{kind=link}

Smokers often pay three to four times more for the same life insurance as nonsmokers.

That gap starts young and widens with age, turning a modest monthly bump into thousands over a policy’s life.

This post breaks down the real numbers, explains how insurers detect nicotine and cotinine, and shows when quitting actually lowers your rate.

If you’re shopping for coverage or planning to quit, you’ll get clear steps to find the cheapest fit for your needs.

Clear Cost Breakdown of Life Insurance for Smokers vs. Non‑Smokers

Smokers pay three to four times what nonsmokers pay for the same coverage. That gap gets worse as you age. Even younger people see their premiums jump the moment tobacco shows up in medical records or on an application. A modest-looking monthly increase turns into thousands of extra dollars over the policy’s life because of how the multiplier stacks up.

Here’s what the numbers actually look like for a 20-year term policy with $500,000 coverage. A 40-year-old male nonsmoker might pay around $450 a year. A male smoker at that same age pays close to $2,000. Women see the same pattern. A 40-year-old nonsmoker pays about $320 annually versus $1,200 if she smokes. That’s more than four times the nonsmoker rate.

| Age | Coverage | Nonsmoker Annual Premium | Smoker Annual Premium | Difference Multiplier |

|---|---|---|---|---|

| 30 (Male) | $500,000 | ≈ $250 | ≈ $700 | 2.8× |

| 40 (Male) | $500,000 | ≈ $450 | ≈ $2,000 | 4.4× |

| 50 (Male) | $500,000 | ≈ $1,200 | ≈ $4,800 | 4× |

| 40 (Female) | $500,000 | ≈ $320 | ≈ $1,200 | 3.8× |

| 40 (Female) | $100,000 | ≈ $192/year ($16/mo) | ≈ $612/year ($51/mo) | 3.2× |

These are estimates. Your quote will shift based on carrier, health, gender, and how underwriting shakes out. But the pattern holds. Smoking status drives your premium harder than almost anything else, often more than cholesterol or blood pressure.

How Insurers Classify Smoking Status in Life Insurance Pricing

If you’ve used any tobacco or nicotine in the past 12 months, you’re a smoker. Doesn’t matter if it’s a pack a day or one cigarette a week. The classification stays the same. And that definition catches products most people don’t think about, like nicotine gum or patches you’re using to quit. Those still put nicotine in your bloodstream, and they’ll show up on a cotinine test.

You’ll answer questions about tobacco history on the health questionnaire. The insurer backs that up with medical records and usually a paramedical exam that tests for nicotine through blood or urine. Cotinine is what your body makes when it breaks down nicotine, and it lingers way longer than nicotine itself. If cotinine shows up in your lab work, you’re getting classified as a smoker no matter what you wrote on the form.

Here’s what triggers smoker classification:

- Cigarettes (any brand, any amount)

- Cigars (though some carriers make exceptions for occasional use)

- Pipes

- Vaping and e-cigarettes

- Chewing tobacco, snuff, dip

- Nicotine patches, gum, lozenges, pouches

- Hookah

- Regular marijuana smoking (some carriers apply smoker rates because of lung risk)

A few insurers let occasional cigar smokers qualify for nonsmoker rates if total use stays under 24 cigars a year and lab tests come back clean. That rule varies by carrier. You’ll need to spell out your exact usage and timing to see if you qualify.

How Medical Exams and Nicotine Testing Affect Life Insurance Costs

Most fully underwritten policies require a paramedical exam with blood or urine testing for nicotine and cotinine. Cotinine is the metabolite your body produces when it processes nicotine, and it stays detectable far longer. That’s why insurers test for it. It catches tobacco use even if you haven’t smoked in days.

Detection windows change based on the test. Blood tests find nicotine for one to three days and cotinine for up to 10 days. Urine tests pick up cotinine for three to four days if you’re an occasional user, but heavy smokers can test positive for up to three weeks. Saliva tests detect nicotine for up to four days. Hair follicle tests reveal use for one to three months, though those aren’t common in standard underwriting.

Key timelines:

- Blood: nicotine 1 to 3 days, cotinine up to 10 days

- Urine: cotinine 3 to 4 days (occasional) or up to 3 weeks (heavy)

- Saliva: nicotine up to 4 days

- Hair: 1 to 3 months

If your cotinine comes back elevated, you’re getting classified as a smoker and priced that way. The test result beats whatever you wrote on the questionnaire. Avoiding smoking for a few days before your exam won’t help if you’re a regular user. The only way to pass is to stop all nicotine long enough for your body to clear cotinine completely.

Why Smokers Pay Higher Life Insurance Rates

Insurers price premiums on mortality risk, which is the statistical likelihood you’ll die during the coverage period. Tobacco use cranks that risk up by increasing your chances of cancer, heart disease, stroke, COPD, and a long list of other conditions that cut life expectancy short. Smokers get lung cancer, throat cancer, and cardiovascular events at higher rates than nonsmokers, and that data shows up consistently in the numbers insurers use to set rates.

Tobacco is the leading cause of preventable death in the U.S. Life insurers price that into every smoker’s premium. A smoker’s life expectancy is shorter than a nonsmoker’s, which means the insurer is more likely to pay a death benefit sooner. That increased likelihood turns directly into higher monthly or annual costs. The pricing reflects the additional financial risk the company takes on when it covers someone whose tobacco use raises the odds of an early claim.

Rate Classes and How Smoking Status Impacts Policy Pricing

Life insurance companies split applicants into rate classes based on overall health and longevity. The top tiers (preferred plus, preferred, standard plus) go to people with clean medical histories, healthy vitals, and no tobacco use. Smokers rarely land in those preferred categories. Instead, they get placed into standard smoker or table-rated classes, which cost significantly more.

A nonsmoker with strong health can land in preferred or preferred plus, where premiums are the lowest the carrier offers. Add tobacco to that same health profile and the insurer bumps you down to a smoker tier. Your premium jumps even if everything else about your health is excellent. Table ratings and flat extras apply when you’ve got additional risk on top of smoking, like high blood pressure or heart disease history. Those adjustments push the premium even higher.

Main rate categories smokers see:

- Standard smoker: baseline pricing for smokers with no other major health issues

- Table-rated smoker: extra surcharge when smoking combines with another risk factor

- Preferred smoker (rare): a few carriers offer a mid-tier smoker class if your health is otherwise spotless

Smoking alone often disqualifies you from the best pricing, no matter how well you score on other health measures. The mortality data on tobacco use is so clear that insurers treat it as a dominant risk factor.

How Long After Quitting You Can Qualify for Lower Life Insurance Costs

Most insurers want at least 12 months of complete tobacco and nicotine cessation before they’ll reclassify you as a nonsmoker. Some set the bar at 24 months. A handful ask for longer if your smoking history was heavy or you’ve got other health concerns. The clock starts the day you stop using all tobacco and nicotine products, including patches, gum, and vaping.

After you’ve been tobacco-free for the required period, you can request a rate reconsideration on your existing policy or apply fresh as a nonsmoker. Either way, you’ll need to pass a new medical exam with nicotine and cotinine testing to prove you’re clean. If you’ve quit for three to five years and kept your overall health strong, you might qualify for preferred or preferred plus nonsmoker rates, which are the lowest tiers most carriers offer.

| Smoke-Free Duration | Possible Rate Tier | Typical Requirements |

|---|---|---|

| 12 months | Standard nonsmoker | New medical exam, negative cotinine test, verification of quit date |

| 24 months | Standard or preferred nonsmoker | Same as above; some carriers require 24 months minimum |

| 3–5 years | Preferred or preferred plus | Clean exam, excellent health markers, no tobacco relapse |

| 5+ years | Preferred plus (near never-smoked pricing) | Outstanding health profile, sustained cessation, carrier discretion |

The longer you stay quit, the closer your pricing moves to what someone who never smoked would pay. Carriers reward sustained cessation because the health risks tied to smoking drop significantly after several smoke-free years, bringing your mortality risk closer to that of a lifelong nonsmoker.

Policy Options for Smokers Seeking Affordable Life Insurance

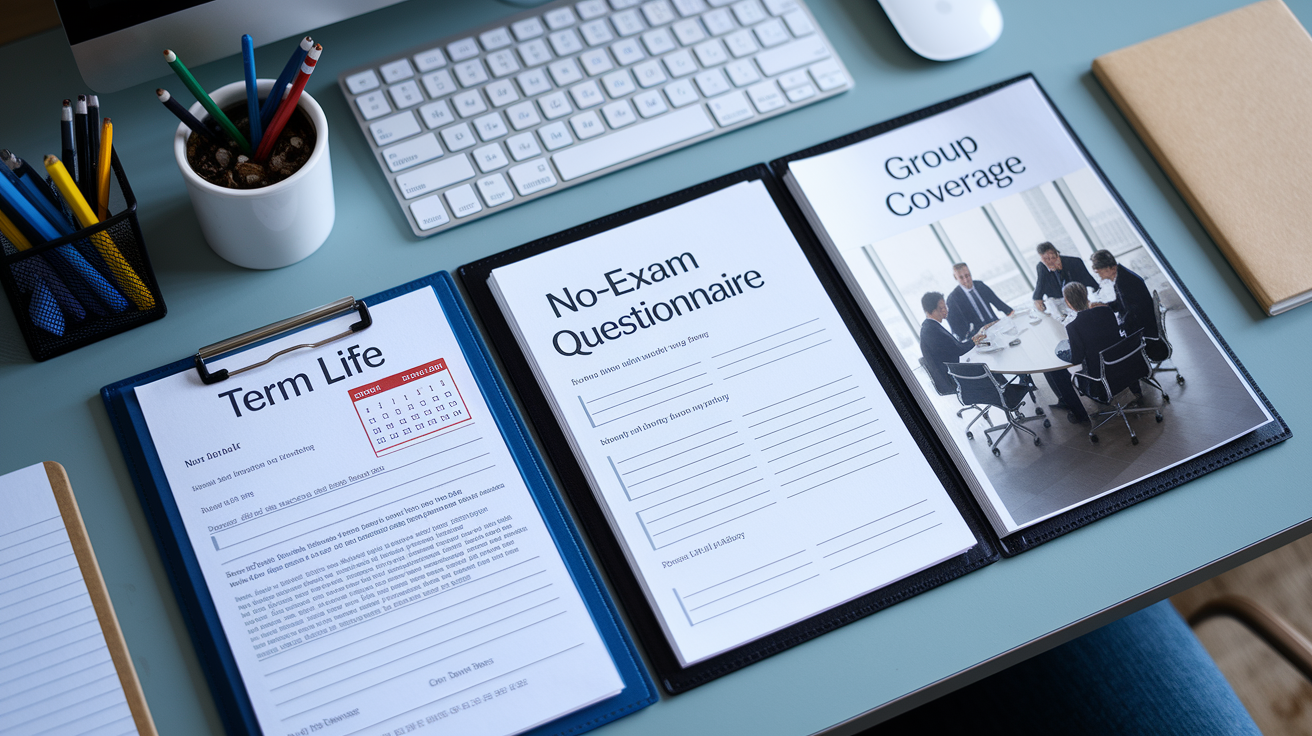

Term Life

Term life is usually the cheapest option for smokers who need solid coverage. Premiums are lower than whole or universal life because the policy only lasts for a set period (typically 10, 20, or 30 years) and pays out only if you die during that term. If you’re planning to quit, term works well because many carriers let you request a rate reclassification after 12 months tobacco-free without buying a new policy. That re-entry option lets you lock in lower premiums on the same contract once you pass a clean exam.

No-Exam Options

Simplified-issue policies skip the medical exam and rely on a health questionnaire plus a review of your medical records. You’ll still answer questions about tobacco, and your smoking status affects your premium, but approval is faster and there’s no paramedical visit. Guaranteed-issue policies go further by requiring no health questions and no exam at all. Coverage amounts are small (often capped at $25,000 or less) and premiums are high relative to the benefit. These also come with a graded death benefit, meaning full coverage doesn’t kick in until you’ve held the policy for two or three years. Guaranteed issue makes sense for smokers who can’t qualify for other coverage due to serious health conditions, but it’s an expensive last resort.

Group Coverage

Employer-sponsored group life typically provides coverage equal to one or two times your annual salary without individual underwriting for the base amount. That means your smoking status won’t raise your premium or disqualify you from baseline coverage. If you want to buy supplemental coverage beyond the base policy, you’ll usually answer health questions and may face higher rates as a smoker. Group life is portable only if your employer allows conversion, and coverage often ends when you leave the job, so it’s not a substitute for an individual policy you control.

Real-World Case Studies on Smoker vs. Non-Smoker Outcomes

A 35-year-old smoker bought a 20-year term policy with $500,000 in coverage and paid smoker rates for two years. After quitting completely, she contacted her insurer 14 months later and requested a rate reclassification. The insurer scheduled a new paramedical exam. Her cotinine test came back clean. Her annual premium dropped from roughly $1,400 to $500, saving her $900 every year for the remaining 18 years of the term. That one decision to quit and follow up saved her more than $16,000 over the life of the policy.

A 42-year-old male smoker compared three policy types when shopping. A $250,000 whole life policy quoted at $320 per month felt out of reach, so he looked at term life and landed a 20-year term with the same coverage for $140 per month as a smoker. He also checked out guaranteed-issue whole life, which offered only $15,000 in coverage for $85 per month and included a two-year waiting period before full benefits kicked in. He chose the term policy because it gave him real protection at a price he could sustain. He planned to request a rate review if he quit smoking within the first few years.

A 50-year-old nonsmoker and a 50-year-old smoker both applied for $500,000 in 20-year term coverage on the same day. The nonsmoker got a preferred rate of $1,200 per year. The smoker was quoted $4,800 annually, a $3,600 annual difference. Over 20 years, the smoker would pay $72,000 more for identical coverage. At age 50, the pricing gap is so wide that even modest health issues in a nonsmoker’s profile still leave them paying far less than a smoker in excellent health. Age amplifies the cost of smoking because older applicants already face higher base premiums, and the smoker multiplier applies on top of that elevated starting point.

Tips to Reduce Life Insurance Costs as a Smoker

If you smoke and need life insurance, a few practical moves can lower your premium or set you up for savings later. Start by comparing quotes from multiple carriers, because underwriting standards for tobacco users vary. Some insurers are gentler with occasional cigar smokers or people using nicotine replacement therapy. Others apply strict pricing across the board. Working with an independent agent who knows which carriers treat smokers better can save you time and money.

Most effective strategies:

- Apply sooner, not later. Premiums rise with age, so waiting a year can cost you more than the savings from quitting first.

- Choose term over whole life. Term policies cost less and give you flexibility to reclassify to nonsmoker rates after you quit.

- Look for carriers that allow rate reconsideration. Policies with re-entry provisions let you request lower premiums on the same contract once you’ve been smoke-free for 12 months.

- Avoid smoking or using nicotine right before your medical exam. Nicotine temporarily raises blood pressure, which can affect your underwriting result beyond just your smoker classification.

- Quit smoking and request reclassification after 12 months tobacco-free. Expect to take a new medical exam with cotinine testing, but the premium drop is usually worth it.

- Consider group life through your employer. Base coverage often doesn’t require underwriting, so your smoking status won’t affect eligibility or cost for that portion.

- Don’t delay buying coverage just to wait until you quit. New health issues or another year of age can offset any savings from quitting, and having some coverage now protects your family immediately.

Quitting tobacco is the biggest step you can take to reduce life insurance costs over time. Once you’ve been smoke-free for a year, reach out to your insurer or agent to start the reclassification process. Most carriers require proof through a new exam, but the premium reduction often exceeds $1,000 per year, making it one of the highest-return financial decisions you can make after kicking the habit.

Final Words

You saw the hard numbers: smokers often pay three to four times what non-smokers pay for the same coverage, with clear examples by age and coverage amount.

We explained how insurers define smoking, how testing and rate classes work, the quit timelines, and practical policy choices to manage cost.

Use those facts to compare quotes and plan. Life insurance cost for smokers vs non smokers can change if you quit or pick a different policy, so there’s a clear path to lower premiums and protect your family.

FAQ

Is life insurance more affordable for nonsmokers than smokers?

Life insurance is significantly more affordable for nonsmokers than smokers. Nonsmokers typically pay three to four times less in premiums because insurers classify tobacco use as a major health risk that shortens life expectancy and increases mortality rates.

How much higher are life insurance premiums for smokers compared to nonsmokers?

Life insurance premiums for smokers are typically three to four times higher than premiums for nonsmokers. For example, a 40-year-old male nonsmoker might pay around $450 annually for a $500,000 term policy, while a smoker of the same age would pay approximately $2,000 annually for identical coverage.

How much does a $1,000,000 life insurance policy cost per month for smokers and nonsmokers?

A $1,000,000 life insurance policy costs smokers significantly more than nonsmokers each month. While exact rates depend on age, health, and policy type, smokers can expect to pay roughly three to four times the monthly premium a nonsmoker would pay for the same coverage amount and term length.

How long after quitting smoking can you qualify for lower life insurance rates?

You can qualify for lower life insurance rates after being tobacco-free for 12 months with most insurers. Some carriers require 24 months of cessation, and reaching preferred pricing often requires three to five years smoke-free plus a new medical exam to confirm your tobacco-free status.

What products trigger a smoker classification for life insurance?

A smoker classification for life insurance is triggered by using cigarettes, cigars, pipes, vaping devices, e-cigarettes, nicotine gum, nicotine patches, nicotine lozenges, hookah, or chewing tobacco within the past 12 months. Some insurers also classify marijuana smoking as tobacco use.

Do insurers test for nicotine during the life insurance application process?

Insurers test for nicotine during the life insurance application process through blood and urine samples collected during the medical exam. These tests detect cotinine, a nicotine metabolite that remains in your system for days to weeks depending on usage frequency, confirming recent tobacco use.

Can smokers get life insurance without a medical exam?

Smokers can get life insurance without a medical exam through simplified issue or guaranteed issue policies. However, these no-exam options typically cost more and offer lower coverage limits compared to traditional policies that require underwriting and a medical exam.

Does quitting smoking guarantee a lower rate on an existing life insurance policy?

Quitting smoking does not automatically lower rates on an existing life insurance policy. You must remain tobacco-free for 12 to 24 months, then request rate reconsideration from your insurer, which typically requires submitting to a new medical exam to verify your nonsmoker status.

Why do life insurance companies charge smokers higher premiums?

Life insurance companies charge smokers higher premiums because tobacco use dramatically increases mortality risk through cancer, heart disease, lung disease, and other conditions. Smokers have shorter life expectancies on average, which means insurers are more likely to pay death benefits sooner.

Can occasional cigar smokers qualify for nonsmoker life insurance rates?

Occasional cigar smokers may qualify for nonsmoker life insurance rates if they smoke 24 or fewer cigars per year, depending on the carrier. Insurers vary in how they classify occasional tobacco use, so disclosing your exact usage pattern during underwriting helps determine your eligibility.