{kind=link}

What happens if a wildfire or hurricane makes rebuilding cost way more than your policy limit?

Extended replacement cost coverage is a simple add-on that can pay above the dollar limit on your policy when costs spike after a covered loss.

Usually it adds 20–50 percent more (often about 25%), giving you breathing room when lumber, labor, or contractor demand explodes.

This post explains how it works, when it actually kicks in, and the key trade-offs so you can decide if the extra protection fits your risk.

Core Explanation of Extended Replacement Cost Coverage

Extended replacement cost coverage is a dwelling insurance add-on that lets your insurer pay more than your policy’s printed limit when rebuild costs spike after a big disaster. Most homeowners policies cover the actual replacement cost up to whatever dwelling limit is on your declarations page. But if lumber shortages, contractor backlogs, or regional demand surges push rebuild costs higher, that base limit won’t cut it. Extended replacement cost steps in to cover the gap, usually bumping available funds to somewhere between 120% and 150% of your dwelling limit. A typical endorsement adds 25% on top, so a $400,000 policy becomes a $500,000 maximum if your insurer confirms that extraordinary conditions are in play.

This only kicks in when adjusters verify that rebuild costs have jumped beyond normal levels because of weird factors like post-wildfire demand spikes, hurricane driven material shortages, or the fact that everyone in your zip code is trying to rebuild at once. Extended replacement cost isn’t a free pass for underinsuring on purpose. If you set a $300,000 dwelling limit on a home that actually costs $400,000 to rebuild under normal conditions, the endorsement won’t just cover the difference. Your insurer expects the base limit to reflect true replacement cost before you even buy the policy.

That said, extended replacement cost does give you breathing room when real cost inflation happens after a covered loss. It protects homeowners who insured their place correctly but got hit with unpredictable price jumps post disaster. Adjusters have to confirm the cause and size of the increase, and insurers only release extra funds when they see clear proof of extraordinary labor or material inflation.

What extended replacement cost coverage does and doesn’t do:

- Does: Pay above the policy limit when rebuild costs blow past expectations because of crazy demand or supply problems

- Does: Apply when labor shortages, material shortages, or disaster driven inflation send contractor bids through the roof

- Does not: Automatically fix intentional underinsurance or routine inflation you should’ve addressed at renewal

- Does not: Trigger for every claim. Adjuster verification of abnormal conditions is required

How Extended Replacement Cost Coverage Works During a Rebuild

Extended replacement cost only turns on when your insurer’s adjuster confirms that rebuilding will cost more than the policy limit because of abnormal market conditions. The insurer starts by estimating rebuild cost using current contractor bids, material pricing, and labor rates. If that estimate stays inside the policy limit, the claim moves forward under standard replacement cost rules. But if the estimate blows past the limit and the adjuster verifies that the spike came from demand surge, regional shortages, or other weird factors, the insurer lets the claim tap into the extended limit.

Here’s how it plays out. Your home is insured for $400,000 and it burns down in a wildfire that torches hundreds of nearby homes. Local contractors are buried, lumber prices have doubled, and roofers are booking months out. Your contractor submits a $450,000 bid to rebuild. If your policy includes a 25% extended replacement cost endorsement, your available dwelling limit jumps to $475,000 (125% of $400,000), which covers the $450,000 rebuild. The insurer reviews the contractor’s numbers, confirms that local conditions justify the higher cost, and approves payment above the base limit.

| Scenario | Base Limit | Extended Limit | Result |

|---|---|---|---|

| Regional wildfire; contractor shortage; materials up 20% | $350,000 | $437,500 (25% ERC) | Covers $425,000 rebuild; insurer pays full claim |

| Hurricane zone; all subcontractors booked; prices surge 30% | $500,000 | $625,000 (25% ERC) | Covers $610,000 rebuild; insurer pays full claim |

| Normal fire; no regional crisis; rebuild estimate $380,000 | $400,000 | $500,000 (25% ERC) | Standard limit covers cost; ERC not used |

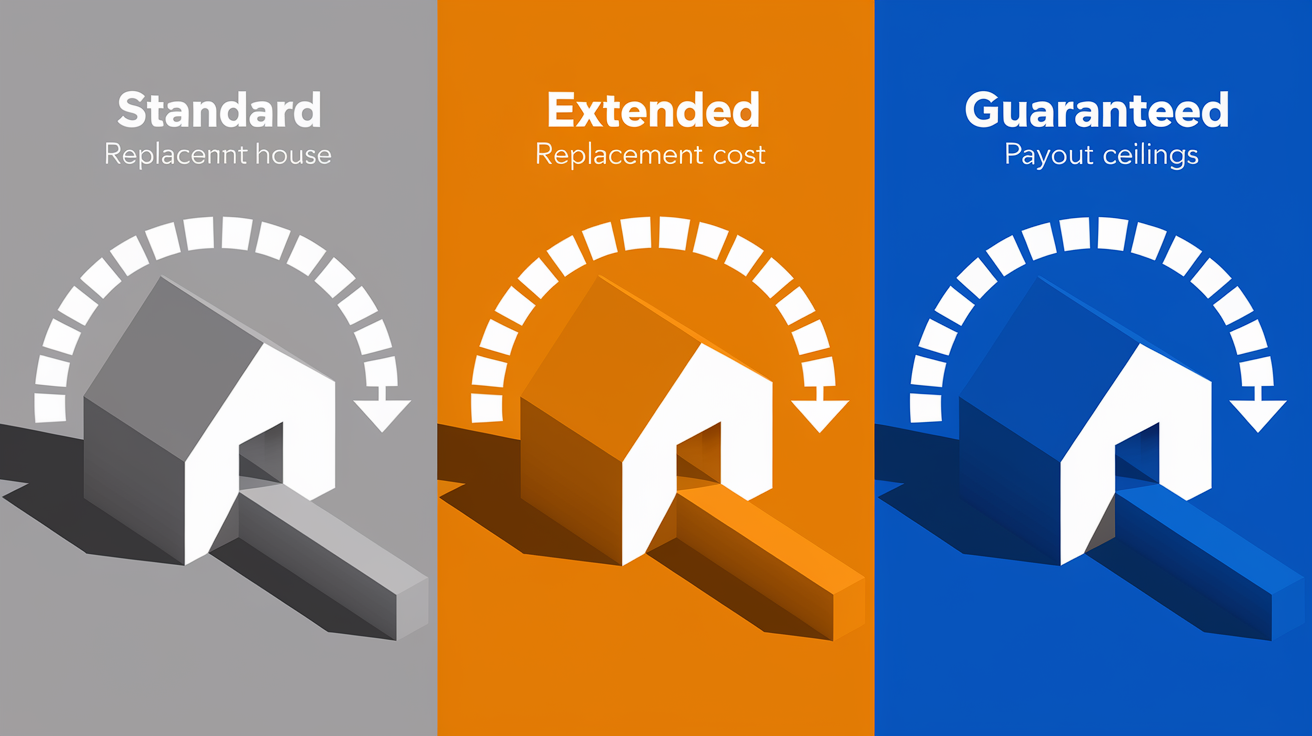

Comparison: Extended vs Standard vs Guaranteed Replacement Cost

Understanding the three tiers of replacement cost coverage helps you pick the right protection for your risk tolerance and budget.

Standard Replacement Cost

Standard replacement cost pays the cost to rebuild or replace the damaged dwelling up to the policy’s stated limit and nothing more. If your dwelling limit is $300,000 and a total loss rebuild costs $320,000 because of normal inflation or small miscalculations, you’re on the hook for the $20,000 difference. Standard replacement cost assumes the dwelling limit was set right when you bought the policy and that annual inflation adjustments keep up with rising construction costs. Most basic homeowners policies default to standard replacement cost.

Extended Replacement Cost

Extended replacement cost lets the payout go above the stated dwelling limit, but only up to a capped percentage, usually 120% to 150% of the policy limit. If your policy limit is $300,000 and you’ve got a 125% extended replacement cost endorsement, the insurer will pay up to $375,000 to rebuild if extraordinary conditions push costs higher. The cap gives you real breathing room, but it’s not unlimited. If rebuild costs blow past even the extended limit, you pay the difference.

Guaranteed Replacement Cost

Guaranteed replacement cost (sometimes called full replacement cost) promises to pay the full cost to rebuild your dwelling no matter how high that cost goes, with no dollar cap. If your $300,000 policy runs into a $500,000 rebuild after a major disaster, guaranteed replacement cost covers the entire $500,000. It’s the most comprehensive option but it’s also getting harder to find. Many insurers don’t offer it anymore, especially in disaster prone areas.

Key differences between the three coverage types:

- Standard: Pays up to the policy limit only; you cover everything above that amount

- Extended: Pays beyond the policy limit up to a specified percentage (like 125%); caps the max payout at that percentage

- Guaranteed: Pays the full rebuild cost with no cap; hardest to find and most expensive

- Inflation guard: Not a separate coverage type but an automatic annual limit increase (usually 2% to 4%) that applies to all three types and helps keep base limits current year over year

- Practical difference: Extended coverage protects against sudden spikes; guaranteed coverage protects against any cost escalation no matter what caused it

Situations Where Extended Replacement Cost Coverage Becomes Highly Valuable

Extended replacement cost matters most when disaster hits your home at the same time it hits dozens or hundreds of others nearby, creating crazy demand for contractors, materials, and labor. Wildfires that burn through entire neighborhoods, hurricanes that flatten whole towns, and tornadoes that wipe out subdivisions all trigger the same economic effect. Too many people need to rebuild at once, and the local construction industry can’t keep up. Prices for framing lumber, drywall, roofing, plumbing, and electrical work all spike above normal. Contractors prioritize the highest bidders, and homeowners without enough coverage are forced to wait or pay the difference themselves.

Extended replacement cost also becomes valuable during periods of regional or national material shortages that happen to line up with your claim. Lumber shortages caused by mill closures, tariff fights, or pandemic related supply chain messes can raise framing costs 30% or more in just a few months. If your home burns down during one of those spikes, your policy limit might not reflect the true rebuild cost anymore, even if the limit was right when you bought the policy. The endorsement gives you headroom to absorb those surprise price jumps without forcing you to scale back finishes, square footage, or quality.

Real world scenarios where extended replacement cost has proven valuable:

- Wildfire in a subdivision: 40 homes destroyed in one neighborhood; contractor demand drives labor costs up 25%; local lumber prices double because of regional shortage

- Major hurricane landfall: Entire coastal county loses power, roofing, and siding; roofers and siding crews are booked for a year; material suppliers run low

- Regional tornado outbreak: Multiple towns hit in one day; FEMA contractors arrive but charge premium rates; local subcontractors are unavailable for months

- Pandemic era material shortage: Lumber, PVC pipe, and appliances all see price surges and delivery delays during your rebuild; costs climb 20% above pre-pandemic estimates

- Labor shortage in growing markets: Hot real estate market pulls all contractors into new construction; remodeling and rebuilding work commands premium pricing

Cost, Requirements, and Availability of Extended Replacement Cost Endorsements

Extended replacement cost endorsements bump your annual premium, but the extra cost is usually pretty modest compared to the extra limit protection you get. Insurers price the endorsement based on the odds of regional demand surges, your home’s location, and the percentage increase you pick. A 25% endorsement on a $400,000 dwelling adds $100,000 of potential payout but might only cost $50 to $150 per year in added premium, depending on the carrier and state. The endorsement is especially cheap in areas with lower disaster risk, and it gets more expensive or unavailable in high risk wildfire or hurricane zones where demand surges are common.

Insurers set conditions to make sure policyholders don’t use extended replacement cost as a substitute for accurate dwelling limits. Common requirements include keeping your Coverage A dwelling limit at or above the estimated replacement cost based on the insurer’s valuation tools, telling the insurer within 60 days of any physical changes to the home that raise replacement cost by $5,000 or more (like room additions, new decks, or upgraded kitchens), and accepting periodic re-evaluations or index adjustments that bump the base limit to keep up with inflation. If you don’t meet these conditions before a covered loss, the insurer can deny the extended replacement cost benefit, leaving you with just the base policy limit.

Availability varies a lot by carrier and state. Some insurers offer extended replacement cost as a standard option on all dwelling policies, while others save it for homes in lower risk areas or require updated appraisals before approval. A few states restrict or regulate the endorsement language, and some carriers have stopped offering it entirely in favor of inflation guard endorsements that automatically raise limits each year by a small percentage. It’s also worth remembering that personal property coverage (Coverage C) is often calculated as a percentage of the dwelling limit, usually 50% or 75%. So if you intentionally lower your Coverage A limit to save on premium, you can reduce your personal property protection even if you’ve got an extended replacement cost endorsement.

Common eligibility conditions for extended replacement cost endorsements:

- Keep Coverage A at least equal to the insurer’s estimated replacement cost (including inflation adjustments)

- Notify the insurer within 60 days of any change or inaccuracy in dwelling information

- Notify the insurer within 60 days of starting physical changes that increase replacement cost by $5,000 or more

- Accept periodic re-evaluations or valuation updates from the insurer

Numeric Examples Showing How Extended Replacement Cost Pays Out

Walking through specific dollar amounts makes the benefit easier to see. Suppose your Coverage A dwelling limit is $200,000 and you add a 50% extended replacement cost endorsement. Your max available rebuild funds jump to $300,000 (150% of $200,000). If a covered total loss happens and contractor bids come in at $280,000 because of post disaster demand surge, your insurer confirms the abnormal conditions and approves payment up to the extended limit, fully covering the $280,000 rebuild without asking you to pay anything out of pocket.

Another common scenario involves a $400,000 dwelling limit with a 25% extended replacement cost endorsement, which raises the max payout to $500,000 (125% of $400,000). If a regional wildfire destroys your home and contractor estimates hit $450,000 because of labor shortages and material price spikes, the extended limit covers the full rebuild cost. But if the rebuild estimate climbs to $520,000, exceeding even the extended limit, you’re responsible for the $20,000 difference unless you negotiate or scale back finishes to stay within the $500,000 cap.

| Base Limit | ERC % | Max Available | Rebuild Cost | Outcome |

|---|---|---|---|---|

| $200,000 | 50% | $300,000 | $280,000 | Fully covered; insurer pays $280,000 |

| $400,000 | 25% | $500,000 | $450,000 | Fully covered; insurer pays $450,000 |

| $350,000 | 20% | $420,000 | $435,000 | Shortfall; insurer pays $420,000; homeowner pays $15,000 |

| $500,000 | 25% | $625,000 | $610,000 | Fully covered; insurer pays $610,000 |

Final Words

Extended replacement cost coverage raises your dwelling limit above the policy when rebuild costs spike after major losses. We defined the endorsement, showed how claims work, compared it to other options, and gave real payout examples.

Check your Coverage A, ask your agent about the ERC percentage and valuation rules, and don’t cut base limits to chase a cheaper premium.

If you still want a plain answer to what is extended replacement cost coverage, it’s a capped over-limit boost that helps cover extraordinary rebuild inflation. A little planning now can save money and stress later.

FAQ

Q: What’s the difference between replacement cost and extended replacement cost? What does 150 extended replacement cost mean?

A: The difference is replacement cost pays to rebuild up to your policy limit, while extended replacement cost adds an over-limit buffer (commonly 120–150%). “150” means coverage up to 150% of the stated limit.

Q: What are the disadvantages of replacement cost coverage?

A: Replacement cost coverage disadvantages include higher premiums, potential underinsurance if limits are too low, required proof of rebuilding costs, and exclusions for code upgrades, some living-expense gaps, or certain endorsements.

Q: What not to say to home insurance?

A: You should avoid telling your insurer you caused damage intentionally, that you started repairs without approval, that you permanently live elsewhere, or giving inconsistent or vague details about the incident.