{kind=link}

Think all Medicare drug plans are the same?

Think again.

Your choice can change what you pay at the pharmacy by hundreds or thousands.

This post shows the key parts of Medicare Part D, how formularies, drug tiers, pharmacy networks, utilization rules, and enrollment windows affect your costs, which mistakes raise your bill, and what to check so your prescriptions stay affordable and you avoid surprise charges or late enrollment penalties.

Understanding Medicare Part D Prescription Drug Plans

Medicare Part D is optional prescription drug coverage sold by private, Medicare-approved insurance companies to people enrolled in Medicare. It helps pay for the medications you pick up at the pharmacy, whether brand name or generic, and can seriously lower your yearly drug costs. You can get Part D either as a stand-alone Prescription Drug Plan (PDP) alongside Original Medicare, or as part of a Medicare Advantage plan that bundles medical and drug coverage into one plan. Without Part D or other creditable drug coverage, you’ll face a late enrollment penalty that bumps up your monthly premium for as long as you have Medicare.

Not everyone needs Part D right away. If you have employer or union retiree drug coverage, VA benefits, or TRICARE, that may count as creditable coverage and let you delay enrollment without penalty. But if you take regular prescriptions, especially for chronic conditions like diabetes, high blood pressure, or heart disease, Part D can make a big difference between affordable monthly copays and paying full retail prices at the pharmacy. Even if you don’t take many drugs today, enrolling during your first chance helps you dodge the permanent late penalty down the road.

Part D plans aren’t all the same. Each insurer builds its own formulary (the official list of covered drugs), sets its own monthly premium, and decides which pharmacies join the network and which drugs require prior approval before the plan will pay. That’s why the cheapest plan for your neighbor might cost you hundreds more per year if your medications land on expensive tiers or aren’t covered at all.

Here are the key features that vary from plan to plan:

Formulary coverage. Every plan covers different drugs and brands. Your specific medication might be excluded or placed on a high cost tier.

Drug tiers. Plans sort drugs into tiers (typically generic, preferred brand, non-preferred brand, specialty). Higher tiers mean higher copays.

Pharmacy networks. Using an out of network pharmacy can double or triple your copay, and mail order options often reduce costs for maintenance drugs.

Utilization management. Plans may require prior authorization, step therapy (trying a cheaper drug first), or quantity limits before approving coverage.

Annual changes. Formularies, premiums, networks, and covered drugs can all change on January 1, so you need to review your plan every fall during the Annual Open Enrollment Period (October 15 through December 7).

Medicare Part D Plan Types and How They Work

There are two ways to get Medicare drug coverage: a stand-alone Prescription Drug Plan (PDP) or a Medicare Advantage plan that includes drug benefits (MA-PD). PDPs pair with Original Medicare (Parts A and B) and cover only your prescriptions. You still use Original Medicare for doctor visits, hospital stays, and other medical care. Medicare Advantage plans with drug coverage bundle everything (hospital, doctor, and prescription benefits) into one plan run by a private insurer, and you must stay in the plan’s network for both medical and pharmacy services.

Both plan types use formularies and drug tiers to control costs and access. A formulary is the plan’s official drug list, organized into tiers that determine what you pay out of pocket. Tier 1 usually holds preferred generics with the lowest copays, often $0 to $10. Tier 2 covers non-preferred generics or preferred brands, tier 3 holds non-preferred brands, and tiers 4 or 5 are reserved for specialty medications (biologics, injectables, high cost drugs) that may require coinsurance of 25% or more instead of a flat copay. Plans also enforce rules like prior authorization (you or your doctor must get approval before the plan pays) and step therapy (you must try a cheaper drug first and show it didn’t work). If your medication isn’t on the formulary at all, you’ll pay full price unless you successfully appeal for an exception.

| Plan Type | What It Includes | Who It Suits | Key Limitations |

|---|---|---|---|

| Prescription Drug Plan (PDP) | Prescription coverage only; pairs with Original Medicare Parts A & B | People who want to keep Original Medicare and choose their own doctors nationwide | Does not include medical coverage; you’ll need separate Medigap if you want supplemental insurance |

| Medicare Advantage with Drug Coverage (MA-PD) | Medical (Parts A & B) and prescription coverage in one plan | People who prefer a single plan with network doctors, lower premiums, and bundled benefits | Must use plan’s network for medical and pharmacy; switching drug coverage means changing your entire medical plan |

Medicare Part D Coverage Stages and Cost Structure

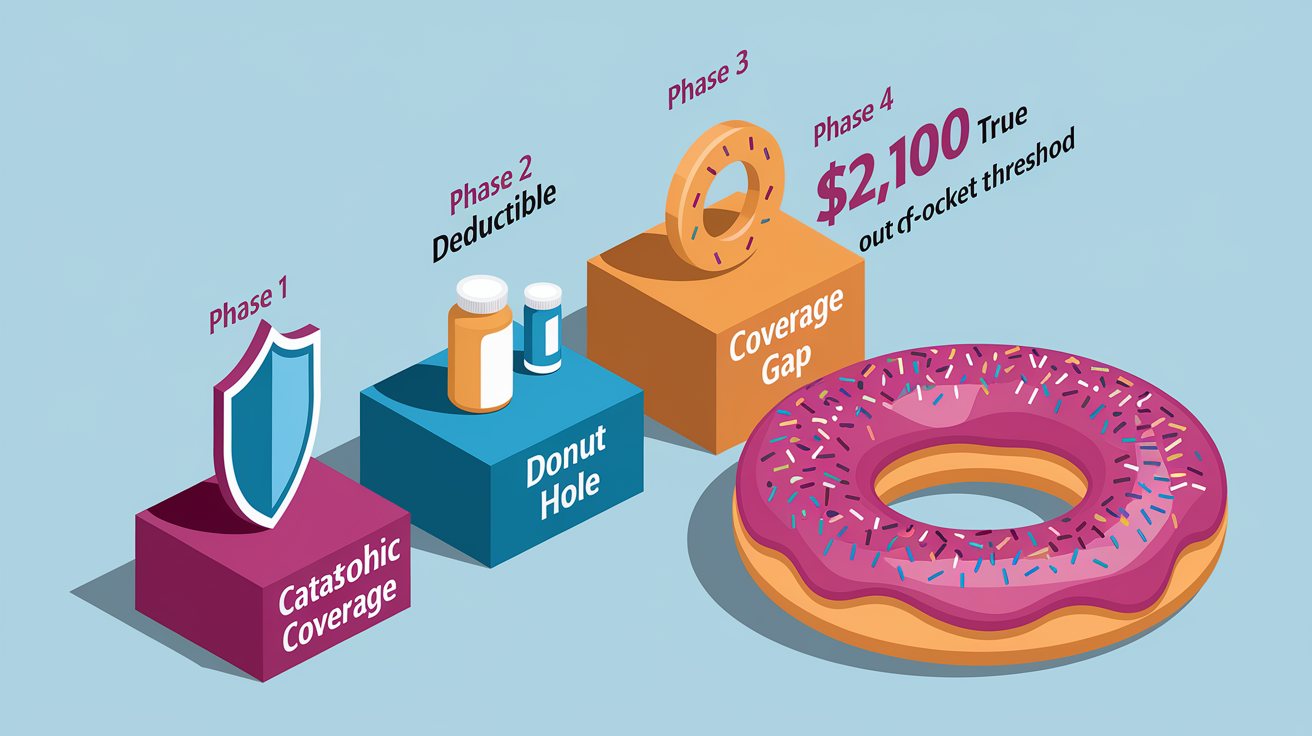

Every Medicare Part D plan follows the same four phase spending cycle each calendar year: the deductible phase, the initial coverage phase, the coverage gap (donut hole), and catastrophic coverage. Understanding these phases helps you predict when your out of pocket costs will spike or drop and plan your yearly drug budget.

Phase 1: Deductible. Some plans start with a $0 deductible, meaning you pay only copays from your first prescription. Other plans require you to pay the full cost of your drugs until you’ve spent up to the plan’s deductible (in 2026, the maximum deductible a plan can charge is $615). Once you hit the deductible, you move into the initial coverage phase.

Phase 2: Initial Coverage. After the deductible, you pay the plan’s standard copays or coinsurance for each prescription (amounts vary by tier and pharmacy). Your plan pays its share, and you stay in this phase until the total drug costs (what you paid plus what the plan paid) reach the initial coverage limit set by Medicare each year. This is the phase where most people spend the majority of the year if they take a few maintenance medications.

Phase 3: Coverage Gap (Donut Hole). Once you cross the initial coverage limit, you enter the gap. In the gap, you pay a higher percentage of the drug cost, typically around 25% for both brand name and generic drugs. Manufacturer discounts count toward closing the gap, so even though you’re paying more, you’re also moving faster toward catastrophic coverage. The gap ends when your true out of pocket costs (your payments, not the plan’s) hit the catastrophic threshold. In 2026, that threshold is $2,100. Once you’ve personally spent $2,100 on covered drugs, you exit the gap.

Phase 4: Catastrophic Coverage. After you reach $2,100 in out of pocket spending in 2026, you pay nothing for the rest of the calendar year on covered drugs. This is the safety net that protects people with very high drug costs (cancer patients, people on expensive specialty medications, or anyone taking multiple brand name drugs). On January 1, the cycle resets and you start back at the deductible phase.

Here’s how you move through the phases in order:

- Pay full cost (or copays if $0 deductible) until you meet the plan’s deductible.

- Pay standard copays or coinsurance during initial coverage until total drug spending hits the initial coverage limit.

- Pay higher cost sharing in the coverage gap until your personal out of pocket reaches $2,100.

- Pay $0 copays for covered drugs for the rest of the calendar year once catastrophic coverage begins.

Medicare Part D Enrollment Windows, Deadlines, and Penalties

You can’t enroll in Medicare Part D anytime you want. There are specific windows when you’re allowed to join, switch, or drop a plan, and missing those windows can lock you out until the next opportunity or trigger a permanent penalty that raises your monthly premium.

Your Initial Enrollment Period (IEP) is a seven month window that starts three months before the month you turn 65, includes your birthday month, and runs three months after. If you’re already on Medicare due to disability before age 65, your IEP is tied to your disability start date. During this window, you can enroll in a Part D plan without penalty. If you skip Part D and don’t have other creditable drug coverage (employer plan, VA, TRICARE), the penalty clock starts ticking after your IEP ends.

The Annual Open Enrollment Period runs every year from October 15 through December 7. During this time, anyone with Medicare can join a Part D plan for the first time, switch from one plan to another, drop Part D coverage, or move between a stand-alone PDP and a Medicare Advantage plan with drug coverage. Changes you make during this period take effect January 1. This is also when you should review your current plan’s upcoming formulary and premium changes. Most plans send an “Annual Notice of Change” in late September explaining what’s different for the new year.

Special Enrollment Periods (SEPs) let you enroll or change plans outside the usual windows if you experience a qualifying life event. Common SEPs include:

Moving out of your plan’s service area (for example, relocating to a different state or county where your current plan isn’t offered).

Losing employer or union drug coverage that was creditable.

Becoming eligible for Medicaid or Extra Help (the Low Income Subsidy).

Moving into or out of a nursing home or long term care facility.

Involuntary loss of coverage (your plan exits the market or loses its Medicare contract).

The late enrollment penalty applies if you go 63 continuous days or longer without Medicare drug coverage or other creditable coverage after your Initial Enrollment Period ends. The penalty is calculated as 1% of the national base beneficiary premium (set each year by Medicare) multiplied by the number of full, uncovered months you went without coverage. That amount is added to your monthly Part D premium for as long as you have Part D. For example, if you delay enrollment by 24 months, you’ll pay an extra 24% of the base premium every month, possibly for decades. The only way to avoid the penalty is to enroll on time or maintain creditable coverage without a gap longer than 63 days.

Medicare Part D Costs Explained (Premiums, Deductibles, Copays)

Medicare Part D cost sharing has several moving parts, and every plan structures them differently. Understanding each piece helps you estimate your total yearly spending and compare plans accurately.

Monthly premium. This is the amount you pay to stay enrolled in the plan, whether or not you fill any prescriptions. In 2026, the average premium for a stand-alone Part D plan is $34.50 per month, but actual premiums range from $0 to over $100 depending on the plan’s coverage, the insurer, and your location. If you’re enrolled in a Medicare Advantage plan with drug coverage, the drug premium is often bundled into the plan’s overall premium, and some MA-PD plans advertise $0 premium (though you still pay copays when you fill scripts).

IRMAA (Income-Related Monthly Adjustment Amount). Higher income beneficiaries pay an additional premium on top of the plan’s base premium. IRMAA kicks in if your modified adjusted gross income from two years ago exceeds certain thresholds (for 2026, it’s based on your 2024 tax return). The extra charge is added to your Part D premium and can range from roughly $12 to over $80 per month depending on your income bracket. Social Security automatically bills IRMAA separately from your plan premium.

Here are the six cost components you’ll encounter with any Part D plan:

Premium. The monthly plan charge. Varies by insurer and coverage level. IRMAA may add an income based surcharge.

Deductible. The amount you pay out of pocket before the plan starts sharing costs. Some plans have $0 deductible, others go up to the 2026 maximum of $615.

Copayments. Flat dollar amounts you pay per prescription (common for generic and preferred brand tiers). Example: $5 for tier 1, $47 for tier 3.

Coinsurance. A percentage of the drug cost you pay (common for specialty tiers). Example: 25% coinsurance on a $10,000 specialty drug means you pay $2,500.

Out of pocket cap. The maximum you pay in a year before catastrophic coverage starts. In 2026 that cap is $2,100 in true out of pocket costs.

Pharmacy network pricing. Using a preferred or in network pharmacy lowers your copay. Going out of network or skipping mail order can raise costs significantly, even for the same drug on the same plan.

Comparing Medicare Part D Plans the Right Way

Choosing a Part D plan based only on the monthly premium is one of the most expensive mistakes you can make. A $0 premium plan might sound appealing until you discover your heart medication sits on tier 4 with 40% coinsurance, pushing your yearly cost into the thousands. The right way to compare plans is to calculate your total annual cost (premiums plus all the out of pocket spending for your actual prescriptions) using the specific drugs and dosages you take today.

Start by making a complete list of every prescription you currently take. Write down the drug name (brand or generic), the exact dosage, and how often you refill it each year. If you take a 90 day supply by mail, note that instead of monthly refills. Gather this information from your pill bottles, your pharmacy’s print out, or your doctor’s records. If your medication list changes seasonally (for example, you only take allergy medication in spring), include those too. The more accurate your list, the more accurate your cost estimate will be.

Next, identify your preferred pharmacies. Some plans offer lower copays at certain chains (CVS, Walgreens, Walmart) or independent pharmacies in their “preferred network.” Mail order pharmacies often cut costs for maintenance drugs, especially if you order a 90 day supply instead of going to the counter every month. Knowing which pharmacy you’ll actually use lets the comparison tool show real world prices instead of hypothetical averages.

Step-by-Step Comparison Checklist

- List all your current medications with exact names, dosages, and quantities (example: Atorvastatin 20 mg, 30 tablets per month).

- Go to the official Medicare Plan Finder at Medicare.gov and enter your ZIP code. The tool will show all available Part D and Medicare Advantage plans in your area.

- Enter your drug list into the Plan Finder. The tool will look up each medication on every plan’s formulary and calculate your estimated yearly cost, including premiums, deductible, and copays.

- Add your preferred pharmacies to the search so the tool shows accurate pricing based on network agreements and mail order discounts.

- Review the plan’s formulary details for each of your drugs. Check the tier, any restrictions (prior authorization, quantity limits, step therapy), and whether the drug is covered at all.

- Compare total estimated annual costs across plans, not just the premium. The Plan Finder will rank plans by total cost and show a detailed breakdown month by month.

- Check for coverage gaps. If one of your drugs isn’t covered or requires an exception, factor in the appeal process or the cost of paying out of pocket. A plan that covers all your medications with no restrictions is almost always cheaper in the long run than fighting for exceptions.

Extra Help (LIS) and Other Cost Assistance for Medicare Part D

Extra Help (officially called the Low Income Subsidy or LIS) is a federal program that reduces or eliminates Part D premiums, deductibles, and copays for people with limited income and resources. It’s administered jointly by the Social Security Administration and the Centers for Medicare & Medicaid Services, and the average annual benefit is worth about $5,700 per person. If you qualify, you’ll pay little to nothing for most covered prescriptions, and you won’t face a late enrollment penalty even if you sign up outside the usual enrollment windows.

To qualify for Extra Help in 2026, your annual income generally must fall below roughly $22,000 for an individual or $30,000 for a married couple (exact thresholds adjust yearly and vary slightly by state). Your countable resources (bank accounts, stocks, bonds, but not your home or car) must stay below about $16,000 for individuals or $32,000 for couples. If you’re already on Medicaid, SSI, or certain state assistance programs, you automatically qualify for Extra Help and don’t need to apply separately. Dual eligible beneficiaries (people with both Medicare and Medicaid) receive the highest level of subsidy and can switch Part D plans once per quarter instead of waiting for Annual Open Enrollment.

Applying for Extra Help is free. You can apply online at the Social Security Administration’s website, call Social Security, or fill out a paper application available at your local SSA office or State Health Insurance Assistance Program (SHIP). The application asks about your income, assets, and household expenses. If approved, the subsidy starts the month after approval or retroactively if you were eligible earlier. Even if you’re not sure you’ll qualify, it’s worth applying. Approval unlocks significant savings and opens Special Enrollment Periods that let you change plans outside the normal windows.

If you need help applying or want to explore other programs that reduce prescription costs, here are the key documents to have ready:

Proof of income (Social Security statements, pay stubs, pension statements, or tax returns).

Asset statements (recent bank and investment account balances).

Your Medicare card and Social Security number.

Proof of address (utility bill, lease, or mortgage statement).

Appeals, Exceptions, and Resolving Medicare Part D Drug Coverage Issues

Sometimes your Part D plan will deny coverage for a prescription, either because the drug isn’t on the formulary, it requires prior authorization you haven’t completed, or the plan wants you to try a cheaper medication first under step therapy rules. When that happens, you don’t have to accept the decision. Medicare gives you the right to request a coverage determination (a formal decision from the plan) and, if denied, to appeal through multiple levels until you get a final answer.

A coverage determination is the plan’s official yes or no answer about whether it will cover a drug, cover it at a lower cost tier, waive a restriction, or approve an exception. You or your doctor can request a determination at any time, and the plan must respond within 72 hours for standard requests or 24 hours for expedited (urgent) requests if your health is at risk. If the plan says no, it must send you a written denial letter that explains the reason and your appeal rights.

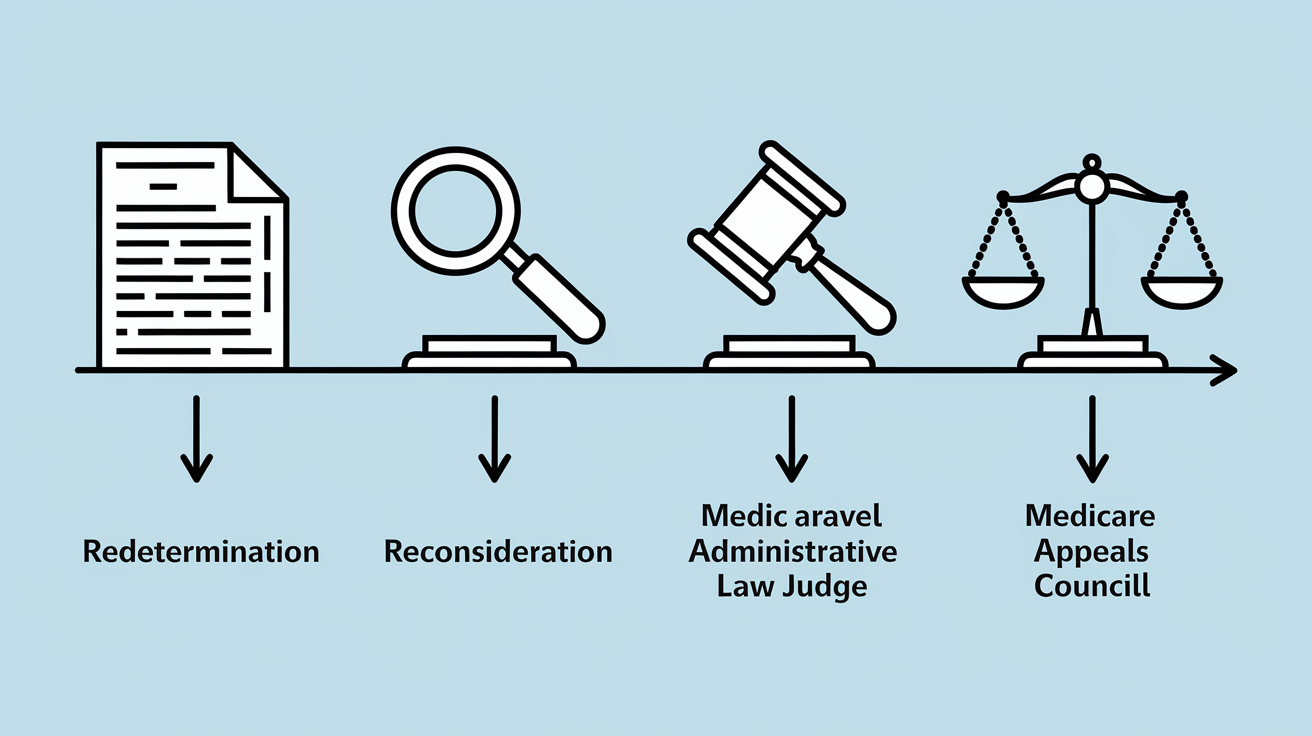

If you disagree with a denial, you move into the appeals process. The first level is called a redetermination. You ask the plan to review its decision again, and an independent reviewer within the plan looks at your case. If the plan denies you again, you can request a hearing with an independent review entity that has no connection to your insurer. From there, appeals can escalate to an administrative law judge, the Medicare Appeals Council, and even federal court, though most cases resolve at the first or second level. Deadlines matter: you usually have 60 days from the denial date to file the next level of appeal, and if your health is in danger, you can request an expedited review at any stage.

Here are the four main appeal stages in order:

- Redetermination. The plan reviews its own decision. You have 60 days to request this after a denial.

- Reconsideration. An independent review organization (IRO) outside your plan evaluates the case. File within 60 days of the redetermination denial.

- Administrative Law Judge (ALJ) hearing. A federal judge hears your case if the dollar amount in dispute meets the minimum threshold (adjusts yearly).

- Medicare Appeals Council and Federal Court. Final review stages for cases that remain unresolved. Rarely needed for typical coverage disputes.

Using Medicare Part D Benefits Day-to-Day

Once you’re enrolled in a Part D plan, getting your prescriptions filled is usually straightforward: show your plan’s member ID card at the pharmacy counter, and the pharmacist will bill the plan and charge you the copay on the spot. But a few day to day strategies can lower your costs and make refills more convenient, especially if you take multiple medications every month.

Mail order pharmacies are one of the easiest ways to save. Most Part D plans contract with a mail order service (often run by the same company that manages the plan’s pharmacy network) and offer a discount if you order a 90 day supply of a maintenance drug instead of picking up 30 days at a time from a retail pharmacy. For example, a drug that costs you $15 per month at the counter might cost $30 for a 90 day mail order (essentially one month free). Mail order works best for prescriptions that don’t change often, like blood pressure meds, cholesterol drugs, or diabetes medications. You’ll submit the prescription to the mail order pharmacy (your doctor can send it electronically or you can mail a paper script), and the pharmacy ships the medication to your home, usually within a week.

Synchronization programs (sometimes called “med sync”) align all your prescription refill dates to the same day each month so you can pick up everything in one trip instead of making multiple pharmacy visits. Many retail chains offer this service for free, and it reduces the chance you’ll run out of a critical medication because you forgot to refill. If your plan allows 90 day supplies at retail (some do, some only offer it by mail), combining synchronization with a 90 day fill cuts your pharmacy trips to once per quarter. You can also transfer a prescription from one pharmacy to another within your plan’s network without losing coverage. Just ask the new pharmacy to request the transfer, and they’ll contact your old pharmacy to move the prescription over. You’re not locked into one location as long as both pharmacies are in network.

Policy Changes and Future Updates Affecting Medicare Part D Plans

Medicare Part D rules, cost limits, and coverage structures change almost every year as Congress and CMS adjust the program to manage spending and improve access. Staying on top of these updates helps you anticipate premium increases, take advantage of new protections, and avoid surprises when you refill prescriptions in January.

For 2026, the key updates include an average stand-alone Part D premium of $34.50 per month, a maximum annual deductible of $615, and a new out of pocket catastrophic threshold of $2,100 (after which you pay nothing for covered drugs for the rest of the year). The $2,100 cap is a major change from prior years and reflects recent legislation designed to limit yearly spending for people with high drug costs. Once you hit that threshold, catastrophic coverage kicks in immediately with $0 copays, protecting you from the unpredictable costs that used to occur in the old coverage gap structure.

Looking ahead, additional policy shifts may affect how plans price their premiums and structure their formularies. Manufacturer rebates (payments that drug companies make to insurers in exchange for favorable formulary placement) are under ongoing review, and changes to how rebates are passed along to beneficiaries could raise or lower premiums depending on the final rules. Plans are also required to update their formularies each year, which means a drug covered this year might move to a higher tier, require new restrictions, or be dropped entirely next January. That’s why reviewing your plan every fall during Annual Open Enrollment isn’t optional if you want to avoid unexpected bills in the new year.

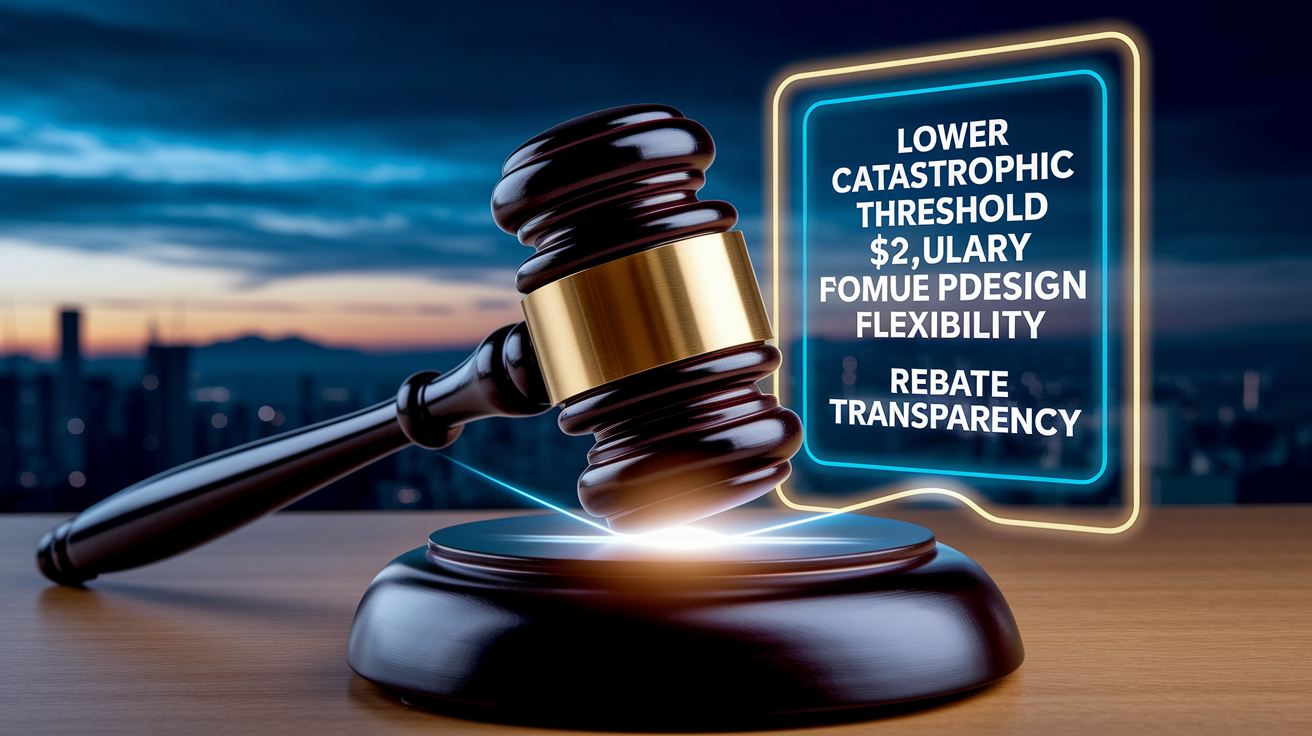

Here are the three most significant near term changes to watch:

Lower catastrophic threshold in 2026. The $2,100 out of pocket cap replaces the old higher threshold and eliminates cost sharing once you reach it, a substantial protection for people on specialty or high cost medications.

Formulary redesign flexibility. CMS allows plans to adjust tier structures and utilization management rules annually. Drugs can move between tiers or gain new prior authorization requirements without advance individual notice beyond the Annual Notice of Change.

Rebate transparency initiatives. Proposed rules may require plans to share more manufacturer rebate savings directly with beneficiaries at the pharmacy counter instead of using rebates only to lower overall premiums. Implementation timelines and final details are still evolving.

Final Words

You’ve seen how Medicare Part D works: what it covers, the two plan types, the four coverage stages, costs to expect, enrollment windows, and where to look for extra help.

Use the step-by-step checklist each year—list your meds, run the Plan Finder, compare total yearly costs, check formularies and pharmacy networks, and note prior authorizations.

Compare options carefully. Reviewing medicare part d plans yearly makes a real difference to out-of-pocket costs, and you can pick a plan that fits your needs with more confidence.

FAQ

Q: What is the best Medicare Part D plan?

A: The best Medicare Part D plan depends on your medications, pharmacy, and budget. Use Medicare’s Plan Finder to compare yearly costs, formularies, and network pharmacies before choosing.

Q: What is the monthly cost for Medicare Part D and how much will it cost in 2026?

A: The monthly cost for Medicare Part D varies by plan; the 2026 average PDP premium is $34.50, though your premium can be higher or lower and IRMAA may add charges.

Q: Does Medicare pay for pacemaker surgery?

A: Medicare pays for pacemaker surgery when medically necessary. Part A covers inpatient hospital costs; Part B covers physician services and outpatient insertion, both subject to deductibles and coinsurance.