{kind=link}

Your starter property policy might not cover everything you assume it does—so what does it actually cover for first-time buyers?

This guide breaks down the essentials: dwelling, personal property, liability, loss of use, and the common perils most starter plans include.

You’ll also learn the big exclusions—like flood and earthquake—how limits and deductibles affect payouts, and which endorsements are worth adding to avoid surprise bills.

Short, clear examples and check-this tips will help you pick the right protection without getting overwhelmed.

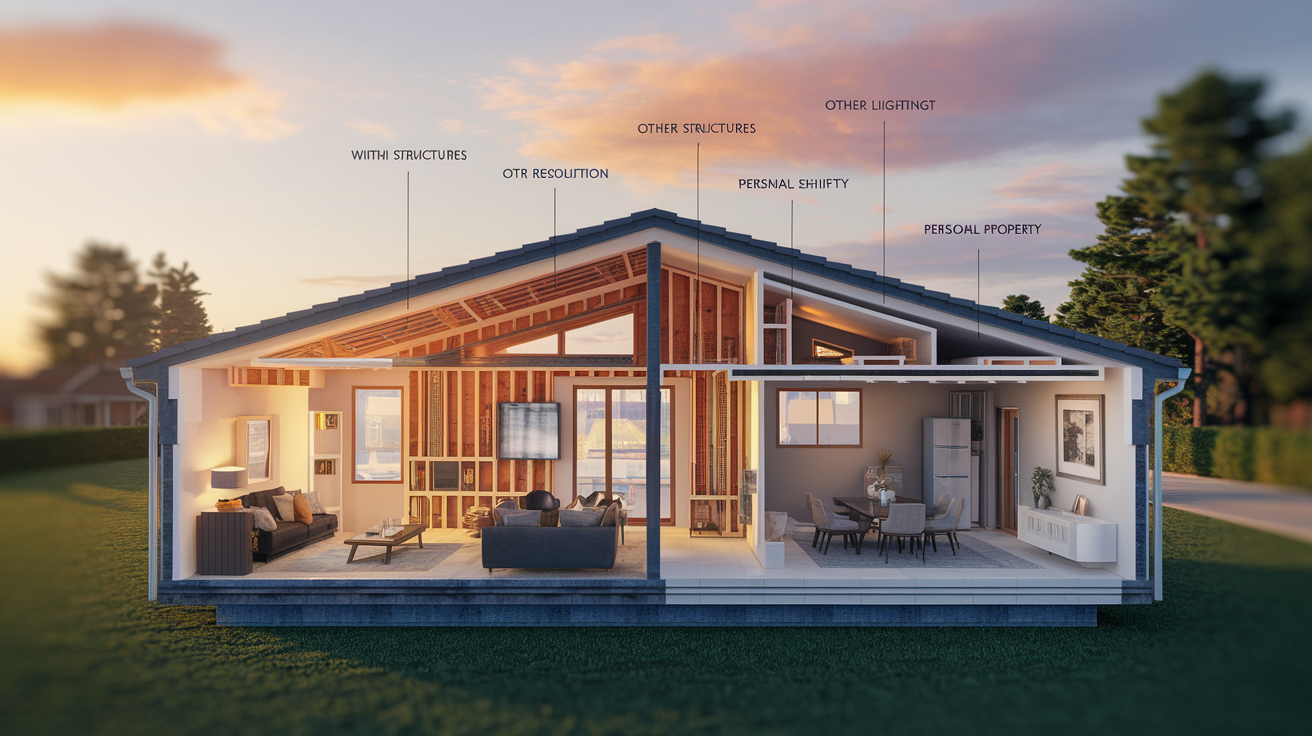

Core Coverages Included in Starter Property Insurance Policies

Starter property insurance works a lot like standard homeowners coverage, just scaled down for first-time buyers or homes with modest values. Dwelling coverage sits at the center. It pays to repair or rebuild your home’s structure after damage from a covered event. Walls, roof, floors, built-in appliances. You’re insuring reconstruction cost, not market value. That’s a key difference. A home worth $250,000 in a hot market might only need $180,000 in dwelling coverage if that’s what it costs to rebuild from the ground up.

Personal property coverage protects what’s inside. Furniture, electronics, clothing, kitchen gear. Most starter policies set this at around 50% to 70% of your dwelling limit. So $180,000 in dwelling coverage gets you somewhere between $90,000 and $126,000 for your stuff. High-value items get tricky though. Jewelry, fine art, collectibles usually have low sublimits, often $1,000 to $2,500. That stolen engagement ring worth $5,000? You might only see $1,500 unless you add a rider.

Liability protection steps in when someone gets hurt on your property or you accidentally damage someone else’s stuff. Guest slips on your icy front step and sues for medical bills and lost wages? That’s where liability coverage does its job. Medical payments coverage tags along and pays small medical bills right away, typically $1,000 to $5,000 per incident, regardless of whose fault it was. Can keep minor injuries from turning into lawsuits. Loss of Use (sometimes called Additional Living Expenses) reimburses you for hotel stays, restaurant meals, and other extra costs when your home becomes unlivable. Kitchen fire forces you out for two months during repairs? This coverage handles it.

Dwelling coverage rebuilds or repairs the physical structure after covered damage

Other structures coverage protects detached garages, sheds, or fences, typically around 10% of your dwelling limit

Personal property coverage replaces belongings inside the home, usually 50 to 70% of dwelling coverage

Loss of Use / Additional Living Expenses pays for temporary housing and meals during repairs

Liability protection defends you in court and pays damages if you’re legally responsible for injury or property damage

Medical payments to others covers guest medical bills immediately, no lawsuit required

Common Perils Covered Under Starter Property Insurance

Starter policies come in two formats: named perils and all risk (sometimes called open perils). Named perils only cover damage from events explicitly listed in your contract. If it’s not on the list, it’s not covered. All risk policies flip that around. They cover everything except what’s explicitly excluded, which usually means broader protection. Most starter policies for first-time buyers are named perils because they cost less. You need to know exactly which disasters your policy will actually pay for.

Fire and smoke whether it’s a kitchen grease fire or a neighbor’s wildfire that spreads

Lightning strikes direct hits that fry electronics or start structural fires

Windstorms and hail roof damage, broken windows, siding torn off in a storm

Theft and vandalism stolen belongings or malicious property damage

Vehicle or aircraft damage a car crashes through your fence or a small plane hits your roof

Volcanic eruption rare, but explicitly covered in most policies

Riots and civil commotion property damage during protests or disturbances

Water damage from burst pipes sudden pipe failures, but not slow leaks or maintenance neglect

The specific list varies by insurer and policy tier. Some carriers include additional events like falling objects or the weight of ice and snow. Others keep the list shorter to reduce premiums. Always check your policy’s declarations page to see exactly which perils apply to your coverage. Ask your agent to walk through scenarios that matter in your area. Hailstorms in the Midwest, wildfire smoke damage in the West.

What Starter Property Insurance Does Not Cover

Flood damage and earthquake damage are the two biggest exclusions in every standard homeowners policy, starter or otherwise. Burst pipe that soaks your basement? Covered. Spring rainstorm that sends two feet of water through your front door? Not covered. You need a separate flood insurance policy, usually through the National Flood Insurance Program (NFIP) or a private flood carrier. Same goes for earthquakes. Cracked foundations, toppled chimneys, structural shifts require standalone earthquake insurance. Especially common in California and the Pacific Northwest but available nationwide.

Routine maintenance issues and damage from neglect are also excluded. If your roof’s been leaking for six months and you never fixed it, the resulting mold and water damage won’t be covered. The policy expects you to maintain your home in good condition. Wear and tear over time also falls on you. Faded paint, old carpet, a 20-year-old water heater that finally dies. Your responsibility, not the insurer’s. Sewer and drain backups are excluded unless you purchase a separate endorsement. Without it, sewage flooding your basement after a heavy rain is entirely out of pocket.

Flood damage rainwater, storm surge, or overflowing rivers require separate flood insurance

Earthquake damage structural and foundation damage from seismic activity needs its own policy

Mold and fungus unless directly caused by a sudden covered peril, mold cleanup is excluded

Pest infestations termites, rodents, and other pests are considered preventable maintenance

Gradual damage slow leaks, long-term settling, and deferred maintenance aren’t covered events

Coverage Limits, Deductibles, and How Starter Policies Calculate Payouts

Your dwelling coverage limit is the maximum your insurer will pay to rebuild your home. It should reflect current construction costs in your area, not your purchase price or property tax assessment. Personal property limits are usually pegged to a percentage of dwelling coverage. Insure your dwelling for $200,000 and you might have $100,000 to $140,000 in personal property protection. Other structures coverage, like a detached garage or shed, is typically capped at about 10% of the dwelling limit unless you request more.

Deductibles control how much you pay out of pocket before insurance kicks in. A $1,000 deductible means you cover the first $1,000 of every claim. Raising it to $2,500 or $5,000 will lower your monthly premium, but you’ll need that cash ready if disaster strikes. Hail damages your roof and the repair estimate is $8,000? You pay your deductible first, $1,000 or $2,500, and the insurer pays the rest. Choosing a deductible you can comfortably afford in an emergency is more important than chasing the lowest premium.

Policies pay claims using one of two methods: replacement cost or actual cash value. Replacement cost reimburses you for the full cost to replace or repair damaged property with new materials of similar quality. No depreciation deducted. Actual cash value subtracts depreciation based on age and condition. A five-year-old couch might be worth half what you originally paid. Most starter policies default to actual cash value for personal property to keep premiums low, but you can upgrade to replacement cost coverage for a modest increase. Worth considering if most of your belongings are relatively new.

| Method | How It Works | Typical Outcome |

|---|---|---|

| Actual Cash Value (ACV) | Pays replacement cost minus depreciation based on age and wear | Lower payout; older items receive much less than new-item cost |

| Replacement Cost (RCV) | Pays full cost to replace with new, similar-quality items | Higher payout; you can buy new equivalents without out-of-pocket gap |

| Deductible Impact | Flat dollar amount you pay first on every covered claim | Higher deductible = lower premium but more cash needed at claim time |

Optional Endorsements That Strengthen Starter Property Insurance

Endorsements (also called riders or floaters) are add-ons that patch common gaps in starter policies. They cost extra, but they’re usually far cheaper than discovering you’re uninsured after a loss. The most popular endorsements address high-value personal items, water damage from sources the base policy excludes, and building code upgrades that inflate reconstruction costs after a major loss.

Even if your starter policy includes basic personal property coverage, items like engagement rings, custom bicycles, camera equipment, and fine art often have sublimits as low as $1,000 to $2,500 per category. Scheduled personal property endorsements let you list specific valuables with their appraised values, removing those sublimits entirely and covering a wider range of perils. Sometimes even accidental damage or mysterious disappearance that the base policy won’t touch.

Scheduled Personal Property

This endorsement covers jewelry, watches, musical instruments, collectibles, and other high-value items at their full appraised value. No deductible in many cases. You’ll need recent appraisals or receipts to prove value, but once scheduled, a stolen $4,000 engagement ring is covered for $4,000, not the $1,500 sublimit in your base policy.

Water Backup Coverage

Standard policies exclude water damage from sewer or drain backups, sump pump failures, and similar sources. This endorsement fills that gap, covering cleanup, repairs, and replacement of damaged property when a basement drain overflows or a sump pump quits during a storm. Common scenarios that can cost thousands to remediate.

Ordinance and Law Coverage

If your home is destroyed and local building codes have changed since it was built, reconstruction may require expensive upgrades. New electrical systems, energy-efficient windows, earthquake retrofitting. Ordinance and law coverage (also called building code upgrade coverage) pays the additional cost to bring your rebuilt home up to current code. Prevents a situation where your dwelling limit falls short because modern standards demand more.

Comparing Starter Property Insurance vs. Comprehensive Policies

Starter policies deliver the same six core coverages as comprehensive homeowners insurance. Dwelling, other structures, personal property, loss of use, liability, and medical payments. But with lower limits, fewer endorsements, and narrower peril lists to keep premiums affordable for first-time buyers or properties with modest values. Comprehensive policies raise those limits, broaden coverage to all risk formats, and bundle in endorsements that starter buyers usually purchase separately. Scheduled items, extended replacement cost, higher liability caps.

The practical difference shows up in two places: claim payouts and peace of mind. A starter policy might set dwelling coverage at exactly what a basic rebuild costs today, with no cushion for cost overruns or premium materials. A comprehensive policy adds extended replacement cost, which pays 125% or even 150% of your dwelling limit if lumber prices spike or supply-chain delays inflate contractor fees. Comprehensive policies also default to replacement cost for personal property and include higher sublimits for valuables. You’re less likely to discover coverage gaps after a loss.

| Feature | Starter Policy | Comprehensive Policy |

|---|---|---|

| Dwelling Coverage | Reconstruction cost estimate; no overrun buffer | Extended replacement cost (125% to 150% of limit) |

| Personal Property Basis | Usually actual cash value (depreciation applied) | Replacement cost standard; higher sublimits for valuables |

| Covered Perils | Named-perils list (fire, wind, theft, etc.) | All-risk/open-perils (covers everything except exclusions) |

| Endorsements Included | Few or none; most are optional add-ons | Scheduled items, water backup, ordinance & law often bundled |

Starter policies fit first-time buyers purchasing homes below the median price in their market, especially when budgets are tight and the property doesn’t have high-end finishes, valuable collections, or unusual risks. Comprehensive coverage makes sense for buyers with custom upgrades, extensive personal property, or homes in areas where rebuilding costs are volatile. Wildfire zones, hurricane-prone coastal markets, historic neighborhoods with strict building codes.

Mortgage Requirements and Proof of Coverage for Starter Properties

Nearly every mortgage lender in the United States requires homeowners insurance as a condition of closing. The lender holds a lien on your property. If the house burns down or suffers catastrophic damage, they want assurance that it will be rebuilt or that their loan will be repaid. Most lenders require dwelling coverage equal to the loan amount or the full reconstruction cost, whichever is higher. They’ll ask for proof before funding the mortgage.

Proof comes in the form of a declarations page. A one or two-page summary of your policy that lists coverages, limits, deductibles, endorsements, effective dates, and the lender’s name as the mortgagee (the party with a financial interest). You’ll receive the declarations page from your insurer as soon as you bind coverage. Your agent or insurer will send a copy directly to your lender’s underwriting department. If coverage lapses or you cancel the policy, the lender is notified and may purchase expensive force-placed insurance on your behalf and bill you for it. Keeping continuous coverage is essential.

Policy number and effective dates confirms active coverage

Dwelling coverage limit must meet or exceed lender’s minimum (usually the loan amount or rebuild cost)

Mortgagee clause names the lender as loss payee so claim checks are co-issued to you and the bank

Starter Policy Cost Factors and Ways to Lower Premiums

Premiums for starter property insurance vary widely based on where you live, the age and condition of your home, and your personal risk profile. Location is the biggest driver. Homes in coastal hurricane zones, wildfire-risk areas, or regions with high crime rates pay significantly more because the likelihood of a claim is higher. A $200,000 home in a low-risk suburb might cost $800 a year to insure. The same home on the Gulf Coast could run $2,500 or more due to windstorm exposure.

Your home’s age, construction type, and condition also matter. Older homes with outdated electrical, plumbing, or roofing systems are more likely to suffer losses. Insurers charge more or require updates before offering coverage. Brick and stone homes generally cost less to insure than wood-frame houses because they’re more resistant to fire and wind damage. Many insurers also check your credit-based insurance score, a metric that correlates credit history with claim frequency, and offer lower rates to buyers with strong credit.

The easiest way to lower your premium is to ask about discounts and compare quotes from multiple carriers. Bundling your home and auto insurance with the same company often saves 10% to 25% on both policies. Installing a monitored security system, smoke detectors, or a sprinkler system can earn another 5% to 15% off. Raising your deductible from $500 to $2,000 will cut your premium noticeably, but only do it if you can afford that higher out-of-pocket cost in an emergency. Review your coverage annually. If you’ve paid down your mortgage or your home’s value has dropped, you might be overinsured and paying for more dwelling coverage than you need.

Bundling home and auto insurance saves 10% to 25% on both policies

Security and fire-safety systems monitored alarms, smoke detectors, sprinklers earn 5% to 15% discounts

Higher deductibles moving from $500 to $2,000 significantly lowers premiums

Claims-free discount some insurers reduce rates after several years without a claim

Newer roof or updated systems recent roof replacement, electrical, or plumbing updates can lower risk scores and premiums

How to File a Claim on a Starter Property Insurance Policy

Filing a claim starts the moment damage occurs. First step is to document everything. Take photos and videos of the damage from multiple angles, make a list of damaged or destroyed items, and save receipts or proof of purchase if you have them. If it’s safe, take temporary steps to prevent further damage. Tarp a hole in the roof or shut off water to stop a leak. Most policies require you to mitigate additional loss. Then contact your insurer as soon as possible. Most companies have 24/7 claims hotlines. Early notification speeds up the entire process.

Once you’ve reported the claim, the insurer will assign an adjuster to inspect the damage, verify coverage, and estimate repair costs. Keep detailed records of every conversation. Write down the adjuster’s name, the claim number, dates and times of calls, and what was discussed. If you hire contractors for emergency repairs, get written estimates and save all receipts. You’ll need to submit them for reimbursement. The insurer will issue a payout based on your coverage type. Actual cash value policies pay depreciated amounts up front. Replacement cost policies often pay ACV first and the rest after you complete repairs and submit invoices.

Document the damage immediately. Photograph and video everything before cleanup or temporary repairs.

Notify your insurer within 24 hours. Call the claims hotline and provide your policy number and a brief description of the loss.

Mitigate further damage. Tarp leaks, board broken windows, shut off utilities if needed. Save receipts for these expenses.

Meet the adjuster. Walk them through the damage, point out every affected area, and answer questions about what happened.

Obtain repair estimates. Get written quotes from licensed contractors. Your insurer may require multiple bids for large claims.

Submit documentation and invoices. Provide receipts, before and after photos, and contractor invoices to finalize the claim and receive full payment.

Claims can be denied if the damage falls under a policy exclusion, results from lack of maintenance, or occurs from a peril not listed in a named perils policy. Mold discovered months after a slow roof leak won’t be covered because the leak should have been fixed when it started. Earthquake damage on a standard policy or flood damage without a separate flood policy will be denied outright. If your claim is denied and you believe the decision is wrong, you have the right to appeal. Ask for a written explanation, review your policy’s coverage and exclusions with your agent, and consider hiring a public adjuster or attorney if the disputed amount is significant.

Final Words

You’ve seen the core protections: dwelling tied to reconstruction cost, personal property often at 50–70% of the dwelling, additional living expense for temporary housing, liability for legal defense and damages, and medical payments for guest injuries. We also covered common perils, typical exclusions like flood and earthquake, limits, deductibles, and useful endorsements.

If you’re still asking what does starter property insurance cover, the short answer is this: essential homeowner protections with lower limits and fewer add-ons. Check your limits and endorsements, update after big life changes, and you’ll be in a much stronger position.

FAQ

Q: What items are covered by a basic property insurance policy?

A: A basic property insurance policy covers the dwelling (reconstruction cost), other structures (often ~10% of dwelling), personal property (commonly 50–70% of dwelling), additional living expenses, liability, and medical payments to guests.

Q: What is the 80% rule in property insurance?

A: The 80% rule in property insurance says you should insure your home for at least 80% of its replacement cost; otherwise the insurer may proportionally reduce your payout on a covered loss.

Q: How much is homeowners insurance on a $400,000 house?

A: Homeowners insurance on a $400,000 house typically ranges from $1,000 to $3,000 per year in the U.S., depending on location, deductible, rebuild cost, claims history, and coverage choices.

Q: What two events are not covered under homeowners insurance?

A: Two events not covered under standard homeowners insurance are floods and earthquakes; both usually require separate policies or endorsements to provide protection.