{kind=link}

Did you know your homeowner’s policy may pay to replace storm or fire damage but not the upgrades your city makes you add to meet current building codes?

Ordinance or law coverage fills that gap.

It pays for three main things: demolition and debris removal required by code, increased cost of construction to meet new standards, and the value of undamaged parts you must tear out to comply.

This post shows what each covers, common permit-time surprises, and how limits can leave you with a big bill.

Core Protections Included in Ordinance or Law Coverage Explained

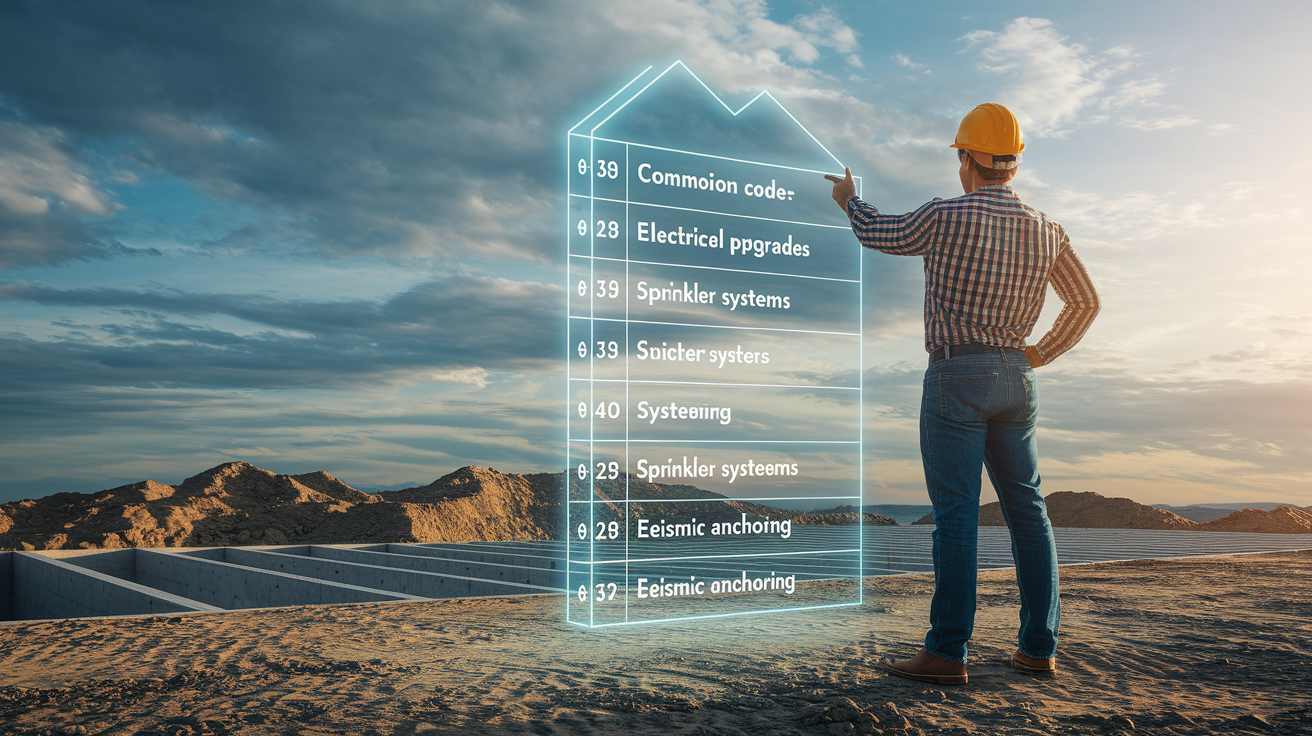

Ordinance or law coverage pays the expenses you need to bring your home into compliance with current local building codes after a covered loss. When fire, wind, or another covered event damages your building, local authorities often require repairs to meet today’s standards, not the codes that existed when your home was originally built. These upgrades can run from seismic reinforcements to electrical panel replacements to fire suppression systems. Without this endorsement, the standard homeowners policy only reimburses you to restore your home to its pre-loss condition, and the added code-driven costs land on your shoulders.

The coverage splits into three main components. First, demolition and debris removal pays to tear down and haul away sections of the building that local law requires removed, even if those sections were only partially damaged. Second, increased cost of construction covers the extra expense to rebuild using materials, methods, or systems that comply with current codes. Think replacing old knob and tube wiring throughout the house after a kitchen fire, or installing a new foundation anchor system required by seismic ordinances. Third, loss to undamaged portion reimburses the value of undamaged parts that must be removed or rebuilt solely to comply with code. For example, a wall that survived a fire might still need to be torn down if new framing rules require structural ties that can’t be retrofitted around existing walls.

Standard homeowners policies pay to replace damaged property “like for like,” returning your home to the condition it was in just before the loss. They don’t pay to bring the building up to a newer mandatory standard enacted after the original construction. That principle is called indemnity, compensating for actual loss without adding value, and it specifically excludes code-driven upgrades. Ordinance or law coverage fills that specific gap, acting as a separate endorsement or built-in clause with its own sublimit.

What gets covered:

Demolition and debris removal when codes require teardown of condemned or unsafe sections

Increased cost to rebuild plumbing, electrical, HVAC, or structural systems to current codes

Removal and replacement of undamaged portions if code requires their removal for compliance

Foundation tie-ins, seismic anchors, and shear wall installations mandated by updated building standards

Fire suppression systems, sprinklers, or emergency exits added per local ordinance

ADA compliant access improvements, elevator retrofits, or stair modifications required by code after a covered loss

How Building Code Upgrade Requirements Influence Ordinance or Law Coverage

Code upgrades often surface during permitting and inspection. The moment a contractor pulls a permit to repair a damaged room, the local building department reviews the entire home and flags systems that don’t meet current standards. In many jurisdictions, once you open a permit, you must bring the affected systems or the entire structure up to code. This can include electrical rewiring if knob and tube circuits are discovered, plumbing replacement if galvanized steel pipes are present, seismic reinforcement if foundation anchors are missing, and accessibility improvements if your home is multi-story and local rules require at least one accessible entrance or bathroom. These requirements can add 10% to 50% or more to the total rebuild cost. That extra expense is only covered if an ordinance or law endorsement is active on the policy.

Even small scale losses can trigger sweeping upgrades. A burst pipe that damages a bathroom may lead an inspector to require the entire home’s plumbing be replaced if it’s decades old. A fire in one room can prompt a mandate to install a full electrical panel upgrade if the existing panel doesn’t meet amperage or grounding standards. Without coverage, you fund those improvements out of pocket or choose not to complete the repairs at all, which can delay rebuilding and jeopardize occupancy permits.

Common code-driven upgrades that ordinance or law coverage pays for:

Electrical panel upgrades and whole house rewiring to meet current National Electrical Code standards

Plumbing replacement from galvanized steel or lead pipes to copper or PEX

Seismic or hurricane tie-downs, shear walls, and foundation anchor bolts

Fire suppression sprinkler systems and hardwired smoke detector networks

Demolition and Debris Removal Requirements Under Ordinance or Law Coverage

Municipalities set damage thresholds that trigger mandatory demolition, often expressed as a percentage of the building’s assessed value or structural integrity. If a covered loss damages more than 50% of the structure, many local ordinances require the entire building be torn down and rebuilt from the ground up, even if portions remain standing and habitable. Demolition and disposal can cost $12,000 for a small single story home and exceed $50,000 for larger two story structures or homes with complex foundations and attached garages. These costs aren’t covered under standard debris removal clauses, which typically pay only for removal of materials directly damaged by the covered peril.

Ordinance or law coverage steps in to pay for demolition mandated by code enforcement, including tearing down undamaged wings, removing load bearing walls that survived the loss, and hauling away materials that must be disposed of in compliance with environmental or safety regulations. In some areas, asbestos abatement or lead paint removal becomes part of the demolition scope, adding thousands to the bill. Without this endorsement, you either absorb the full cost or abandon the property if the expense exceeds available funds.

| Cost Type | Typical Range |

|---|---|

| Demolition labor and equipment | $8,000–$35,000 |

| Debris hauling and disposal fees | $3,000–$12,000 |

| Environmental abatement (asbestos, lead) | $5,000–$25,000 |

Increased Cost of Construction: The Largest Expense in Ordinance or Law Claims

Increased cost of construction typically represents the bulk of an ordinance or law claim, because it includes every line item where the contractor must use a better material, install a new system, or follow a more stringent method than the original home employed. A full electrical panel upgrade can run $6,000 to $20,000 depending on home size and complexity. Installing a residential fire sprinkler system averages $8,000 to $20,000 for a standard single family home. Seismic retrofits, foundation anchoring, cripple wall bracing, and shear panel installation commonly cost $20,000 to $100,000 depending on foundation type, number of stories, and local seismic requirements. Adding accessible features like ramps, wider doorways, or ADA compliant bathrooms can add another $10,000 to $40,000 to the rebuild budget.

These expenses stack up quickly. You might face a $150,000 structural repair from a covered fire and discover that code required upgrades push the true rebuild cost to $230,000. The difference, $80,000, is only covered if the policy includes ordinance or law coverage with a limit high enough to absorb it. Insurers typically offer limits expressed as a percentage of the dwelling coverage: 10%, 25%, 50%, or 100%. On a home insured for $400,000, a 25% ordinance limit provides $100,000 of additional coverage for these code driven increases. If the limit is only 10%, you get $40,000 and pay the remaining $40,000 out of pocket.

The most frequent high cost items include foundation tie-ins and anchoring (common in California and Pacific Northwest seismic zones), HVAC system replacement to meet current energy codes (especially when old gravity furnaces must be swapped for high efficiency units), and whole house electrical rewiring when inspectors flag knob and tube or aluminum wiring during the rebuild. Each of these upgrades can individually exceed the limits provided by a basic 10% ordinance endorsement, which is why older homes in code active jurisdictions often need 50% or 100% limits to avoid serious gaps.

Coverage for Undamaged Portions: When You Must Tear Down What Wasn’t Broken

One of the least intuitive aspects of building code enforcement is the requirement to remove or rebuild undamaged parts of a structure. In seismic and hurricane regions, local ordinances often mandate that if you repair one major component, say a shear wall damaged by fire, you must bring adjacent undamaged walls and framing into compliance at the same time. This can mean tearing down a perfectly intact wall, removing and replacing floor joists, or demolishing an undamaged chimney because it lacks the seismic ties required by current code. Demolition costs for these undamaged sections can range from $20,000 to $50,000 depending on the scope and accessibility of the work.

Without ordinance or law coverage, the insurer pays only for the loss to damaged portions. If the building department requires the removal of undamaged framing or roofing to complete code compliant repairs, that cost falls entirely on you. This scenario is common in older homes where isolated damage triggers a cascade of mandatory upgrades. A water leak damages one bathroom, but the inspector requires the entire second floor’s plumbing be replaced because the pipes are galvanized steel. The bathroom pipe is covered. The rest of the floor’s plumbing is not, unless the ordinance endorsement applies.

Why Standard Homeowners Insurance Excludes Code-Driven Costs

Standard homeowners policies operate on an indemnity principle. They compensate you for the loss you actually suffered, restoring property to its pre-loss condition without adding new value. If your home was built in 1950 with knob and tube wiring and a fire damages the kitchen, the insurer pays to replace the kitchen wiring with the same type and capacity that existed before the fire. Upgrading that wiring to modern Romex with GFCI outlets and a 200-amp panel is considered an improvement, not indemnity, and is therefore excluded. The same logic applies to foundation anchors, seismic shear walls, sprinkler systems, and accessibility ramps. They represent a higher standard than what existed, so the base policy won’t pay for them.

This exclusion exists in nearly every standard homeowners policy form. Insurers don’t want to pay for mandatory community improvements or citywide retrofit programs that aren’t directly caused by the covered peril. The result is a coverage gap: you suffer a covered loss, you file a legitimate claim, and the insurer pays the pre-loss value, but the building department requires code upgrades that can double the repair bill. Ordinance or law coverage closes that gap by explicitly covering costs required to comply with laws or ordinances in effect at the time of loss.

Common exclusions that remain even with ordinance or law coverage:

Pre-existing code violations that existed before the loss and weren’t triggered by the damage

Zoning changes that increase lot coverage limits, require setbacks, or restrict building footprint

Voluntary upgrades or aesthetic improvements unrelated to code compliance

How Ordinance or Law Coverage Limits and Sublimits Work

Most insurers offer ordinance or law coverage as a percentage of the dwelling coverage limit. Common options are 10%, 25%, 50%, or 100% of Coverage A (the dwelling limit). If your home is insured for $300,000 and you select a 25% ordinance limit, you have $75,000 available for code driven costs. Some policies break that limit into three separate sublimits, Coverage A for loss to undamaged portions, Coverage B for demolition and debris removal, and Coverage C for increased cost of construction, while others pool the entire limit and let you use it across all three categories as needed. Check your policy declarations to see which structure applies.

A separate ordinance or law deductible may also apply. Some insurers use a deductible expressed as a percentage of the dwelling limit, commonly 5% or 10%. On a $300,000 dwelling limit, a 5% deductible means you pay the first $15,000 of ordinance driven costs before coverage kicks in. Other policies apply the standard homeowners deductible (often $1,000 to $5,000) to ordinance claims, and a few apply no separate deductible at all. Confirm this detail with your agent, because a high percentage deductible can significantly reduce the effective coverage in smaller claims.

| Limit Type | Typical Amount | What It Applies To |

|---|---|---|

| Percentage of dwelling coverage | 10%, 25%, 50%, 100% of Coverage A | All ordinance-driven costs combined or split among A/B/C sublimits |

| Separate dollar limit | $50,000, $100,000, $250,000 | Fixed amount available regardless of dwelling coverage changes |

| Deductible (percentage) | 5%–10% of dwelling coverage | Amount you pay before ordinance coverage begins |

| Deductible (flat) | Standard homeowners deductible ($1,000–$5,000) | Applied to ordinance claims same as other covered losses |

Cost of Ordinance or Law Coverage and Premium Impact Factors

Adding ordinance or law coverage typically increases your annual homeowners premium by roughly $100 to $500 for low to moderate risk properties, though the cost can climb substantially higher in areas with frequent code updates, high seismic or wind exposure, or historic district restrictions. Insurers price the endorsement based on home age, construction type, location, and the chosen limit. An older home with knob and tube wiring in a seismic zone will carry a higher premium than a recently built home in a low risk area, because the likelihood and cost of code triggered upgrades are much greater.

Underwriting factors include whether the home has been updated within the last decade, proximity to coastlines or fault lines, local building department enforcement patterns, and whether the property is in a historic preservation district where retrofit requirements are especially stringent. Some insurers offer tiered pricing. Choosing a 10% limit might add 3% to 5% to your premium, while selecting a 100% limit could add 10% to 15%. In absolute dollar terms, if your base homeowners premium is $2,000 per year, a 50% ordinance limit might cost an extra $150 to $300 annually.

The cost benefit calculation is straightforward for older homes. Paying a few hundred dollars per year to avoid a potential $40,000 to $80,000 out of pocket expense makes financial sense, especially when code upgrades are almost certain to be required after any significant loss. For newer homes in low code change areas, the endorsement may feel optional, but even recent construction can trigger retrofit requirements if local ordinances change between the build date and the loss date.

Real-World Claim Scenarios Showing Coverage Gaps Without Ordinance or Law Protection

A homeowner in a 1920s bungalow experiences a kitchen fire that causes $120,000 in structural damage. The local building department requires seismic anchoring, shear wall installation, and a new electrical panel before issuing a certificate of occupancy. The contractor estimates $60,000 for these code driven upgrades. The homeowner’s policy has a $400,000 dwelling limit but no ordinance or law coverage. The insurer pays $120,000 for fire damage and stops. The homeowner must either pay $60,000 out of pocket or leave the home unfinished and unoccupied. With a 25% ordinance endorsement ($100,000 limit), the code upgrades would be fully covered and the rebuild could proceed.

A two story home built in 1975 suffers wind damage that requires replacement of the roof and one exterior wall. During permitting, the inspector flags the entire house for knob and tube wiring removal, outdated plumbing, and the absence of foundation anchor bolts. Demolition of undamaged framing to install shear panels costs $22,000. Electrical rewiring costs $18,000. Plumbing replacement costs $14,000. Foundation anchoring costs $28,000. Total code driven expenses: $82,000. The homeowner’s policy includes only a 10% ordinance limit on a $250,000 dwelling coverage, providing $25,000. The homeowner pays the remaining $57,000 or delays the rebuild while seeking financing.

A multi-unit building sustains a partial loss from a burst pipe, damaging two units and common hallways. The city requires ADA compliant accessible entries, upgraded fire suppression systems, and stair modifications before re-occupancy permits are issued. The condo association faces a $95,000 bill for these compliance improvements. The master policy has no ordinance or law coverage. The association levies a special assessment on all unit owners to cover the shortfall, and owners without personal ordinance coverage on their HO-6 policies must pay their share of the assessment from savings. Had the master policy included a 50% ordinance endorsement, the compliance costs would have been covered under the association’s claim.

Filing an Ordinance or Law Coverage Claim and Required Documentation

When filing an ordinance or law claim, the insurer will ask for detailed documentation showing that the additional costs are required by law, not optional upgrades or contractor suggestions. Start by obtaining a written statement or formal notice from the local building department listing the specific code sections and ordinances that apply to your repair. This might be an inspection report, a permit condition sheet, or a formal compliance order. Without official documentation, the insurer may deny the ordinance portion of the claim or reclassify those costs as voluntary improvements.

Next, ask your contractor to prepare separate line item estimates, one for the basic repair to pre-loss condition and one for the code driven upgrades. The insurer needs to see the cost difference clearly. Include permit receipts, inspection fees, and any engineering or architectural reports required by the building department to demonstrate compliance. If demolition of undamaged portions is required, obtain a letter from the inspector or contractor explaining why code mandates removal and what ordinance applies. Keep copies of all correspondence with the building department, contractor bids, and any legal notices or citations issued during the repair process.

Key documents to gather for your ordinance or law claim:

Building department inspection report or code compliance order listing specific code sections and required upgrades

Contractor estimates with separate line items for pre-loss repair vs. code driven work

Permit applications and receipts showing fees paid for demolition, construction, and inspection

Engineering or architectural reports if seismic, structural, or accessibility modifications are required

Copies of applicable local ordinances or building code excerpts cited by the inspector or contractor

Who Needs Ordinance or Law Coverage the Most?

Older homes face the highest exposure because decades of code evolution mean the gap between original construction standards and current requirements is wide. If your home was built before 1980, it likely predates modern electrical codes, energy efficiency standards, seismic retrofitting rules, and fire suppression requirements. Even homes built in the 1990s can trigger significant upgrades if local jurisdictions adopted stricter codes in the 2000s or 2010s. Multiunit buildings, condominiums, and rental properties also carry elevated risk because code enforcement is often more aggressive when public safety or tenant occupancy is involved, and small losses can trigger building wide compliance mandates.

Properties in seismic zones, coastal hurricane regions, and areas with active wildfire urban interface codes should strongly consider at least a 50% ordinance limit. Many risk managers recommend 100% of dwelling coverage for homes in these high code change jurisdictions. Landlords and condo associations face additional exposure because loss of rental income or special assessments can compound the financial impact of an under insured ordinance claim. If your building department has a reputation for strict enforcement or if recent local disasters have prompted sweeping new retrofit ordinances, ordinance or law coverage is nearly essential.

High risk factors that increase the need for ordinance or law coverage:

Home built before 1980 with original plumbing, wiring, or HVAC systems still in place

Location in seismic zone, coastal wind zone, or wildfire interface area with active retrofit programs

Multiunit building, condominium, or rental property where code applies to common areas and multiple units

Historic home or landmark property subject to preservation board rules and additional compliance requirements

Final Words

When a covered loss leads to city orders, this coverage steps in for the expensive extras—demolition and debris removal, rebuilding to current codes, and tearing out undamaged parts when required.

The post walked through those three protections, how building codes raise costs, typical limits and sublimits, filing tips, and who’s most exposed.

If you’re asking what does ordinance or law coverage cover, it pays for the code-driven costs standard policies leave out. Check your limits, talk to your agent, and you’ll be ready if codes change after a loss.

FAQ

Q: Should I get ordinance or law coverage?

A: Ordinance or law coverage is worth buying if your property faces code-change risk—older homes, historic districts, or high-hazard areas—because it pays required upgrades, demolition, and debris costs that standard policies don’t cover.

Q: What is an example of an ordinance or law coverage claim?

A: An example of an ordinance or law coverage claim is a post-fire rebuild where the insurer must pay $40,000 for rewiring, sprinkler installation, and structural tie-ins to meet current building codes.

Q: What is Florida ordinance or law coverage and how much ordinance and law coverage should I have in Florida?

A: Florida ordinance or law coverage is an endorsement that pays code-driven rebuild costs in Florida; typical limits run 10%–100% of dwelling value, and many homeowners choose 25%–50% for higher-risk or older properties.