{kind=link}

Think your insurance check will buy a brand-new replacement after a loss?

Think again.

How your insurer values things changes what ends up in your hands.

Actual Cash Value subtracts depreciation, so you get the item’s current worth.

Replacement Cost pays to replace with new materials and usually returns the depreciation after you finish repairs.

This post shows how depreciation is calculated, how it changes payout timing and out-of-pocket cost, and which option might suit your home and budget.

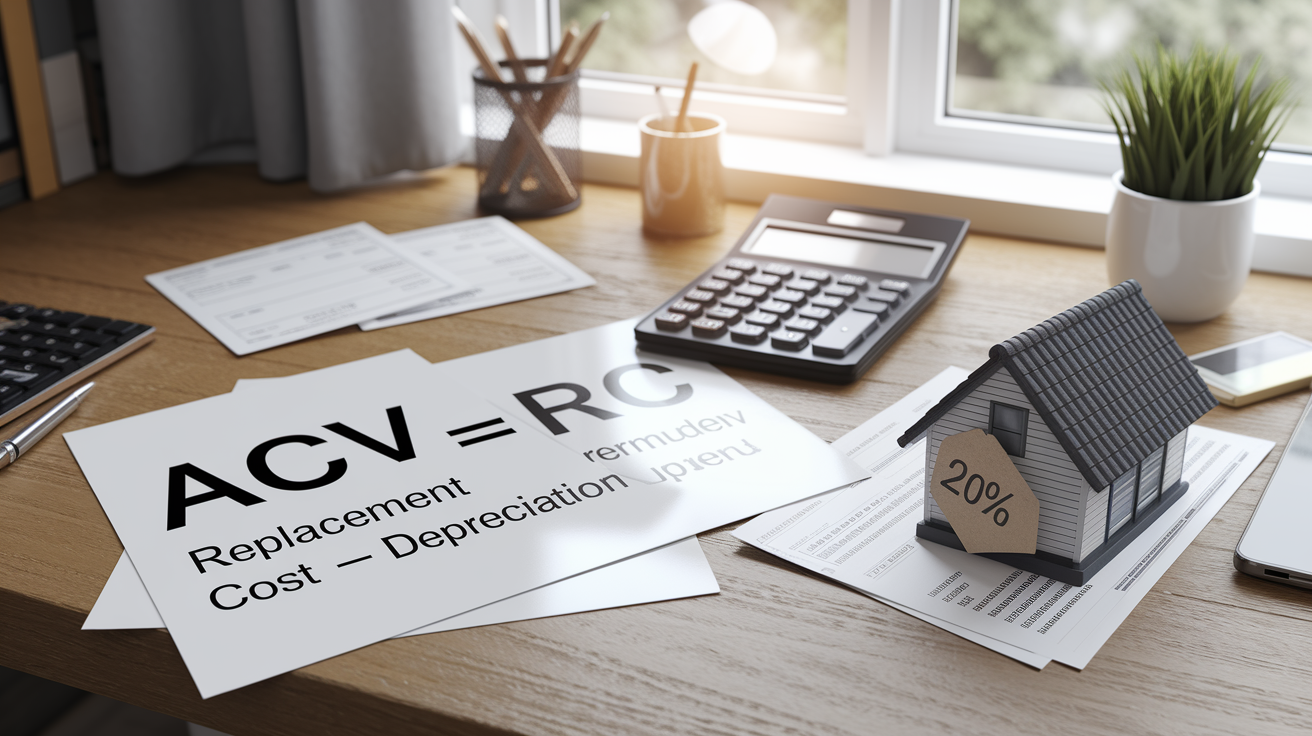

Clear Breakdown of Actual Cash Value vs Replacement Cost Payout Methods

Actual Cash Value (ACV) is what your insurer pays to replace a damaged item minus depreciation. The formula’s simple: ACV = Replacement Cost − Depreciation. Depreciation itself gets calculated as Age ÷ Useful Life. Say your roof’s five years old with a 25 year expected lifespan. Depreciation is 5 ÷ 25 = 20%. If replacing that roof costs $15,000 today, your ACV payout would be $15,000 × (1 − 0.20) = $12,000, before your deductible. The key reason ACV payouts are lower? The insurer’s only paying for the current value of a used item, not a brand new one.

Replacement Cost (RC) is the full cost to repair or replace your damaged property with new materials of like kind and quality, without deducting for depreciation. Under RC policies, you get the entire $15,000 replacement cost in the roof example above (minus your deductible). Many insurers pay Replacement Cost in two stages. First, they send you the ACV amount ($12,000), then after you complete the repair and submit receipts, they release the held back depreciation ($3,000). This two step process protects the insurer by making sure you actually replace the item rather than pocketing a depreciated value check and leaving the damage unrepaired.

The financial consequence of choosing ACV over RC? You personally cover the depreciation gap, which can be thousands of dollars on major losses like roofs, HVAC systems, or entire home contents. In exchange for accepting that risk, ACV premiums are typically lower. Replacement Cost policies cost more, often 10–30% higher in premium, because the insurer’s on the hook for the full replacement price, not just the depreciated value.

Here are the core contrasts between ACV and RC:

- Depreciation: ACV subtracts it, RC does not deduct it from your payout

- Payout timing: ACV often paid in one check, RC frequently paid as ACV first, then recoverable depreciation after you submit invoices

- Documentation required: RC usually demands receipts and contractor bills to release the second payment, ACV may settle with less paperwork

- Premium impact: RC premiums run roughly 10–30% higher than equivalent ACV coverage, depending on property age and insurer underwriting

Understanding Actual Cash Value and How Insurers Calculate Depreciation

Actual Cash Value reflects what your damaged item’s worth today, accounting for its age, condition, and remaining useful life. Insurers rely on industry standard useful life tables to determine how quickly items depreciate. A laptop might have a four year useful life. Carpeting seven to twelve years. A residential roof twenty to thirty years. The depreciation percentage is simply the fraction of useful life already consumed. Once the insurer has the replacement cost estimate from a contractor or pricing guide, they multiply that figure by (1 − depreciation percentage) to arrive at the ACV. Your deductible is then subtracted from that depreciated amount, and the result is your net payout.

Depreciation percentages can be surprisingly large, especially on items with short useful lives. If you bought a laptop two years ago for $1,200 and the replacement cost today is also $1,200, but the insurer assumes a four year useful life, the depreciation is 2 ÷ 4 = 50%. Your ACV is therefore $1,200 × 0.50 = $600. Subtract a $500 deductible, and you walk away with $100, far short of the cost of a comparable new laptop. Deductibles apply equally to both ACV and RC settlements, but the depreciation hit under ACV means the starting payout’s already reduced before the deductible comes into play, compounding the out of pocket burden.

Depreciation Examples

Consider a five year old asphalt shingle roof with a 25 year useful life and a current replacement cost of $10,000. Depreciation is 5 ÷ 25 = 20%, so the ACV is $10,000 × (1 − 0.20) = $8,000. With a typical $1,500 deductible, your net ACV check is $6,500, leaving you $3,500 short of the full replacement cost.

Now picture a six year old water heater with a twelve year useful life and a $1,200 replacement cost. Depreciation is 6 ÷ 12 = 50%, yielding an ACV of $600. After a $500 deductible, your payout’s just $100. Under a Replacement Cost policy, you’d receive the full $1,200 minus the deductible, $700 net, enough to cover most or all of a new unit’s purchase price.

Replacement Cost Coverage, Payment Timing, and Policy Variations

Replacement Cost coverage pays the full amount needed to repair or replace damaged property with new materials of like kind and quality, without any deduction for depreciation. The critical detail most policyholders miss is the two step payment process. When you file a claim, the insurer typically issues an initial check for the Actual Cash Value (the depreciated amount). You then hire a contractor, complete the repair or replacement, and submit the final invoice and receipts. Once the insurer verifies you’ve spent the money, they release the “recoverable depreciation,” the difference between the ACV and the full Replacement Cost. This staged approach ensures you actually rebuild rather than taking a smaller check and walking away.

Replacement Cost limits still apply, and your policy’s dwelling or personal property limits cap what the insurer will pay. If your policy lists a $300,000 dwelling limit and your home’s actual rebuild cost is $375,000, you’re responsible for the $75,000 shortfall unless you carry additional coverage. To receive the full RC payout, you must provide contractor invoices showing the work was completed and the materials purchased. Insurers won’t release recoverable depreciation on promises or estimates, only on proof of expenditure. This documentation requirement adds a layer of complexity to RC claims that ACV claims avoid, but it also ensures the insurer pays for genuine rebuilds, not hypothetical ones.

Replacement Cost coverage is particularly valuable for homeowners with newer roofs, HVAC systems, appliances, and structural components, where depreciation on an ACV policy would create significant gaps. While RC premiums run higher, often 10–30% above ACV rates, the peace of mind and reduced out of pocket risk usually justify the extra cost for primary residences and high value properties.

RC Variations

Standard Replacement Cost covers repairs or replacements up to your stated policy limit without depreciation. If your dwelling’s insured for $250,000 and the rebuild costs $250,000, you receive the full amount (minus your deductible) after submitting receipts.

Extended Replacement Cost adds a buffer, typically 20% to 50% above your policy limit, to help cover unexpected cost spikes due to inflation, material shortages, or labor market changes. For example, a policy with a $300,000 limit and 25% extended RC would pay up to $375,000 to rebuild. This endorsement costs extra but protects against sudden price jumps between the time you bought the policy and the time disaster strikes.

Guaranteed Replacement Cost offers the broadest protection. The insurer commits to rebuilding your home to its original condition regardless of the final cost, even if it exceeds your policy limit. Guaranteed RC policies often require regular appraisals to keep limits reasonably aligned with true rebuild costs, and they typically carry higher premiums and stricter underwriting. Not all insurers offer this option, and it’s most common for newer homes in stable construction markets.

Calculation Examples Comparing Cash Value vs Replacement Value

Walking through side by side numbers makes the financial difference between ACV and RC immediately clear. These examples use realistic replacement costs, typical useful life assumptions, and common deductibles to show how much more you receive under Replacement Cost coverage and how much you’d have to pay out of pocket under Actual Cash Value.

Take the five year old roof scenario. Current replacement cost is $15,000, the roof’s useful life is 25 years, so depreciation is 5 ÷ 25 = 20%. Under an ACV policy, the payout is $15,000 × (1 − 0.20) = $12,000. Subtract a $1,500 deductible and your net check is $10,500. To install a new roof costing $15,000, you’re $4,500 short. Under a Replacement Cost policy, the insurer initially pays the $10,500 ACV amount, you submit the contractor’s invoice after installation, and they release the remaining $3,000 in recoverable depreciation. Your total payout is $15,000 − $1,500 = $13,500, covering nearly the entire job and leaving you only the deductible to pay.

The same math applies to personal property with shorter useful lives. A two year old laptop with a four year lifespan and a $1,200 replacement cost depreciates 50%. ACV payout is $600. With a $500 deductible, you receive $100. Replacement Cost pays the full $1,200 minus the $500 deductible, $700 net. The $600 difference is the depreciation you avoid under RC. For a three year old sofa originally costing $2,000 with a ten year useful life, depreciation is 30%. ACV is $1,400, RC is the full replacement value. For a five year old winter coat purchased for $400 with an eight year useful life, ACV drops to $250 (62.5% depreciation), while RC reimburses up to the cost of a comparable new coat.

| Item | Replacement Cost | Depreciation % | ACV (before deductible) | RC (before deductible) |

|---|---|---|---|---|

| 5-year-old roof (25-year life) | $15,000 | 20% | $12,000 | $15,000 |

| 2-year-old laptop (4-year life) | $1,200 | 50% | $600 | $1,200 |

| 3-year-old sofa (10-year life) | $2,000 | 30% | $1,400 | $2,000 |

| 5-year-old coat (8-year life) | $400 | 62.5% | $150 | $400 |

Premium Differences and Out of Pocket Cost Implications

Choosing Replacement Cost over Actual Cash Value typically increases your annual premium by 10% to 30%, depending on your property’s age, location, insurer, and the specific limits you carry. For example, if your ACV homeowners premium is $1,200 per year, upgrading to RC might raise it to somewhere between $1,320 and $1,560. The exact percentage varies widely. Older homes with outdated systems may see smaller percentage increases because the insurer assumes higher depreciation offsets part of the replacement cost exposure, while newer homes with expensive finishes may face steeper hikes.

Deductibles reduce both ACV and RC payouts equally, but the depreciation gap under ACV compounds the problem. In the roof example, a $1,500 deductible subtracted from a $12,000 ACV payout leaves you with $10,500, but you still need $15,000 to replace the roof, so your total out of pocket cost is $4,500. Under RC, the $1,500 deductible is your only out of pocket expense (assuming the replacement cost matches the estimate). The depreciation gap, the portion the insurer doesn’t pay under ACV, can grow to tens of thousands of dollars on major losses like total home rebuilds, making RC the financially safer choice despite the higher premium.

Key cost considerations include:

- Premium difference: RC policies usually cost 10–30% more than equivalent ACV coverage

- Deductible: subtracted from the initial payout under both valuation methods, but RC starts from a higher base amount

- Depreciation gap: the unreimbursed portion under ACV that you pay from savings or loans, eliminated under RC

- Rebuild shortfall risk: if your dwelling limit’s too low, even RC won’t cover the full cost, extended or guaranteed RC endorsements address this

- Value of RC on major losses: a $300 annual premium increase can save you $20,000 in out of pocket rebuild costs after a total loss, making the long term math strongly favor RC for most homeowners

When Homeowners, Renters, and Landlords Should Choose Each Valuation Method

Homeowners with primary residences should almost always choose Replacement Cost for their dwelling and strongly consider RC for personal property, especially if they own newer appliances, electronics, or high value furnishings. The potential depreciation gap on a total loss or major roof/HVAC claim can easily exceed $20,000, dwarfing the modest annual premium increase. RC is particularly important if you’ve recently remodeled, installed a new roof, or upgraded major systems, because those improvements have little accumulated depreciation and would be expensive to replace out of pocket under an ACV policy. For older homes with original systems nearing the end of their useful lives, the math shifts slightly. ACV premiums are lower, but you accept the risk of large shortfalls if a covered peril strikes before you’ve budgeted for replacements.

Renters typically insure only personal property, and many insurers default renters policies to Actual Cash Value for contents. If you own expensive electronics, musical instruments, jewelry, or furniture, upgrading to Replacement Cost for personal property is often worth the small additional premium, commonly $20 to $60 per year depending on your coverage limits. The difference becomes stark when you lose a two year old laptop, gaming console, or television. ACV might pay half the replacement price, while RC reimburses the full cost of a comparable new item. For renters with minimal or older belongings, ACV can suffice, but review your inventory carefully and calculate the potential depreciation gap before deciding.

Landlords and commercial property owners face a trade off between cash flow and asset protection. Rental properties, especially older multifamily buildings or single family rentals with aging roofs and systems, can be insured under ACV to save premium dollars, with the understanding that you’ll fund part of any major repair out of reserves or future rent income. If the property’s newer or recently renovated, Replacement Cost protects your investment and ensures full restoration without eroding your equity. Commercial policies often allow you to mix valuation methods: RC for the building structure, ACV for tenant improvements or older equipment. The key is matching coverage to your risk tolerance and capital reserves.

Scenarios and rules of thumb:

- Choose ACV if premiums are tight, the property’s older with low remaining useful life on major systems, or you self insure part of the risk with cash reserves

- Choose RC if you want predictable, minimal out of pocket costs after a claim, own newer or high value property, or can’t easily absorb a $10,000+ shortfall

- RC can save thousands on a single major claim (roof, HVAC, total loss) even if you pay hundreds more in annual premium over a decade

- ACV suffices for low value secondary properties, older rental units, or personal items you’re willing to replace at depreciated value

Documentation, Proof of Loss, and Steps to Ensure Full Replacement Payment

Documentation affects your payout under both Actual Cash Value and Replacement Cost policies, but RC claims demand significantly more paperwork to unlock the full settlement. Insurers require proof that you actually spent the money to repair or replace the damaged property before they release recoverable depreciation. Without receipts, contractor invoices, and photos of the completed work, you’ll receive only the initial ACV payment and forfeit the additional funds you’re entitled to under your RC policy. Even ACV claims require a proof of loss statement describing the damaged items, their age, and original cost, but the insurer settles immediately rather than holding back depreciation.

Replacement Cost payout mechanics work like this. After your claim’s approved, the insurer sends a check for the Actual Cash Value (replacement cost minus depreciation, minus your deductible). You hire a contractor, purchase materials, and complete the repair. You then submit the final invoice, paid receipts, before and after photos, and any required certificates of completion. The insurer reviews the documentation, confirms the work matches the scope of the claim, and issues a second check for the recoverable depreciation. If you skip the documentation step or abandon the repair, the insurer keeps the depreciation holdback and you lose thousands of dollars in benefits you already paid premium to secure.

Documentation Essentials

Start your documentation process before disaster strikes by creating a home inventory with photos or video of each room, close ups of serial numbers on electronics and appliances, and receipts for major purchases stored in a cloud account or safe deposit box. After a loss, take detailed photos of all damage before touching anything. Insurers and adjusters need to see the extent and cause of the damage. When you meet with contractors, save every written estimate, even if you don’t hire that contractor. Multiple bids can support your claim for higher replacement costs. Once repairs begin, photograph work in progress and keep all material receipts, labor invoices, and permits. If the insurer requires you to retain damaged items until an adjuster inspects them, store them safely and document their location.

Proof of loss essentials include:

- Comprehensive photo and video inventory of your home and belongings taken before any loss occurs

- Receipts, model numbers, and serial numbers for appliances, electronics, furniture, and valuable items

- Multiple contractor estimates showing scope of work and itemized costs

- Final paid invoices and material receipts proving you completed the replacement or repair

- Before and after photos of the damaged area and the finished restoration

- Any required building permits, inspection certificates, or compliance documentation for structural repairs

Glossary of Cash Value and Replacement Cost Settlement Terms

Insurance settlement language can be confusing, and misunderstanding a single term can cost you thousands of dollars in unclaimed benefits. This glossary defines the core concepts you’ll encounter when comparing Actual Cash Value and Replacement Cost policies or navigating the claims process.

- Actual Cash Value (ACV): the current value of damaged property, calculated as replacement cost minus depreciation based on age and condition

- Replacement Cost (RC): the full cost to repair or replace damaged property with new materials of like kind and quality, without deducting for depreciation

- Depreciation: the reduction in an item’s value over time due to age, wear, and obsolescence, typically calculated as (Age ÷ Useful Life) × Replacement Cost

- Recoverable depreciation: the amount an insurer withholds from an initial Replacement Cost settlement and releases after the policyholder submits proof of completed repair or replacement

- Extended Replacement Cost: optional coverage that pays a percentage (often 20%–50%) above your policy’s stated dwelling limit if rebuild costs exceed that limit

- Guaranteed Replacement Cost: coverage that pays the full cost to rebuild your home to its original condition, regardless of your policy limit, as long as the home was adequately insured at policy inception

- Fair market value: the price a willing buyer would pay a willing seller for property in its current condition, sometimes used interchangeably with ACV but not identical in all contexts

- Salvage rights: the insurer’s legal ownership of damaged property after paying a total loss claim, the insurer may sell salvageable parts to recover some claim cost

Final Words

You now know the core difference between ACV and replacement cost: ACV deducts depreciation, while replacement cost aims to pay to buy new. The post walked through formulas (age ÷ useful life), clear examples, payment timing, premium trade‑offs, and the documentation you’ll need.

If you’re still wondering what is the difference between actual cash value and replacement cost, remember: ACV lowers payouts for wear and tear; RCV covers the cost to replace new. Pick the option that fits your budget and risk. You’ve got this.

FAQ

Q: Which is better, actual cash value or replacement cost?

A: The better option between actual cash value and replacement cost depends on your priorities: replacement cost pays full new-item costs (higher premiums), while ACV pays depreciated value (lower premiums, more out-of-pocket risk).

Q: What is the cash value of a $500,000 whole life insurance policy?

A: The cash value of a $500,000 whole life policy is the policy’s savings portion, not the death benefit; it varies by premiums paid, dividends/interest, and policy age—check your annual statement or ask your insurer.

Q: How do you tell if you have an ACV or RCV policy?

A: You tell if you have an ACV or RCV policy by checking your declarations page for the phrases “actual cash value” or “replacement cost,” reviewing endorsements for recoverable depreciation, or asking your agent directly.

Q: What is the actual cash value of a 20 year old roof?

A: The actual cash value of a 20-year-old roof is replacement cost minus depreciation; for example, with a 25-year useful life depreciation is 80%, so ACV would be about 20% of replacement cost before deductibles.