIP, you can apply any time. For Medicare, enroll during your Initial Enrollment Period or the Annual Election Period. For COBRA, you have 60 days from the date you lose employer coverage to elect continuation. Second, gather your documentation. Most applications ask for proof of income (recent pay stubs or last year’s tax return), Social Security numbers or tax identification numbers for everyone applying, proof of citizenship or lawful presence, and proof of any current or prior coverage (especially if you’re claiming a Special Enrollment Period). Third, compare at least three to five plans using the cost, network, and formulary checks described earlier, then select the one with the best total annual cost for your expected use. Fourth, complete the application online, by phone, or with the help of a navigator or broker (assistance is free for Marketplace and Medicaid applications). Fifth, pay your first month’s premium by the due date to activate coverage. Most plans won’t start until the first premium is received.

Here are five enrollment steps in order:

-

Determine your eligibility and enrollment window: confirm Open Enrollment dates, Special Enrollment Period qualification, Medicaid year-round access, or Medicare enrollment periods.

-

Gather required documents: Social Security numbers for household members, proof of income (pay stubs or tax return), proof of identity and residency, dates of prior coverage loss if claiming a Special Enrollment Period.

-

Compare plans: review at least 3 to 5 options on premium, deductible, network, formulary, and total annual cost. Use online comparison tools or work with a navigator.

-

Submit your application: complete the enrollment online, by phone, or in person. Double-check all information before submitting to avoid delays.

-

Pay your first premium on time: coverage typically starts the month after your application is processed and the first payment is received. Missing the payment deadline can cancel your enrollment.

Common documents you’ll need include recent pay stubs or your most recent federal tax return (to verify income for Marketplace subsidies or Medicaid), Social Security numbers or immigration document numbers for everyone applying, proof of residency (utility bill, lease, or driver’s license), and a termination letter or COBRA notice if you’re claiming loss of coverage as your qualifying event. If you’re enrolling in Medicare, you’ll also need your Social Security number and information about any current employer coverage to determine whether you should delay Part B. Keep copies of everything you submit, and save confirmation numbers and emails. You may need them if there’s a processing delay or dispute.

Final Words

Compare networks, costs, and prescription coverage first, that’s the heart of choosing a plan. This guide walked through major health coverage options, plan types like HMO vs PPO, Marketplace tiers, government programs, and supplements.

You also saw how premiums, deductibles, copays, and out-of-pocket max shape your real yearly cost, and how to estimate it. Plus the enrollment steps and documents to have ready.

Use these points to narrow options and pick the right health coverage options. You’re in control and ready to act.

FAQ

Q: What are the 4 types of insurance coverage?

A: The four main types of insurance coverage are life, health, property (home and auto), and liability (including umbrella policies). Each protects different risks, so choose based on your assets and needs.

Q: Does health insurance cover stroke?

A: Health insurance can cover a stroke—emergency care, hospital stays, imaging, medications, and rehab are typically covered. Coverage and out-of-pocket costs vary by plan, network, and prior authorization rules—check your benefits quickly.

Q: What is the best healthcare coverage plan?

A: The best healthcare coverage plan depends on your health needs, budget, preferred doctors, and prescriptions. Compare total annual cost, network access, and formularies, not just the monthly premium.

Q: What health insurance covers Zepbound?

A: Coverage for Zepbound depends on your insurer and plan; some employer, private, or Medicare Part D plans may cover it with prior authorization or step therapy. Check your formulary and ask your prescriber to verify coverage.